One Year on and the Trump Effect in Stocks Has Not Worn Off

One year on from Donald Trump’s election victory and US equity markets are on course to open near record highs once again, having made stunning gains over the last 12 months – more than 30% in the case of the Dow and Nasdaq.

While many may claim that Trump’s achievements to date equate to very little given his difficulties repealing and replacing Obamacare, slower than expected progress on tax reform and minimal detail on fiscal stimulus, investors have clearly not been deterred as is evident by staggering gains in US stocks. Of course, much of this may still be conditional on the President delivering on the latter two in particular and some is also attributable to the rally in global equity markets over the same period, but the Trump trade is clearly still alive and well.

This is despite the fact that the Fed has raised interest rates three times since the election and is likely to do so again next month, which many will have believed could have threatened the economic recovery and with that, the stock market rally. That is clearly not the case and with the economy having now come off two quarters of around 3% annualized growth, one may wonder whether there is any need for the spending element of the President’s plan to revive the economy. There certainly doesn’t appear to be the desire for it that we’ve seen for tax reform over the course of the year.

DAX Under Pressure After Weak Corporate Returns

While political and geopolitical events have caused minor problems along the way, the rally has been very gradual and consistent with few hiccups along the way. In the absence of any major US economic events this week, Trump’s tour of Asia will continue to attract the bulk of the attention, although I imagine the rhetoric coming from the meetings and press conferences will be broadly in line with what we’ve heard already. Assuming no slip ups along the way and no unexpected back and forth with North Korea – which is possible given the country is one of the main topics of conversation – there’s little reason to believe we won’t see more of the same in the markets.

USD Consolidating But Further Gains May Lie Ahead

The US dollar has consolidated over the last couple of weeks since rebounding off its lows on the prospect of more rate hikes and tax reform progressing more smoothly than thought – albeit not as quickly as one would hope. The greenback is still looking bullish into the end of the year though and the appointment of Jerome Powell as Janet Yellen’s replacement as Chair should support this, particularly if he is accompanied by other hawkish appointments on the board.

From a technical perspective, the ECB meeting a couple of weeks ago triggered a move in EURUSD that was enough to push the pair through its head and shoulders neckline, which in the process drove the US dollar index through the neckline of its inverse head and shoulders. While this already looked on the cards, the break of the neckline would appear to be a bullish signal for the greenback in the weeks and months ahead.

