A positive session in Europe and Asia overnight, including a strong rally in China, is failing to lift U.S. futures ahead of the opening bell on Wall Street on Wednesday.

It appears that tomorrow’s Federal Reserve decision is possibly weighing on risk appetite in the U.S.. Risk aversion is not unusual ahead of such a big announcement or release and this is being touted as the biggest Fed announcement in years.

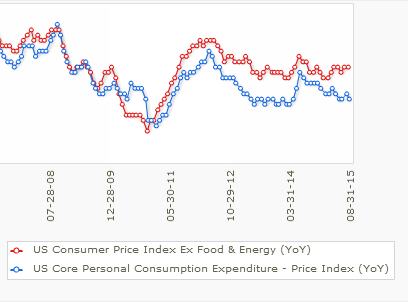

One thing that could get a reaction today is U.S. inflation data, given that this is the main concern holding back the Fed from hiking rates at the moment. It should be noted that the CPI reading is not the Fed’s preferred measure of inflation and the core reading is some way above the core personal consumption expenditure price index. That said, they won’t necessarily ignore the release and if we see evidence that inflationary pressures are picking up or easing off further, it could sway the decision.

This is the last of the major economic releases before the decision so there is potential to see quite a sharp reaction to it if it goes against expectations, especially if significantly so. Another disappointing reading in particular could have a big impact with the markets only pricing in around a 25% chance of a rate hike tomorrow.

The pound was given a real boost from the U.K. jobs report this morning, which pointed to ongoing and sustainable improvements in the labour market. Falling unemployment and higher wages are undoubtedly what will grab people’s attention and right so.

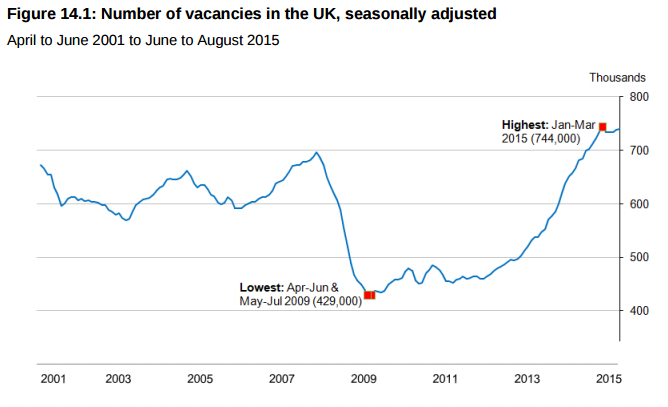

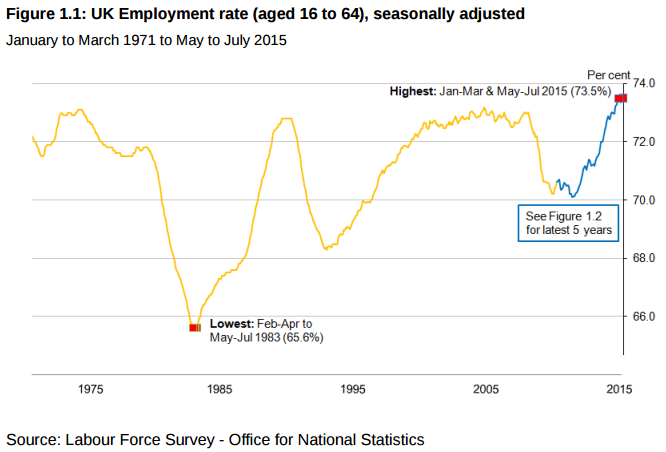

But even some of the lesser tracked gages such as job vacancies and working age employment support the view that the rise in wages is sustainable.

Source – ONS UK Labour Market Report

It could even be argued that there is a more compelling case to raise rates in the U.K. than in the U.S..

GBPUSD – rallied strongly on the back of the release breaking back through 1.54, having previously looked on the more bearish side and traded near one week lows. The pair faces some resistance now around 1.5420 and a failure to break through this could lead to a rather bearish head and shoulders setup at which point 1.5330 will be a key support. Above 1.5420, 1.5480-1.55 will be a key resistance for the pair. Given the positives associated with the jobs report, the path of least resistance may lie to the upside.

The euro fell quite considerably against the pound in following the release but this move was helped half an hour later by the weaker than expected inflation reading for the eurozone. With inflation remaining low in the eurozone and the stronger euro on the back of safe haven flows not helping matters, the chance of further stimulus from the ECB is growing, which could act to weaken the euro in the coming months.

EURGBP – fell back below 0.73 following the data this morning and could face further losses as the day progresses. The pair has been range bound for almost a month now with 0.74 providing resistance to the upside and 0.7240 support below. Given the new momentum gained this morning and the inability of the pair to gain any above 0.7350 this week so far, we could see 0.7240 come under pressure once again. This is a significant support which if broken could prompt another strong move to the downside, with 0.7150 being the next key support level.

EURUSD – also experienced some weakness in the aftermath of the eurozone inflation release, falling to 1.1225 – a six day low – where it is now finding support. This is a key short term support level and a break could bring 1.1150 into focus. Below here, 1.11 is key as this takes us back to September lows. Given the rejection at 1.14 earlier this week, a break below 1.11 would be longer term bearish, potentially opening up a move back towards 1.10 initially.

The FTSE wasn’t quite so positive in response to the U.K. data, in fact it actually pulled back following the release before quickly reversing these losses to trade at new daily highs, in line with the broader market. It’s worth noting here that while we may have got initial negativity to this as rate rises are seen as being negative for equity markets, especially what’s perceived to be premature ones, the overriding driver of the FTSE is not the U.K.. The FTSE is a global index and when the broader market is higher and the Chinese markets rallied strongly overnight, a strong jobs report is unlikely to hold it back for long. The latter are the main drivers despite small temporary moves.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024