US Treasuries received a huge boost yesterday following the postponement of the impending defaulting event on 17th October. Stock prices rallied strongly, with risk appetite broadly higher. However, yields actually decreased despite the increase in stock prices, as Fixed Income traders re-entered the market believing that US is at least one step closer to resolving the Debt Ceiling crisis which has resulted in at least one big name institution selling their existing Treasuries holdings.

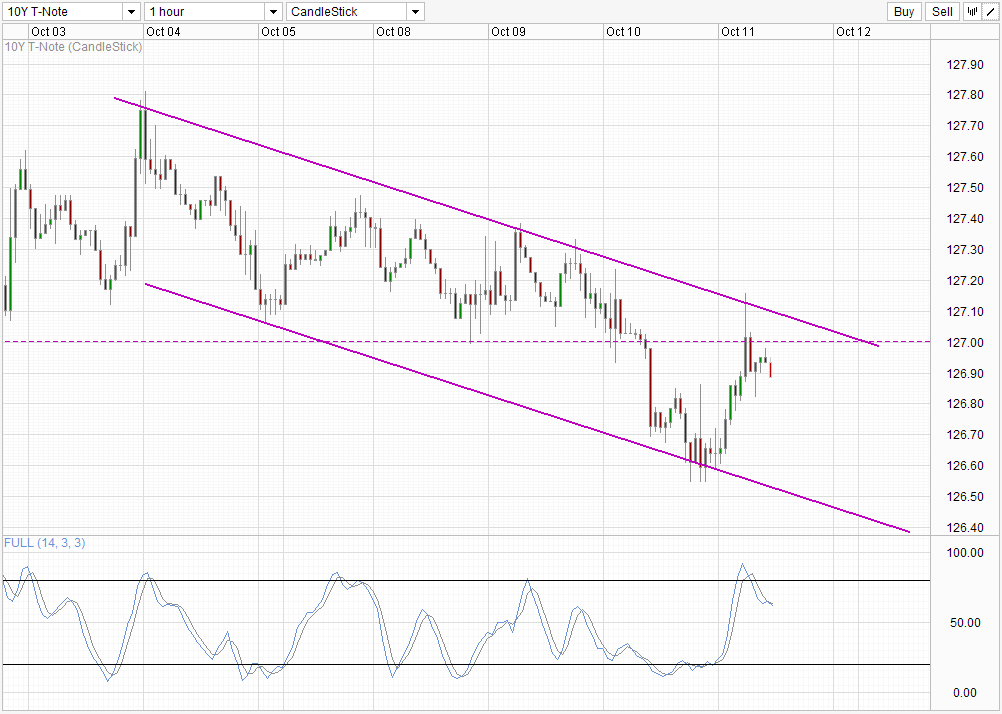

Hourly Chart

Looking at prices of the 10Y benchmark T-Note, yesterday’s rally – though strong which was also fundamentally supported, wasn’t able to shake off the strong technical influence it is under right now. Both the lows and the highs of yesterday’s US session were kept within the descending channel, with 127.0 round figure keeping pressure on bulls as well. This suggest that the short-term trend continues to be lower, and price action agrees, with selling activities spotted during Asian hours and Channel Bottom opening up as a bearish target. There could be potential acceleration lower should 126.8 – 126.85 intraday support is broken. Stochastic indicator echoes the same view, with Stoch curve breaking below 80.0 in conjunction with the holding of 127.0 resistance, giving us a bearish cycle confirmation.

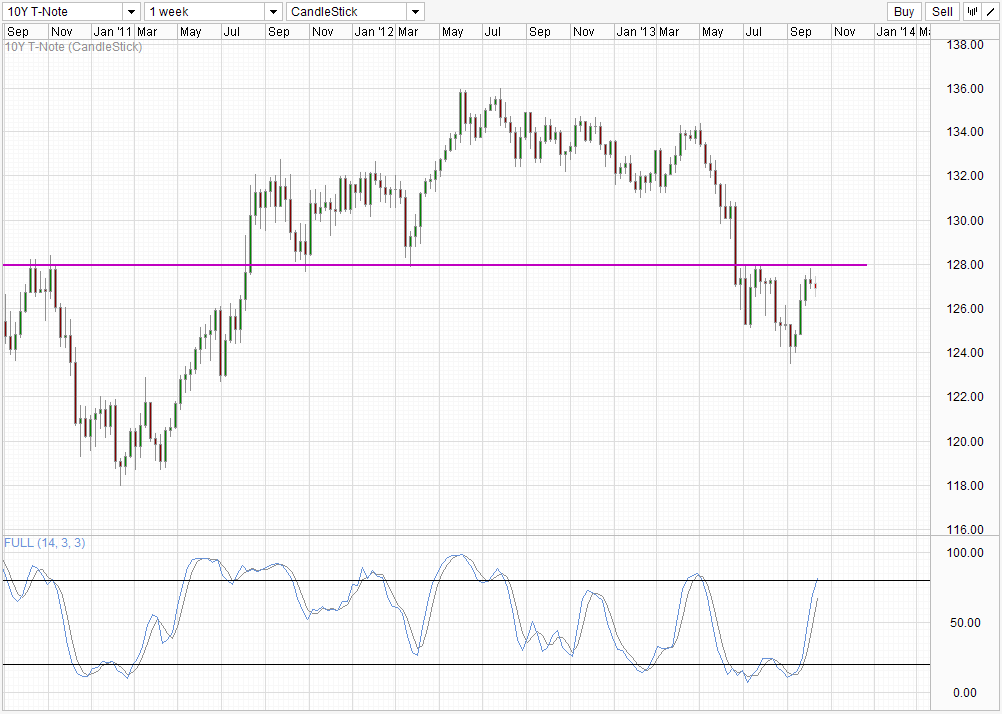

Weekly Chart

Long term outlook also favor lower prices (higher yields), with the short-term bearish momentum part of the bigger bearish momentum from the 128.0 rejection. Similarly, Stochastic indicator on the Weekly Chart also favor future bearish movements, as readings are already within the Overbought region but Stoch curve has yet to form a top. This is actually a good thing for bears who already have short positions, as it suggest that bearish momentum may be able to push lower much lower when the bearish signal appears eventually. For those bears who have been on the sideline, they may need to wait for price breaching 126.0 and preferably 124.0 coupled with a Stoch peak in order to have their entry signal.

Fundamentals also support both short-term and long-term declines. What US politicians have done is basically kick the can 6 weeks later, and should everything remain in square one, we could possibly see default fears coming back in within the next couple of weeks which will drive 10Y prices lower once more. Long-term wise, the recent appointment of Yellen as Fed Chairman does not change the fact that we are looking at the end of QE3 in 2014, with some Fed members wanting it to happen as early as mid 2014. If QE purchases are tapered and stopped, we will be losing a huge chunk of Treasuries purchases which will definitely drag prices lower from where we are now. This decline will almost certainly happen as this is a fundamental demand issue. Despite speculators already expecting that this would happen and may have even started selling months ago, the moment QE taper starts, there will be an immediate demand void which will pull prices down. The only question remaining is whether Treasuries prices will continually drop further, and not whether a buy the rumor/sell the news behavior will happen.

More Links:

GBP/USD – Relying on Support at 1.5950 Level

AUD/USD – Remains Subdued with Solid Support at 0.94

EUR/USD – Finds Solid Support at 1.35

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014