A six week winning streak in U.S. indices is on course to come to an abrupt end on Friday as this weeks’ commodity rout, likely combined with some profit taking in the absence of too much data, takes its toll.

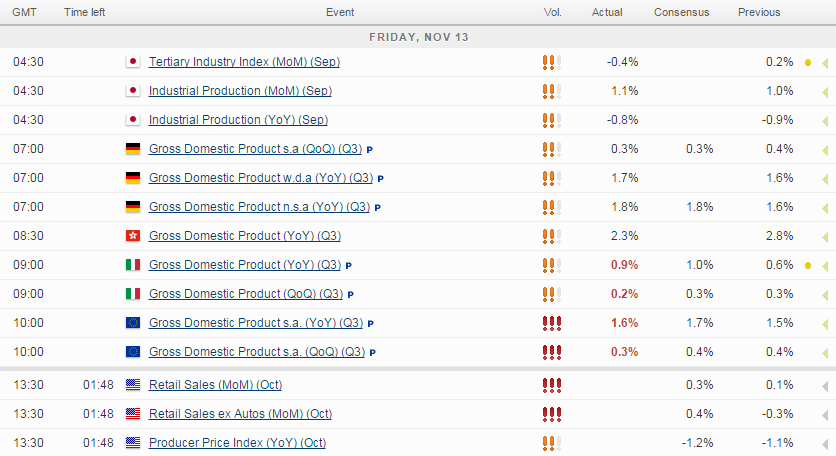

This morning’s GDP data from the eurozone has done nothing to lift sentiment in Europe having confirmed that sluggish growth continued in the third quarter. The 0.3% growth the region did scrape appears to have largely been driven by higher domestic demand as consumers take advantage of the low inflation environment. While this is encouraging, the deterioration in manufacturing is a concern as it makes up around a fifth of the economy and is showing little sign of recovering. The slowdown in emerging markets is clearly hurting the euro area, given that it is responsible for around a quarter of all its exports, and the weak euro isn’t doing enough to drive higher demand. Under the circumstances, there is clearly a need for further monetary easing from the ECB and based on recent comments from Mario Draghi, that is still likely to come in December. The euro has weakened dramatically against the dollar on expectations that the Fed will raise rates in December but it appears this is not enough for the ECB to reconsider and a rate cut alongside additional bond buying in December now looks likely.

The consumer will remain in focus today, with the latest retail sales and consumer sentiment figures from the U.S. being released. The consumer is extremely important to the U.S. economy, with personal consumption making up more than two thirds of total U.S. output. Retail sales this year have broadly disappointed with increased disposable income from lower oil prices failing to provide much of a stimulus. Subdued wage growth appears to be behind the lower levels of consumer spending and I’m sure the Fed would love to see signs of this improving before it raises rates in December. Following last month’s 0.3% decline in core retail sales, we’re expecting to see a 0.4% rise for October, which would be only the third time this year that we’ve seen such growth. Consumer sentiment has been near all-time highs this year despite the weaker retail sales, although the trend has definitely been softening. This is expected to rise to 91.3 today from October’s downwardly revised 90 reading.

EURUSD

The euro has come under pressure against the dollar this morning as weaker GDP figures and ongoing expectations of December easing weigh on the single currency. The pair had paired last Friday’s losses over the course of the week but ran into resistance around 1.0830 which had previously provided support for the pair. While I wouldn’t write off the potential for a broader correction in the pair given the significant losses experienced over the last month, there remains a substantial bearish bias in the markets and as we approach the end of the year, I would expect much larger losses to come. I think only a U-turn from the Fed or ECB would prevent the pair reaching parity by the end of the year. A strong retail sales report today could build on today’s bearish move and help drive the pair back towards Tuesday’s lows, with a break of this potentially opening a move back towards 1.0520 – April lows.

WTI Crude

WTI extended is losing streak to seven days on Thursday and in the process broke and closed below what had been a key support region throughout September and October. While we are seeing some consolidation today, the outlook for WTI once again looks quite bearish and August lows around $37.25 may now be eyed. Along the way, it may run into support around $40, $39.30 and $38, but given the ongoing oversupply story, reports of storage units nearing capacity and Iran possibly filling any gap left by U.S. production slowing, I see no reason right now for it not to be trading back at August lows in the coming months.

The S&P is expected to open 3 points lower, the Dow 39 points lower and the Nasdaq 11 points lower.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024