European equity markets are expected to open around 1% lower on Friday, as similar losses in the U.S. weigh on investor sentiment as we head into the end of the week.

With a large amount of economic data to come throughout the European session though, traders will have to remain on their toes on Friday as things could get quite volatile. There are a number of tier one releases among those being released today which should make things interesting, not to mention the fact that earnings season is continuing in the background with a number of big companies reporting today. With all this going on, I wouldn’t be surprised to see some significant swings in the market throughout the day as investors respond to all the new information.

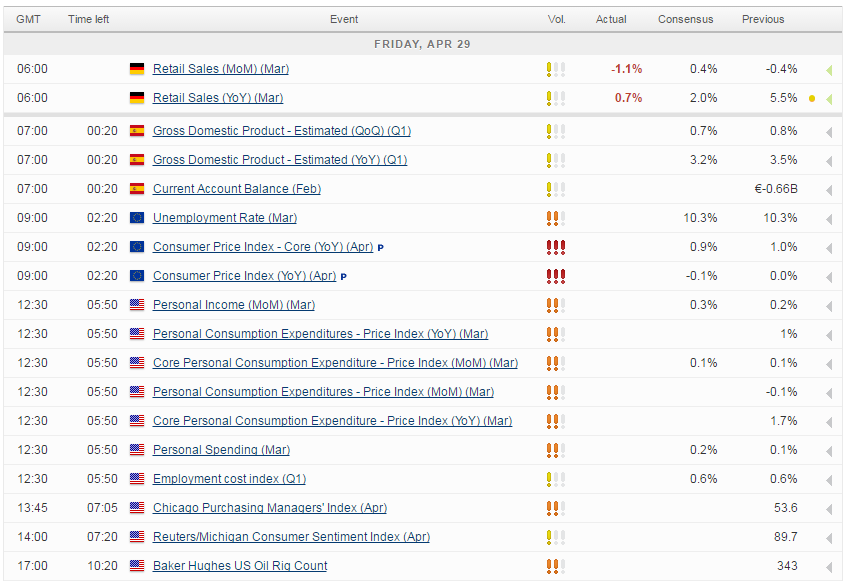

The economic data has already started flowing, with French preliminary first quarter GDP and German retail sales figures being released. It’s been a mixed start, with the French economy expanding by 0.5% in Q1, slightly ahead of expectations, while the Q4 reading was also revised higher by 0.1%. German retail sales on the other hand were quite poor, having dropped for a second month and recorded the largest decline since June.

Still to come this morning we’ve got flash GDP data from Spain, which is expected to record another quarter of impressive growth at 0.7%. The economy appears to be cooling though having peaked in the middle of last year and this would actually represent its slowest quarterly growth since the fourth quarter of 2014. Also to come from the eurozone we’ll get the latest unemployment number, which is expected to remain at 10.3%, and the preliminary reading of April’s inflation data, the headline reading of which is expected to dip back into negative territory despite the ECBs best efforts to stimulate the region.

There’s plenty more to come from the U.S. later, most notably personal income and spending data, as well as the Fed’s preferred inflation measure – the core personal consumption expenditure price index. Any uptick in the number here, which the Federal Reserve has indicated that it doesn’t expect, could see pressure rise on the central bank to raise interest rates in June given that it’s already close to target at 1.7%. We’ll also get UoM consumer sentiment data this afternoon and finally to cap things off this week, the Baker Hughes oil rig count.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024