Thursday May 9: Five things the markets are talking about

The Sino-U.S trade war escalation remained front and center in capital markets overnight.

Global equities along with U.S stock futures continue to face pressure with time running out for U.S tariffs to escalate between the world’s two largest economies. Safe haven trading dominates proceedings with yen, gold and sovereign debt climbing as investors continue to seek sanctuary.

President Trump insists that China “broke the deal” and “will be paying for it.” His threat has many stock investors paying for it also. A ‘no broker’ trade deal has the potential to see equities give up another -10 to -20%. His comments overnight came ahead of the Chinese delegation’s arrival stateside today for ‘the’ final round of bilateral trade negotiations. China is expected to retaliate should the U.S push ahead with their tariff threats.

Elsewhere, Iran has set a two-month deadline for Europe to throw the country an economic lifeline amid U.S sanctions, otherwise it will abandon limits on uranium enrichment.

While in the U.K, PM Theresa has won a reprieve from her own Conservative Party, which has kept the rules on challenging for the leadership unchanged. In other words, Ms. May remains in place until Brexit is delivered.

On tap: The U.S. releases trade and producer-prices data this morning, along with Canada’s trade numbers (08:30 am EDT). Uber’s initial public offering is expected to price after trading closes in the U.S today.

1. Stocks sea of red

Asian equities fell to a two-month low overnight as investors wait to see whether Chinese and U.S trade negotiators are able to save an eleventh-hour trade deal in Washington this week.

In Japan, the Nikkei fell for a fourth consecutive session to end at its lowest level in six-weeks as investor caution dominates ahead of the talks stateside. The Nikkei share average dropped -0.93% Thursday. The benchmark index has lost -4.3% after hitting a 2019 high in the last week of April. The broader Topix lost -1.38%. All but two of its 33 subsectors finished in negative territory.

Down-under, Aussie stocks bucked the trend in Asia trading as Federal regulator’s moved to block a merger between the country’s third and fourth-largest telecommunications companies. The ASX 200 closed up +0.4% following six-drops in the prior eight trading days. Energy jumped +1.3% after the overnight rebound in oil prices while utilities jumped 2%. But materials lost -0.3%. In S. Korea, the Kospi index fell -2%.

In China and Hong Kong, major stock indexes closed at 11-week lows on Sino-U.S trade tensions. President Trump has vowed not to back down on his threat to increase tariffs by the end of the week in a no deal scenario. The blue-chip CSI300 index fell -1.9%, while the Shanghai Composite Index declined -1.5%. In Hong Kong, at the close of trade, the Hang Seng index was down -2.39%, its lowest close since March 8. The drop brought losses for the index to -5.9% for the week, while the Hang Seng China Enterprises index fell -2.27%.

In Europe, regional bourses trade lower across the board tracking lower Asian Indices and lower U.S Index futures as trade tensions and Brexit talks continue to weigh on markets.

U.S stocks are set to open in the ‘red’ (-0.78%).

Indices: Stoxx600 -0.75% at 379.60, FTSE -0.28% at 7,250.65, DAX -0.65% at 12,100.96, CAC-40 -1.16% at 5,354.87, IBEX-35 -0.56% at 9,175.00, FTSE MIB -0.74% at 21,047.50, SMI -0.75% at 9,549.50, S&P 500 Futures -0.78%

2. Oil falls as trade war outweighs inventory drop, gold higher

Oil are under pressure this morning as an escalating Sino-U.S trade battle is outweighing any upward pressure from a surprise decline in U.S inventories of crude.

Brent crude oil futures are at +$69.72 a barrel, down -65c from Wednesday’s close and is heading for the second consecutive weekly loss. U.S West Texas Intermediate (WTI) crude futures are at +$61.43 per barrel, down -69c and set for a third week of losses.

With market hopes fading for a Sino-U.S trade agreement, globe growth worries now dominate proceedings and is putting upward pressure on ‘black’ gold.

Note: Higher tariffs are set to take effect on Friday, during Chinese Vice Premier Liu He’s two-day visit to Washington from today.

