While investors will primarily continue to be focused on tomorrow’s highly anticipated Federal Reserve announcement, there is once again a lot of important economic data being released today which will offer a temporary distraction.

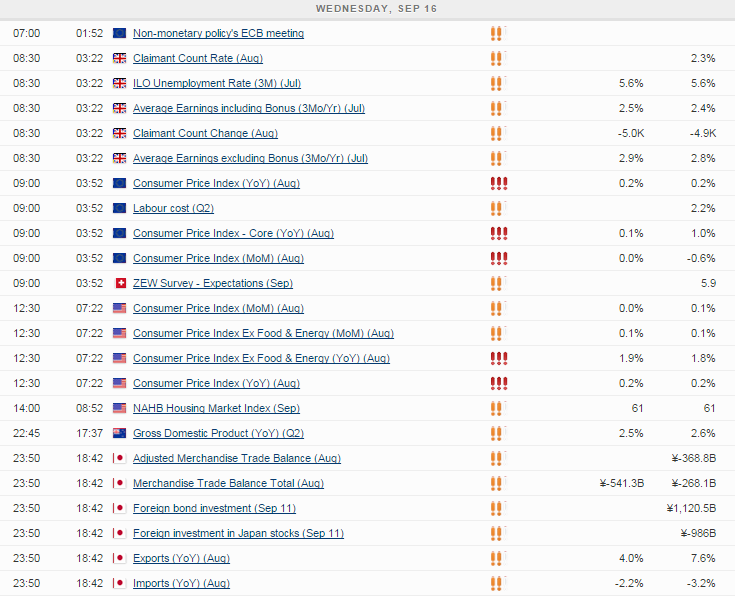

U.K. jobs data will be released this morning and once again, the earnings component of the report is going to be of most interest. As in the U.S., the U.K. finds itself in a position in which unemployment has fallen back to a very low level and yet wage growth has remained frustratingly subdued. In this already challenging inflation environment, price growth has therefore remained very low creating a headache for the Bank of England.

Wages are expected to have grown by 2.9% in the three months to July, a slight increase on last month and consistent with the improvements seen over the last 12 months. Including bonuses this is expected to be slightly lower at 2.5%. Unemployment is expected to have remained at 5.6%, not far from the pre-financial crisis levels.

If momentum continues in the labour market as it has over the last 12 months, the BoE could be tempted to raise rates early next year which is currently earlier than the markets are expecting. The central bank is clearly getting closer to this point now, although recent activity in emerging markets related to China and the prospect of a Fed rate hike may slow them down a little as they wait to analyse all the data.

Final eurozone CPI figures for the eurozone will be released this morning and are expected to be unchanged at 0.2%, with the core reading remaining at 1%. While the figures are being weighed down by falling commodity prices, other downward price pressures exist that may encourage the ECB to add more bond buying in the coming months. The euro emerging as an apparent safe haven hasn’t helped matters, pushing it to 1.13 against the dollar, neither has the turmoil in emerging markets which could hit exports, particularly in Germany.

The Fed will begin its much anticipated two day meeting today, with the announcement, along with statement, press conference and economic projections coming tomorrow evening. Markets are currently pricing in only a 25% chance of a rate hike at this stage but they have been wrong when it comes to the Fed on many occasions in the past, so I expect some of this caution that we’re seeing in the markets to persist.

Today’s CPI reading may have only a small bearing on the outcome as it is not their preferred measure of inflation. That said, it is expected to show the downward price pressures are very much still there, with overall prices rising by only 0.2% year on year. That said, the core reading is expected to rise to 1.9% from 1.8% previously, only marginally below the Fed’s 2% target. It’s preferred measure is still some way below this still though so I don’t expect it to hugely influence their decision making over the next couple of days.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024