So close yet so far, yields of US10Y hit a high of 3.0328% on 31st Dec but there wasn’t any strong breakout despite crossing the supposed line in the sand. Instead, yields starting falling steadily in the month of January, reaching a low 2.6694% on the final day of Jan trading, erasing all the gains and more earned in December.

The major culprit for this decline in yield is obviously the risk aversion flow. Certainly market seeking safer assets such as long dated treasuries should not be a surprised when there are hints of a strong bearish stock correction. But what is interesting is that even a surprise QE taper by the Fed last week failed to drive yields higher, with demand for safety assets outweigh the drop in future Fed purchases.

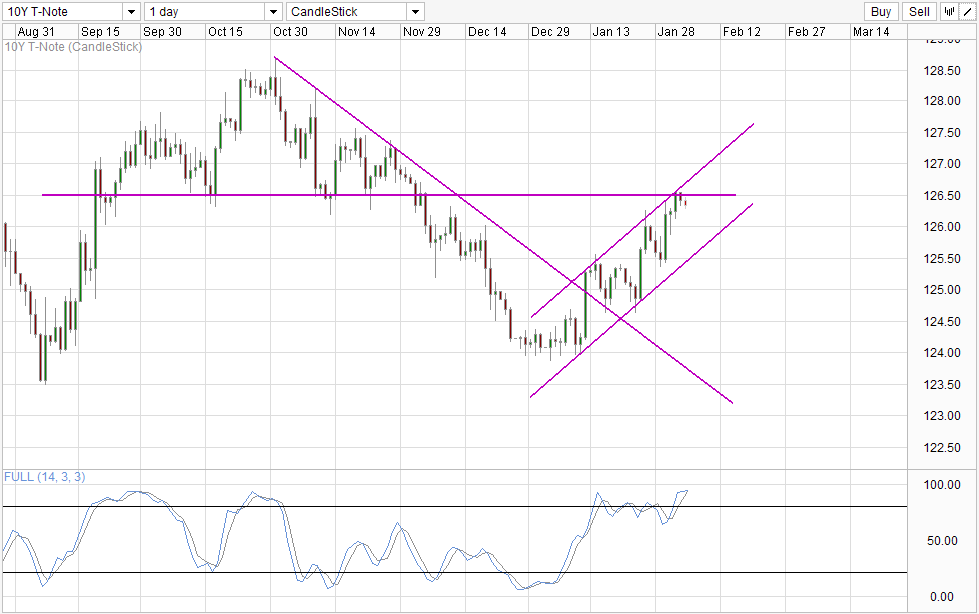

Daily Chart

From a fundamental perspective, there is no way that private investors will be able to buy enough treasuries to overcome the decline in Fed purchases. Perhaps the market is able to do it right now, but as the cut gets deeper, it will be impossible for the market to buy an additional $10 billion worth of treasuries every month just to maintain current yield levels. As such, yields should still revert back from current unnaturally low levels to rise up to the modern average range between 4.5 – 6.0%.

In fact, there are already signs of pulling back – 10Y prices are facing difficulty breaking the 126.50 resistance and confluence with the rising Channel Top. Stochastic readings are also deeply Overbought. Stoch curve have yet to point lower but the gap between Stoch/Signal has narrowed and a cross appears to be likely. All these point to a bearish reversal which opens up a move towards Channel Bottom and 125.5 round figure support.

However, it should also be noted that the same argument used to justify higher yields can also be used when 10Y prices showed signs of topping back on 13th and 24th Jan. The only difference between then and now is that Treasuries purchases have been cut by $5 billion then versus the $10 billion now. This may seem significant, but it should be noted that the cut was only announced last week, and it is unlikely that the fundamental impact can be felt immediately especially since the difference would also be spread out across the entire month. Hence, we should not underestimate the bullish risk aversion strength that had foiled 2 bearish pullback attempts. The implication is that prices may have higher likelihood of rebounding when the aforementioned support levels are tagged, and in the most extreme bullish scenario a break of 126.5 cannot be ruled out especially if risk aversion continue to worsen.

More Links:

WTI Crude – Bullish Momentum Intact Despite S/T Bearishness

S&P 500 – Feb to Follow Jan Into The Red Sea? Recent History Says Yes.

Gold Technicals – Staying Supported By Risk Aversion Flows

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014