To date, oil prices have had some support from signs of “tighter global supply” on the back of production cuts by the OPEC+ – Brent and WTI have risen more than +30% year-to-date. Supplies have also been tightened by U.S sanctions on Venezuela and Iran.

Also providing support on these deeper pullbacks in crude prices this week is the surprise drawdowns in U.S inventories. Data stateside yesterday, from the EIA, showed that U.S crude oil stocks fell by -4M barrels in the week to May 3.

Ahead of Sino-U.S trade negotiations, gold prices are little changed. Spot gold has edged up +0.2% to +$1,283.41 per ounce, while U.S gold futures are also +0.2% higher at +$1,284.10. Panic flight to safety has yet to occur, expect the yellow metal to gyrate throughout trade talks.

3. Sovereign debt remains in demand on trade concerns

Earlier this morning, Norway’s central bank (Norges) left their deposit rate unchanged at +1% as expected. The decision to keep policy steady was unanimous, however, policy makers did bring forward its next potential rate hike to June according to their statement. “The outlook and balance of risks suggests that the policy rate will be raised in June 2019”. The prior view was in H2 2019.

Note: Norges has raised the Deposit Rate on two occasions since Sept 2018 by a total of +50 bps. The last hike was back in March.

Elsewhere, the yield on two-year Treasuries has fallen -2 bps to +2.28%, while the yield on 10-year notes eased -1 bps to +2.45%. In Germany, the 10-year Bund yield fell -1 bps to -0.05%, its fifth straight decline, while down-under, Australia’s 10-year yield dropped -2 bps to +1.7145%.

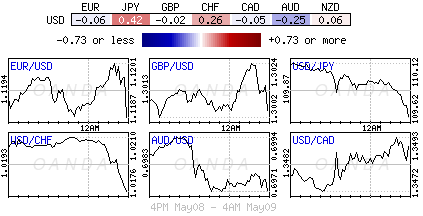

4. Rick aversion continues to dominate proceedings

Risk aversion theme has remained intact in the overnight session as US/China trade and Brexit talks looked increasingly more vulnerable.

USD/JPY (¥109.75) has tested its three-month lows below ¥109.60 as the Yen currency benefits from its traditional safe-haven status on market turmoil.

GBP/USD (£1.3001) tested below the psychological £1.30 level on speculation that PM May’s cross-party talks might not yield the positive results that many involved have been expecting.

Norges Bank gave a “hawkish” hold in key rate decision as it brought its forward the guidance on the next potential hike forward. EUR/NOK (€9.7895) tested below €9.78 level on ‘hawkish’ guidance.

Consensus believes that China will likely see its FX reserves continue to decline should Sino-U.S trade tension escalate, as the authority might intervene to defend the yuan against the U.S. China will be willing to tolerate some devaluation to offset the tariff impact on Chinese exports. Beijing may need to undertake further easing measures to bolster confidence and to stabilize growth. The dollar is up +0.4% at ¥Y6.8125 ahead of the onshore close.

BTC Bitcoin has rallied above $6,000 overnight for the first time in six-months, padding the rebound following November’s plunge and adding to optimism that the worst of the cryptocurrency market’s selloff might be over.

5. China inflation numbers – consumer and producer prices

Data overnight showed that China inflation picked up in April, but this was mostly due to supply-side factors and not stronger domestic demand.

Consumer price inflation rose to a six-month high of +2.5% y/y in April, up from +2.3% y/y in March and in line with expectations. The increase was driven by an acceleration in food price inflation, from +4.1% y/y to a three-year high of +6.1%.

Note: Disruptions to pork supply caused by African swine flu was mostly to blame – pork price inflation jumped to +14.4%.

Producer price inflation also picked up from +0.4% y/y, to a four-month high of +0.9%. This increase was partly due a growth in factory gate prices from +0.1% to +0.3%.

Note: Higher food inflation is expected to continue to push up CPI in the coming months, but, with economic growth unlikely to stage a strong recovery, the market does not see a higher PPI in the coming months.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019