Source – Thomson Reuters Eikon

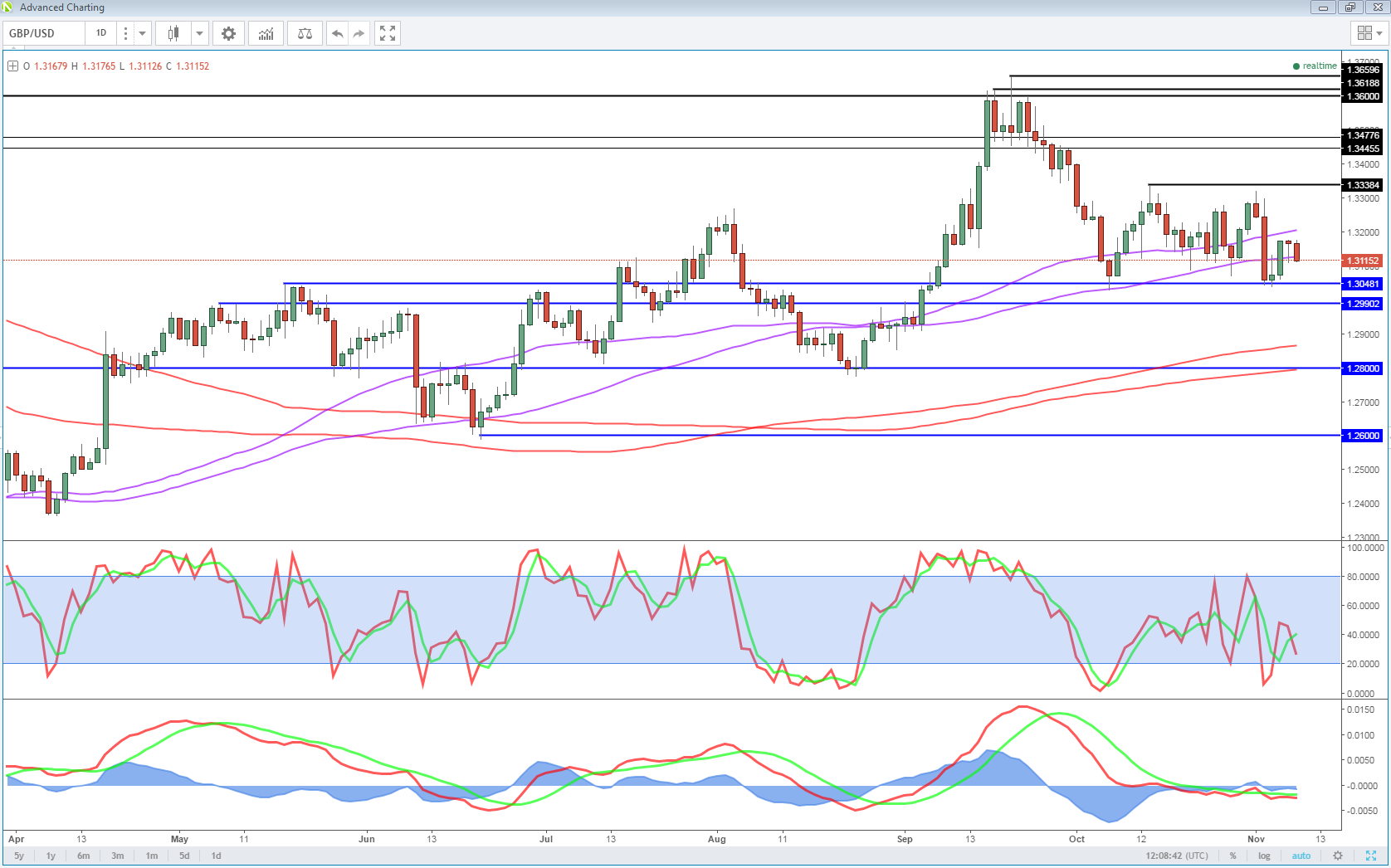

GBP Under Pressure as May’s Problems Mount

It’s been a relatively slow week for the markets so far, despite there being a number of concerning political stories than have the potential to cause further disruption down the line. The UK as ever is right at the top of this list, with Prime Minister Theresa May in the uncomfortable position of potentially being forced to sack another member of her cabinet at a time when her position is already seen by many as untenable in the aftermath of her disastrous election campaign.

Still, the softness we’re seeing in the pound today is likely more a reflection of the Bank of England’s decision to raise interest rates last week while adopting a dovish stance on future hikes. While much of the move was priced in on Thursday, we have seen a minor pullback since and I think today’s drop is simply a continuation of Thursday’s initial decline. The pound will face a big test around 1.30-1.3050 against the dollar should we reach those levels and a break of this could trigger a move back towards 1.28.

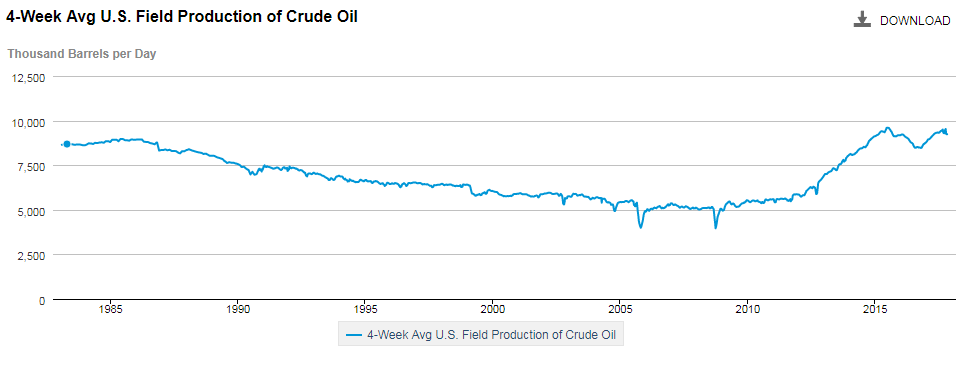

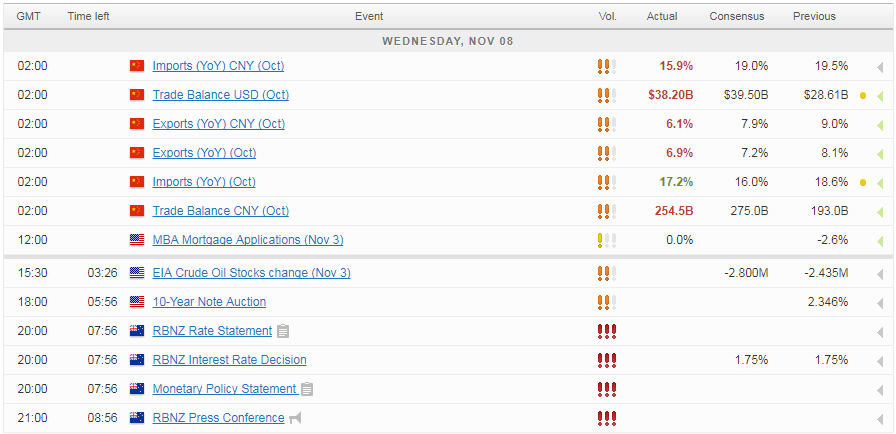

Oil Inventories Eyed as Oil Rally Continues

The one notable release today will be crude inventory numbers from EIA which come after API reported another small drawdown on Tuesday and as the political situation in Saudi Arabia – OPEC’s largest producer – becomes a growing concern. I don’t think this has been a big factor in oil’s recent rise given the talk of an output cut extension next year, growing demand forecasts and the stabilisation in US output.

Source – EIA

With momentum not slowing though there does appear to be more upside potential and the situation in Saudi Arabia may be supportive of this the longer is goes on.

EUR/USD – Euro Unchanged as Investors Search for Cues

Economic Calendar

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024