European futures are looking a little mixed ahead of the first trading day of the week as the uncertainty surrounding Greece’s future in the eurozone continues to grow. Focus this week will also be on Asia where a number of economic reports will offer fresh insight into Japan’s flagging recovery and China’s efforts to stave off a hard landing.

Greece’s decision on Friday to bundle together four repayments due to the International Monetary Fund this month into one due on 30 June has bought the country a little bit more time at the negotiating table with its creditors. That said, given how talks have gone so far, I struggle to see what good that will do as neither side is showing any appetite to budge on key issues of pension and labour market reform and VAT.

Greek Prime Minister Alexis Tsipras took to parliament on Friday to lambast its creditors approach to the negotiations, labelling the latest proposal “absurd” which will no doubt have ruffled a few feathers. There needs to be some compromise from both sides, albeit probably much more from Greece being the debtor country, otherwise I fear we could be seeing them walking blindly towards disaster.

The institutions have already come round to the idea of lower primary surpluses but I don’t see them budging on other key issues unless Greece comes up with a credible alternative. Tsipras is also pushing for debt relief and while most agree this will happen at some point, it seems unlikely now as it would have little to no chance of being passed through the parliaments of creditor countries while further bailouts are being discussed.

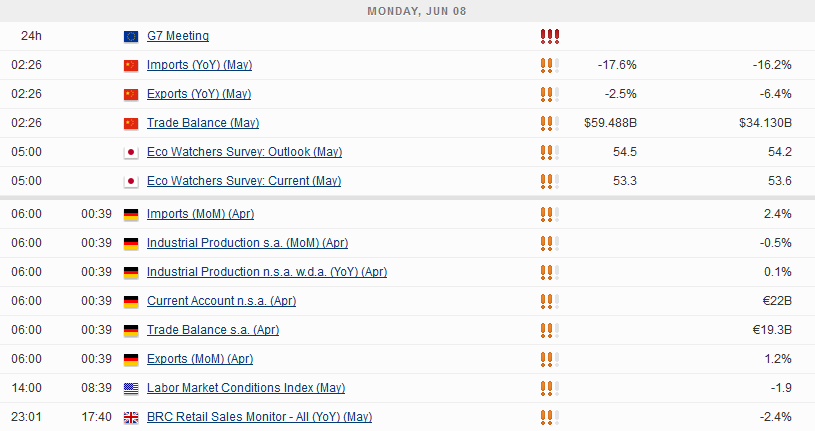

There isn’t much data coming from Europe this week, barring a few minor reports. Today we’ll get industrial production and trade balance figures from Germany, as well as the Sentix investor confidence reading for the eurozone. The key data release this week will be U.S. retail sales on Thursday as consumer spending has been a key thing missing this year despite a growing disposable income. We need to see spending picking up if the Federal Reserve is going to have enough confidence in the economy to raise rates.

There is lots of data coming from Asia this week, so China and Japan in particular will be a key focal point. Overnight there was some good news for both countries as China’s trade surplus ballooned to $59.5 billion, close to February’s all-time high of $60.6 billion. The boost was primarily driven by a 17.6% decline in imports which does tarnish the data as it raises serious questions about domestic demand in a country that’s trying to move towards a consumption driven economy.

Japan’s first quarter GDP reading was revised significantly higher offering some optimism for this year. The economy grew by 1% in the first quarter, 3.9% on an annualized basis, which was well ahead of expectations and a big revision on the preliminary reading. The revision was mostly driven by higher capital spending which will be music to the ears of the government. Consumption was also higher which may suggest that after a year of trauma following the sales tax hike, the consumer may finally be adjusting. The question now is whether this can all lead to higher wages and inflation, which has been notoriously hard to come by.

The FTSE is expected to open 8 points higher, the CAC unchanged and the DAX 27 points lower.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Craig Erlam

His views have been published in the Financial Times, Reuters, The Telegraph and the International Business Times, and he also appears as a regular guest commentator on the BBC, Bloomberg TV, FOX Business and SKY News.

Craig holds a full membership to the Society of Technical Analysts and is recognised as a Certified Financial Technician by the International Federation of Technical Analysts.

Latest posts by Craig Erlam (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024