Monday April 29: Five things the markets are talking about

Global equites are mixed at the start of this data laden and holiday interrupted week. The ‘big’ dollar is trading steady and Treasury yields have ticked a tad higher as investors wait for further clues on global growth with a plethora of data out from the U.S., Europe and China.

Note: Markets in Japan remain closed for Golden Week, with a number of other countries set to follow suit on May 1 (CNY, CHF, GER. Fr. & ITL).

Stateside starts with the Fed’s favourite inflation reports today (U.S PCE 08:30 am EDT). Any further softness would have investors increasing their bets on a Fed interest rate cut this year – futures are currently pricing in a +50% odds for the Fed to cut this September.

For many, the big event this week will be U.S Federal Reserve monetary policy meeting, its interest rate announcement and in particular, Chair Powell press conference – will he be standing by his recent ‘dovish’ outlook?

Elsewhere, the China’s Caixin PMI then follows for a second update on Chinese manufacturing, along with German retail sales (May 1) as well as the latest Bank of England (BoE) interest rate announcement (May 2) – Brexit seems to be temporarily on the back burner.

On Friday, U.S non-farm payrolls (NFP) is expected to round off the week with another solid report.

On the Sino-U.S trade front, Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin announced last week that they will travel to Beijing for trade talks beginning on April 30.

On tap: ANZ Business confidence (Apr 29), CAD GDP, consumer confidence & NZD employment change (Apr 30), Bank holiday – CNY, CHF, GER. Fr. & ITL, U.S ISM manufacturing PMI, FOMC monetary policy statement & CNY Caixin manufacturing PMI (May 1), U.K inflation report, BoE monetary policy statement & AUD building approvals (May 2), non-farm payroll (May 3).

1. Some stocks get the green light

On the whole, global equities are starting the week better bid after strong U.S Q1 economic growth, coupled with data showing profits at Chinese industrial firms grew for the first time in four months.

Note: Tokyo’s Nikkei was closed for a public holiday.

Down-under, Aussie Australian shares ended lower on Monday after losses in financial stocks pulled the benchmark down from its 12-year high as investors remained cautious ahead of bank earnings. The S&P/ASX 200 index closed down -0.4%, breaking its four consecutive days of gains. The benchmark gained +0.1% to close at its highest level since December 2007. In S. Korea, the Kospi index closed out up +1.7%.

In China, the blue-chip CSI300 index rose +0.3%, while the Shanghai Composite Index closed down -0.7%. Both indexes on Friday posted their worst weekly drop in 28 on policy support worries.

Note: Data on the weekend showed that profit at China’s industrial firms grew last month, rebounding from four-months of contraction.

In Hong Kong, indexes followed suit, the Hang Seng index rose +1.0%, while the China Enterprises Index gained +1.1% on stronger U.S and China data.

In Europe, regional bourses trade mostly lower on the open following a mixed session in Asia and slightly higher U.S Index futures. The Spanish IBEX is underperforming following the Spanish General Elections (see below) over the weekend.

U.S stocks are set to open in the ‘black’ (+0.8%).

Indices: Stoxx600 -0.03% at 390.74, FTSE -0.06% at 7,423.50, DAX -0.10% at 12,302.99, CAC-40 -0.01% at 5,569.11, IBEX-35 -0.59% at 9,450.27, FTSE MIB +0.18% at 21,776.50, SMI -0.02% at 9,722.00, S&P 500 Futures +0.08%

2. Oil falls after Trump presses OPEC, gold higher

Oil is starting the week under pressure, extending the end of last week slump, after President Trump demanded that OPEC+ raise output to soften the impact of U.S sanctions against Iran.

Brent crude futures are at +$71.66 per barrel, down -49c, or -0.7% from their last close. U.S West Texas Intermediate (WTI) crude futures are at +$62.87 per barrel, down -43c, or -0.7%, from Friday’s settlement.

Note: Both benchmarks fell around -3% in the previous session.

In typical Trump fashion, the U.S President told reporters that he called up OPEC and told them that gas prices must come down. The President’s actions, have at least temporarily, put a stop to crude oil’s +40% rally since the beginning of the year.

