No battle has been one, but, this market is looking to believe in something. There are many who think that the ECB is still needed to quell fears of contagion from the sovereign debt crisis. More so than ever, now that every FX trader has become a FI specialist and is currently inversely trading risk with periphery yields. Perhaps the ECB needs to reactivate its bond buying program to keep periphery yields down? Despite higher yields having spread to Italy ahead of tomorrows litmus test bond issue there, the ECB has but the program on hold and has stayed out of the market for the last 13-weeks. These periphery sovereigns require some breathing space. Their programs do not need to be swayed by capital market players who’s only aim is to make a fast buck.

Different asset class prices are being influenced by yields and with Spain being the instigator. Their country yields are coming off recent currency bloc highs this morning and remain at “highly stressed†levels as speculation continue to believe that the whole country will require a bailout and not just the financial sector. Italy it seems is along for the immediate ride. With many believing that this country is also in the cross hairs for external help is keeping their yields dangerously elevated. Most of the pull back in yields is not strategic, its mostly positional and some profit taking. Even Germany’s go to bund are being allowed some breathing space this morning. Despite dealers making room for supply in the market place, record low yields are becoming too rich a give up. The market fears that contagion could also sweep into Germany. However, just like treasuries, bunds belong to one of the safest and most liquid asset classes globally and are always in demand.

Euro data this morning is doing the region no favors. Factory output fell sharply in April (-0.8%), a strong indication that the market should expect the region to shrink again later this year and this after only narrowly escaping a recession in the Q1. Digging deeper, it’s no surprise to see that the periphery headliners of Spain, Portugal and Italy lead the decline. However, their powerhouse leader, Germany managed to see a pullback too. This will only raise more concerns about the regions ability to withstand the downturn. With very little else being reported in the range traded sessions, market focus will switch to US retail sales this morning. Noting cheery is expected with these numbers either. Many are looking for a bigger negative number of -0.2%, and mark the largest decline in two-years and should do very little to sway markets away from expectations of further monetary accommodation in the US. Everyone else is doing it, the Fed may as well get into the action!

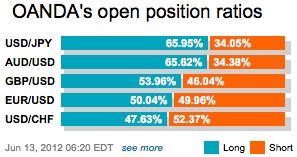

The retail sector have been the winners in this erratic trading environment over the past 24-hours. They went long yesterday and this morning they seem to have come over to the dark side and joined the masses by letting go these longs to net short the single currency. Event risk will have many wading to the sidelines, however, braver souls prefer to short this market, even if it currently feels better bid. Investors remain a better seller on rallies, looking to off load some EUR’s ahead of the psychological 1.26 handle. Their objective is to retest last weeks lows of around 1.2435. Through this strong support, downward momentum should pick up because of the plethora of stops parked here. Despite daily momentum remaining negative, and the nearer this weekend event risk is, the market will want to tighten up their overall exposure. Record shorts want a lower market, but, playing the percentages and lowering one’s exposure because of even risk will require higher prices first!

Other Links:

EUR, To Be Long or Short?

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019