Tuesday September 18: Five things the markets are talking about

It was coming, the market new it was coming, just when, and how much, were the unknown variables.

President Trump has imposed an additional +10% tariffs on about +$200B worth of imports from China, rising to +25% by the turn of the New Year. Trump has threatened additional duties on about +$267B more if China contemplates hitting back on the latest U.S action, beginning next Monday.

Of course China is going to retaliate, but how, is part of the guessing game – “to protect its legitimate rights and interests and order in international free trade, China is left with no choice but to retaliate simultaneously.”

There are a few tech exceptions – which benefit Apple/Fitbit for now – and the tiered deployment is to help U.S companies find alternative supply chains. However, if the U.S needs to go to phase three, it would consume all remaining U.S imports from China and Apple products and its competitors would not be spared.

The problem for China is that they do not import enough U.S goods to go head-to-head with the U.S leverage strategy. They will want to cause U.S pain and will probably focus even more on the tech sector. Nevertheless, watch the Yuan’s value, it may be one of China’s strongest weapons. It has weakened by about -6.0% in the past three-months, offsetting any -10% tariff rate by a substantial margin.

From an asset price viewpoint, it’s been a rather ‘subdued’ reaction to Trump’s announcement. Buying U.S dollars in response to trade conflicts does not seem to be as appealing anymore. The delay in imposing +25% tariffs may explain the lack of movement, in addition to the fact that the tariffs have been widely anticipated.

1. Stocks mixed results

In Japan, the Nikkei rallied overnight to its highest close in seven-months, led by insurers thanks to rising U.S Treasury yields. However, no surprises, capping gains were electronic suppliers, which underperformed as the market weighs the new U.S China, tariff impact. The index closed out +1.4% higher, while the broader Topix rallied +1.8%.

Down-under, materials and energy stocks pushed Aussie equities lower as the escalating Sino-U.S trade war pressured commodity and oil prices. The S&P/ASX 200 index fell -0.4% at the close. The index rallied +0.3% yesterday. In S. Korea, the Kospi stock index closed +0.26% higher along with some of its regional bourses as Chinese markets largely shrugged off trade tariff threats.

In China, stocks staged a late rebound as the blue-chip index CSI300 rallied +1.9% as some investors bet that authorities will increase their investment in infrastructure to offset the impact of the latest tariff penalties from Trump. In Hong Kong, the Hang Seng index closed out +0.6% higher.

In Europe, regional bourses have shrugged off early weakness following the ‘telegraphed’ U.S tariff announcement after the yesterday’s U.S close. Autos lead the gains, while the materials sector and consumer discretionary are under early pressure.

U.S stocks are set to open in the ‘black’ (+0.2%).

Indices: Stoxx50 +0.5% at 3,363, FTSE +0.1% at 7,318, DAX +0.6% at 12,164, CAC-40 +0.6% at 5,383; IBEX-35 +0.4% at 9,446, FTSE MIB +0.2% at 21,148, SMI -0.3% at 8,908, S&P 500 Futures +0.2%

2. Oil prices fall as U.S-China trade war questions demand, gold lower

Oil markets have eased a tad as the Sino-U.S trade war questions the outlook for crude demand from the world’s two largest economies.

Brent crude futures have dropped -29c, or -0.37% to +$77.76 per barrel, while U.S West Texas Intermediate (WTI) crude is down -15c, or -0.22%, at +$68.76 per barrel.

U.S crude ‘bears’ believe that these tariffs are likely to limit economic activity in both China and the U.S – a hit to growth is a hit to consumption.

Note: Refineries stateside consumed about +17.7m bpd of crude oil last week, while China’s refiners used about +11.8m last month.

Crude ‘bulls’ are currently clinging to the potential supply cuts caused by U.S sanctions on Iran (third-largest producer in OPEC) as reason enough to support short-term oil prices.

Ahead of the U.S open, gold prices are under pressure as the ‘big’ dollar steadies amid concerns of an escalation in Sino-U.S trade tensions. Spot gold is -0.3% lower at +$1,197.51 an ounce, after rising +0.6% in Monday’s session. U.S gold futures are down -0.3% at +$1,202.20 an ounce.

However, if the ‘big’ dollar loses its ‘tariff haven’ appeal, expect the ‘yellow’ metal to find support on pullbacks.

3. Sovereign yields rally

U.S Treasury yields have backed up along the curve on growing expectations that the Fed could raise interest rates a few more times this year after recent data showed wages spiking last month, elevating concerns about inflation.

Note: U.S data last week showed that wages in August posted their largest annual increase in more than nine-years, rising +0.4% m/m and +2.9% y/y.

Yesterday, U.S 10’s touched +3.022%, the highest level in four-months, along with U.S 30-year yields at +3.159%. As to be expected, the short end rallied to a 10-year high, backing up to +2.799%.

Elsewhere, German Bund yields continue drifting upward to the +0.50% level amid better sentiment around Italy. The 10-year Bund yield is trading at +0.46%, up +0.05%. In the U.K, the 10-year Gilt yield has rallied +1 bps to +1.536%.

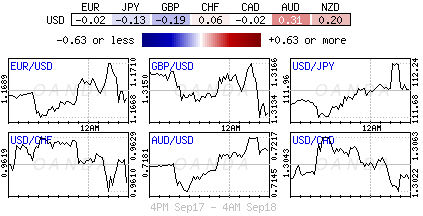

4. Dollar muted reaction

EUR/USD (€1.1680) shows a muted reaction to the U.S announcement that it will charge +10% on another +$200B of Chinese imports starting from next Monday. Typically trade tensions have been positive for the ‘big’ dollar; maybe attitudes will change once China shows its hand.

GBP/USD (£1.3126) pulls back from recent six-week highs as the market awaits Thursday’s E.U summit.

TRY ($6.3670) continues to weaken, down another -0.7% as investors remain confident in fading last weeks bigger than expected Central Bank of the Republic of Turkey (CBRT) rate hike.

An interest rate increase by the Norges Bank on Thursday is widely expected and already broadly priced into EUR/NOK (€9.5406). However, NOK bulls believe the central bank will likely signal more rate increases, which should provide further support for this commodity currency.

5. Reserve Bank of Australia (RBA) stays true to its ‘hawkish’ stance

In its minutes released overnight there were no surprises. The RBA maintained its interest-rate guidance in the minutes from its meeting a fortnight ago, reiterating that increases will eventually come amid anticipated economic strength.

RBA also noted that a number of G10 central banks, including the Fed, were expected to continuing rate hikes. This had been reflected in the markets, “most notably a broad-based appreciation of the US dollar” that “raised risks” for some, especially for “fragile emerging” markets. However, “the modest depreciation of the AUD was helpful for domestic economic growth.”

The copy and recent rhetoric suggests that Aussie policy makers remains highly confident its current stance – interest rates at record lows will ultimately bring lower unemployment, higher wage growth and an uptick in inflation over time.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019