A negative session in the US and Asia overnight is looking to weigh on European markets ahead of the open on Thursday, with futures currently pointing to a slightly lower open across the board.

We have now approached the business end of the week in the markets and I’m expecting investors to start getting a little anxious. There are a number of risk events in the coming days that could have big impacts on the markets – UK election today, US jobs report tomorrow and negotiations with Greece entering a crucial stage – so we’re likely to see investors being a little more cautious than normal.

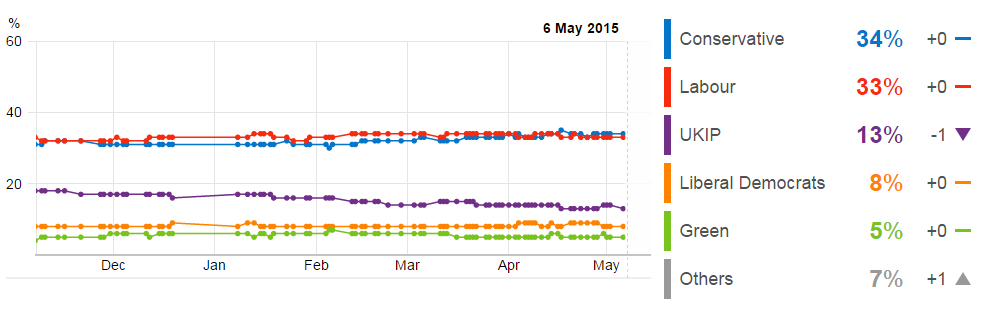

After weeks of campaigning, the UK will head to the polls today in what is expected to be the closest fought election in decades. The polls have barely changed in recent months and still show the Conservatives and Labour neck and neck with around a third of the votes each meaning both will be a long way from securing a majority.

*A combination of all major polls from the BBC’s poll tracker page.

This creates a lot of uncertainty that could weigh on the markets today. This is particularly true for the pound as today’s result will have an impact on growth expectations, interest rate forecasts and whether we’ll get a referendum on EU membership. The stakes are pretty high. The FTSE will be less impacted due to the global nature of many of the stocks in the index making it less sensitive to political changes at home.

There’s so many possible outcomes of the election with, for example, a Conservative UKIP coalition offering something very different to a Labour SNP one. Not only is this the closest fought election in years, it also offers the potential of two very different governments for the next five years. It will be very interesting to see how investors react over the next 24 hours or so.

For more information on the election, the possible outcomes and how the markets could react, check out our election preview and analysis.

Greece may have managed to repay €200 million to the IMF yesterday and stay afloat for now, but the country is fast running out of money and there are serious doubts that it will be able to repay another €763 million when it comes due on Tuesday, the day after the next eurogroup meeting.

Negotiations are not progressing as hoped despite the daily talks between the different parties. It’s not even clear at this stage whether the IMF and EU are on the same page after it was reported that the IMF wants the EU to accept writedowns on Greek debt as has become unsustainable. This could slow negotiations further which really isn’t helping matters.

On the bright side, the ECB yesterday extended the emergency liquidity assistance to Greek banks and didn’t apply any new haircuts on the Greek assets the banks are using as collateral. This may change going forward but I imagine that will depend on how talks progress between now and Monday’s meeting. If this does carry on into the weekend, we may see a lot of risk aversion tomorrow as a lot can change in the two days the markets are not open.

The FTSE is expected to open 8 points lower, the CAC 11 points lower and the DAX 15 points lower.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024