Job vacancies fall

Australia’s Westpac leading index came in flat in February, falling from an upwardly-revised +0.1% reading in January, despite firmer commodity prices. In addition, skilled vacancies in February fell 0.9% m/m, escalating January’s revised 0.5% decline. The Australian jobs markets has been one of the more robust parts of the domestic economy, registering monthly average jobs growth of more than 30,000 over the past six months. Any signs of a peak in jobs activity could be detrimental to the Aussie. February’s employment report is due tomorrow morning.

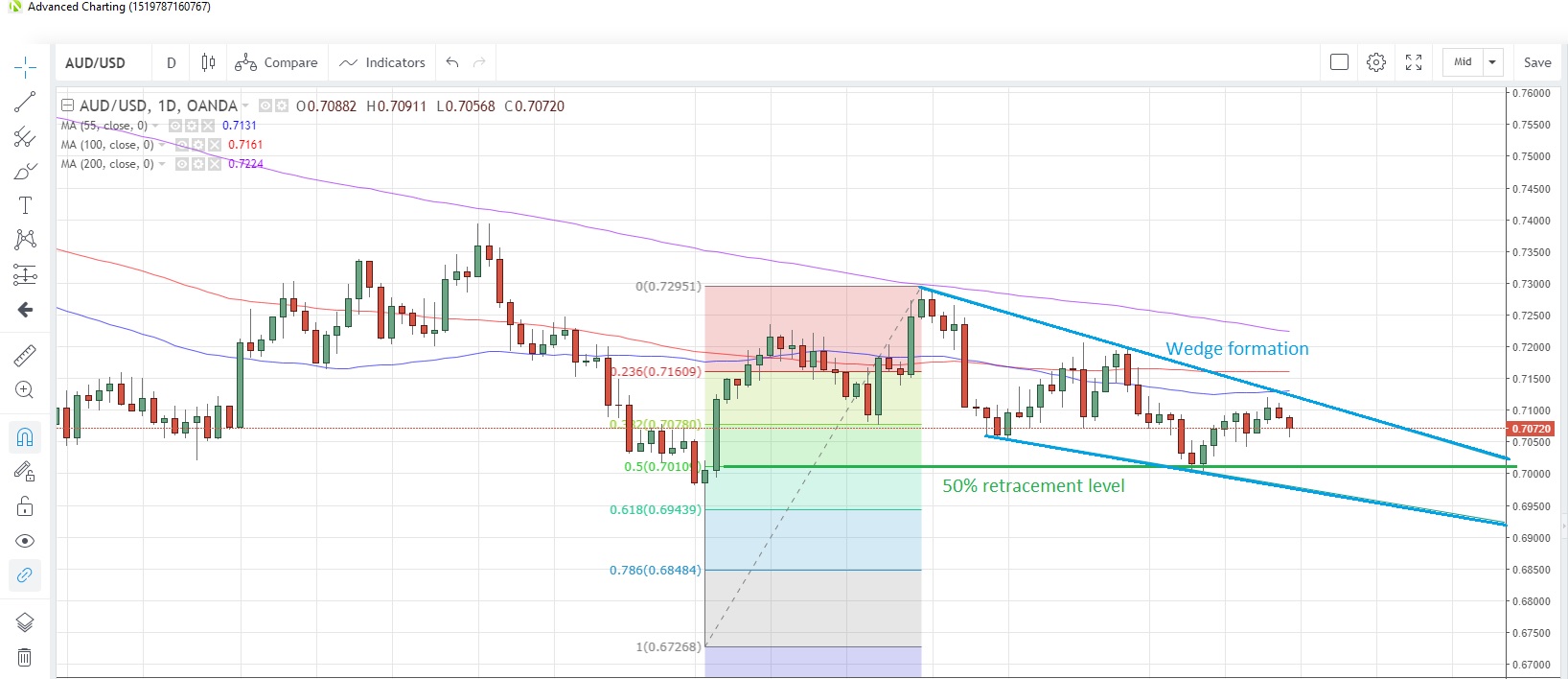

AUD/USD slid to a six-day low during the morning session, touching 0.7056. The FX pair seems to be shying away from the 55-day moving average at 0.7131, which has capped prices so far this month.

AUD/USD Daily Chart

Source: OANDA fxTrade

PBOC May cut Reserve Ratio in Q2

The China Securities Journal was speculating today that the central bank may cut banks’ reserve ratio requirements (RRR) in the second quarter of the year. The talk comes after PBOC governor Yi Gang said on March 9 that China’s financial sector faces challenges and the world economy is facing downward pressure. He added that there is room to cut the RRR to help reduce the risk of a sharper slowdown.

USD/CNH was barely changed today after the PBOC pushed the USD/CNY fix 39 pips higher to 6.7101, the first higher fix in three days. The FX pair is testing the upper bound of a downward channel which has been building since December. China shares were not impressed with the speculation, falling for a second straight day after touching a one-year high yesterday.

USD/CNH Daily Chart

Source: OANDA fxTrade

FOMC in the spotlight

The conclusion of the two-day FOMC meeting later today is likely to be less-dramatic than the past few times, with the Fed not expected to change rates, nor alter its stance on monetary policy going forward. The central bank is seen announcing the end of the asset roll-off from its balance sheet and the market will be anticipating an update to the projected number of rate hikes this year (if any). Market pricing is currently suggesting no hikes this year and a 34% chance of a cut by January 2020. An update to the Fed’s economic projections could be the only highlight for volatility.

Fed’s dovishness may depend on end of QT and inflation targeting

The rest of the calendar is populated with producer prices from Germany and the UK for February, together with the UK’s retail and consumer prices.

The full MarketPulse data calendar can be viewed at https://www.marketpulse.com/economic-events/

OANDA Senior Market Analyst Craig Erlam previews the week’s business and market news

Source: MarketPulse

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Andrew Robinson

Latest posts by Andrew Robinson (see all)

- RBA cuts rates on virus impact - 2 March 2020

- Commodities Weekly: Oil rises first time in eight days - 2 March 2020

- Daily Markets Broadcast 2020-03-03 - 2 March 2020