A good portion of oil’s rally occurred this month after Trump tightened sanctions against Iran by ending all exemptions that major buyers especially in Asia previously had.

Dealers have indicated that they are shifting their focus away from voluntary supply cuts, which have been led by OPEC since the start of the year, on the belief that “cooperation” may not last beyond a meeting between OPEC+ scheduled for June.

Also, Russia has indicated that it would be able to meet China’s oil demand needs – they wish to replace the imports it usually gets from Iran.

Note: Russia is also hoping to restore oil pipeline supplies to Poland and central Europe in a fortnight, after they were suspended last week over crude quality problems.

Ahead of the U.S open, gold prices trade atop of their one-week highs as the ‘big’ dollar comes under some pressure as the market focuses on soft U.S inflation data that overshadowed strong GDP numbers late last week. Spot gold is steady at +$1,285.59 per ounce, while U.S gold futures are also firm at +$1,287.70 an ounce.

3. S&P helps boost Italian bonds; Spain steady after vote

Starting the week on better footing, Italian government bonds have rallied after S&P maintained the country’s sovereign credit rating last Friday at BBB, calming some market concerns on a possible move into junk territory. Nevertheless, the ratings agency did maintain its ‘negative outlook’ on the eurozone’s third largest economy.

Italy’s 10-year BTP yield is down -5 bps to +2.53%, while the BTP/Bund spread is at +254 bps, its tightest in over a week and well-off last week’s two-month high of +269 bps.

Staying in Europe, Spanish PM Pedro Sanchez looks set to regain power after his Socialists overcame a challenge by right-wing nationalists in elections in Spain yesterday. Nevertheless, it looks very likely that he would need the backing of other groups to remain in office – potentially partnering with either the liberal party Ciudadanos or forming a govt with left-wing Podemos and Catalan separatists. There has been little immediate impact on Spain’s bond market, with 10-year bond yields flat at +1.03%.

Elsewhere, the yield on U.S 10-year Treasuries has gained +1 bps to +2.51%, the largest gain in a week, while in the U.K, the 10-year Gilt yield rose +2 bps to +1.161%.

4. Dollar happy to consolidate for now

USD continued to consolidate following last week’s GDP data. Although the Q1 growth beat expectations, both dealers and investors took note of the build in inventories and weaker-than-expected inflation component of the release. Any further weaker data, specifically inflation, could provide new pressure on the ‘big’ dollar.

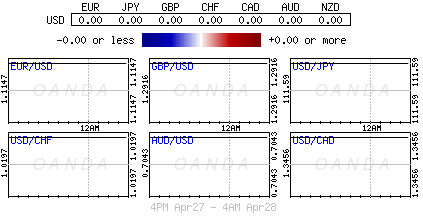

EUR/USD is steady at €1.1160 area with focus on a plethora of growth and inflation data for release over the coming week. Tomorrow, investors get to see the release of France, German and Spanish CPI along with Eurozone and Spanish Q1 GDP. Friday will see the Eurozone flash CPI readings.

USD/JPY (¥111.71) is a tad higher but remains below the psychological ¥112 handle. With Japanese markets closed all week due to the Golden Week holiday, expect price moves to dictated mostly by the lack of liquidity.

5. Eurozone lending to businesses slows

Data this morning showed that Eurozone bank lending to businesses slowed last month, following a brief pickup in February.

The ECB has indicated that lending to nonfinancial corporations grew at an annual rate of +3.5% after a revised rate of 3.8% in February – that is below the rates seen in H2 2018.

Note: For comparison, in 2007 and in the first half of 2008, bank lending to businesses was running at rates well above +12%.

Lending to eurozone households also slowed, too. Lending in the sector grew at an annual rate of +3.2% in March after +3.3% growth in February.

ECB’s Draghi had earlier indicated that “the central bank’s monetary policy measures, including a new series of targeted longer-term loans or TLTROS, would help to safeguard favorable bank lending conditions and will continue to support access to financing, in particular for small- and medium-sized enterprises.”

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019