(Tempe, Arizona) — Economic activity in the manufacturing sector expanded in May, and the overall economy grew for the 121st consecutive month, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®.

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee: “The May PMI® registered 52.1 percent, a decrease of 0.7 percentage point from the April reading of 52.8 percent. The New Orders Index registered 52.7 percent, an increase of 1 percentage point from the April reading of 51.7 percent. The Production Index registered 51.3 percent, a 1-percentage point decrease compared to the April reading of 52.3 percent. The Employment Index registered 53.7 percent, an increase of 1.3 percentage points from the April reading of 52.4 percent. The Supplier Deliveries Index registered 52 percent, a 2.6-percentage point decrease from the April reading of 54.6 percent. The Inventories Index registered 50.9 percent, a decrease of 2 percentage points from the April reading of 52.9 percent. The Prices Index registered 53.2 percent, a 3.2-percentage point increase from the April reading of 50 percent.

“Comments from the panel reflect continued expanding business strength, but at soft levels consistent with the early-2016 expansion. Demand expansion continued, with the New Orders Index strengthening, but remaining in the low 50s, the Customers’ Inventories Index remaining at a ‘too low’ level, and the Backlog of Orders Index contracting for the first time since January 2017. Consumption (production and employment) continued to expand, resulting in a combined PMI® contribution of 0.3 percentage point. Inputs — expressed as supplier deliveries, inventories and imports — were lower this month, primarily due to inventory softening and supplier’s continuing to deliver faster, resulting in a combined 4.6-percentage point reduction in the Supplier Deliveries and Inventories indexes. Imports contracted for the second straight month. Overall, inputs reflect supply chains’ ability to respond faster and indicate that supply managers are closely watching inventories. Prices remain at a relatively stable level.

“Respondents expressed concern with the escalation in the U.S.-China trade standoff, but overall sentiment remained predominantly positive. The PMI® continues to reflect slowing expansion,” says Fiore.

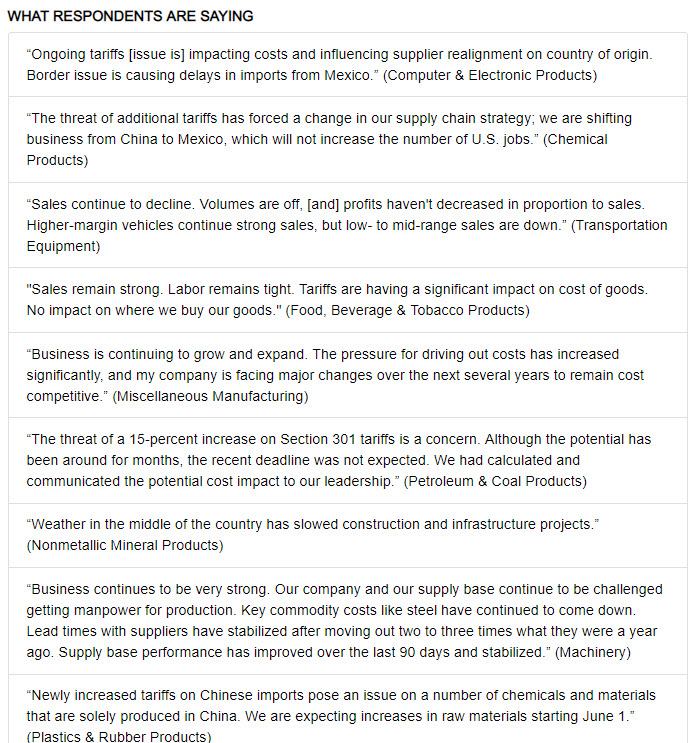

Of the 18 manufacturing industries, 11 reported growth in May, in the following order: Printing & Related Support Activities; Furniture & Related Products; Plastics & Rubber Products; Textile Mills; Miscellaneous Manufacturing; Electrical Equipment, Appliances & Components; Computer & Electronic Products; Chemical Products; Food, Beverage & Tobacco Products; Nonmetallic Mineral Products; and Machinery. The six industries reporting contraction in May — listed in order — are: Apparel, Leather & Allied Products; Primary Metals; Petroleum & Coal Products; Wood Products; Paper Products; and Fabricated Metal Products.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Ed Moya

Latest posts by Ed Moya (see all)

- Market Insights Podcast – Powell struggles to deliver a hawkish hold - 1 November 2023

- Fed React: USD/JPY softer after Fed fails to deliver hawkish hold - 1 November 2023

- EUR/USD: Dollar wavers on slower pace of Treasury Refunding Sales and mixed labor data - 1 November 2023