The DAX has ticked higher in the Friday session, as the index trades at 12,610.50. On the release front, there was just one event out of the eurozone. Retail PMI improved to 52.7, its highest level since July 2015. In the US, the focus is on employment numbers, highlighted by nonfarm payrolls and wage growth. Nonfarm payrolls dropped to just 98 thousand in March, but is expected to rebound to 194 thousand in the April report.

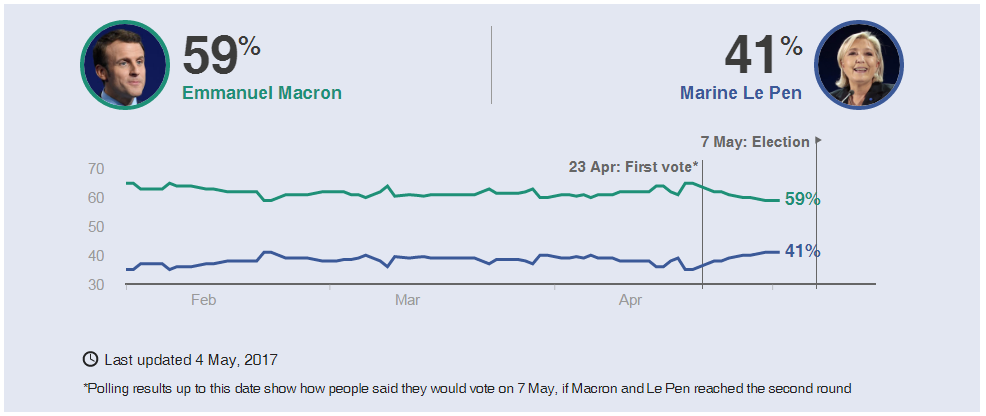

All eyes are on the French presidential election, which will be held on Sunday. Despite a turbulent campaign with plenty of mud-slinging to go around, opinion polls continue to point to a decisive victory for centrist Emmanuel Macron over far-right candidate Marine Le Pen. The two squared off in a testy television debate on Wednesday, with Macron widely considered to have won the debate. Throughout the week, polls have shown Macron holding comfortable lead of 20 points over Le Pen, and the euro climbed to 6-month highs on Thursday, as the markets are clearly confident that the polls are on track and that Macron will win. Still, many voters don’t like either candidate and remain undecided, which means that the polls may not be as accurate as they were in the first round. If Le Pen loses but does much better than predicted, we could see European stock markets lose ground.

Macron has Euro Markets on Firm Footing

Source – BBC

The polling average line looks at the five most recent national polls and takes the median value, ie, the value between the two figures that are higher and two figures that are lower.

Source – BBC

French Election Timeline

May 3 – TV debate between the two remaining candidates

May 5 – [from midnight] Poll blackout

May 7 – Second round of French presidential elections. Last polls close at 19:00 BST / 14:00 EDT, with an exit poll result announced immediately.

May 11 – Official proclamation of the new President.

May 14 – [from midnight] End of Francois Hollande’s mandate

June 11 – First round of legislative elections

June 18 – Second round of legislative elections.

As expected, the Federal Reserve stayed on the sidelines on Wednesday, holding the benchmark rate at 0.75 percent. The Fed rate statement was hawkish, as policymakers emphasized the positives and downplayed a soft first quarter. The statement noted that consumer spending remains strong and that inflation was “running close” to the Fed’s 2 percent target. The Fed’s message is clearly one of optimism, as the central bank remains on track to raise interest rates twice more in 2017. The Fed’s bullish statement immediately raised the likelihood of a rate hike at June meeting, which jumped to 74 percent after the statement, up from 63% before meeting. The Fed has two key goals which have been achieved, namely full employment and an inflation rate of 2%. One area of concern is the balance sheet, which stands at $4.5 trillion. The minutes of the March meeting stated that policymakers want to start reducing this figure before the end of 2017, and we could see another reference to the balance sheet in the April minutes.

Economic Calendar

Friday (May 5)

- 4:10 Eurozone Retail PMI. Actual 52.7

- 8:30 US Average Hourly Earnings. Estimate 0.3%

- 8:30 US Nonfarm Employment Change. Estimate 194K

*All release times are EDT

*Key events are in bold

DAX, Friday, May 5 at 4:50 EDT

Open: 12,634.50 High: 12,628.50 Low: 12,600.00 Close: 12,610.50

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Kenny Fisher

Latest posts by Kenny Fisher (see all)

- AUD/USD jumps after Fed says rate hike unlikely - 2 May 2024

- Canadian dollar edges higher as Fed pauses again - 2 May 2024

- USD/JPY slides – did Tokyo intervene? - 2 May 2024