The G-20 meeting at the weekend had something for all commodities. News of a 90-day truce in the US-China trade war helped the agricultural sector, while metals benefited from the US dollar’s slide. Oil prices soared after Saudi Arabia and Russia agreed to extend their pact to manage the oil market into 2019, raising the prospect of official production cuts at this week’s OPEC meeting.

Energy

CRUDE OIL prices are higher this week on the back of the G-20 developments. Now all eyes are on Thursday’s OPEC meeting to see if production cuts are announced. Canada has already announced some production cuts post-G-20, with Alberta, the country’s largest oil producing province, announcing an unprecedented cut of 325,000 barrels per day (bpd). Yesterday, Qatar announced that it will leave OPEC on January 1 2019 to focus on its gas production. As a result, it will no longer be bound by OPEC’s agreements.

WTI is now at $53.46 and is looking at its second weekly advance in a row. From a technical perspective, Fibonacci resistance lies at $55.890, 23.6% retracement of the mammoth October-November drop. The spread between WTI and Brent has narrowed to about $8.5 from above $10 in October.

WTI Weekly Chart

Source: OANDA fxTrade

NATURAL GAS is steadying around the middle of a three-week range following last month’s volatility. The weather factor is playing less of a role in direction this week, with below-average temperatures in the east countered by warmer-than-normal weather in the west.

Bloomberg has reported that US natural gas output has reached a record high since at least 2014, which could continue to pressure prices from their 4-1/2 year highs struck last week. The growing demand for the cleaner fuel is evidenced by an announcement from South Korean shipbuilder Hyundai Heavy that it has won an order for two new Liquefied Natural Gas carriers worth about US$370 million.

Agriculturals

SOYBEAN prices jumped to a 4-1/2 month high yesterday following news of the US-China trade war truce. Recall that soybeans had been worst hit of the agricultural commodities since the tariff tit-for-tat started. China’s imports of soybeans in October had fallen 95% from a year earlier, recent data had showed. Immediately following the handshake, the US announced that China had agreed to buy a “substantial amount” of agricultural, energy, industrial and other products from the US.

Yesterday’s surge stopped short of the 200-day moving average at 9.233, which has capped prices since June 7. Net non-commercial futures positioning is at its most bearish since the week of July 17, the latest data snapshot as of November 27 from CFTC shows.

Soybeans Daily Chart

Source: OANDA fxTrade

WHEAT prices have not reacted so enthusiastically to the G-20 announcements as they failed again to close above the 100-day moving average at 5.066. Prices did manage to halt a three-month slide last month, and this month looks set to build on that reversal. Notably, wheat has closed above the 55-month moving average for the past nine months. Russia’s exports of wheat are reported to be up 19% as at November 29 compared to last season.

SUGAR has started the week with a firmer bias after the G-20 meeting, but has so far failed to take out last week’s two-week high. Speculative positioning as at November 27 shows net non-commercial longs are at the lowest in six weeks, according to CFTC data, as the commodity fails to make headway to the upside. The European Commission announced that the Euro-zone 2018-19 sugar production is 11% lower than a year earlier.

CORN prices jumped to their highest in 3-1/2 weeks yesterday, pushing the recent rally to a second day. Speculative investors reduced their net long positions for a third straight week to November 27 and they are now at their least since the September 25 reporting week.

Precious metals

The broader risk-on mood since the G-20 meeting has seen the US dollar move lower. This has benefited GOLD, even though its appeal as a safe haven has waned. Gold prices touched a near-four week high this morning and are currently at 1,235.66. The gold/silver ratio slumped to its lowest in nearly two weeks yesterday as risk appetite surged. It has now recovered a tad to 85.567.

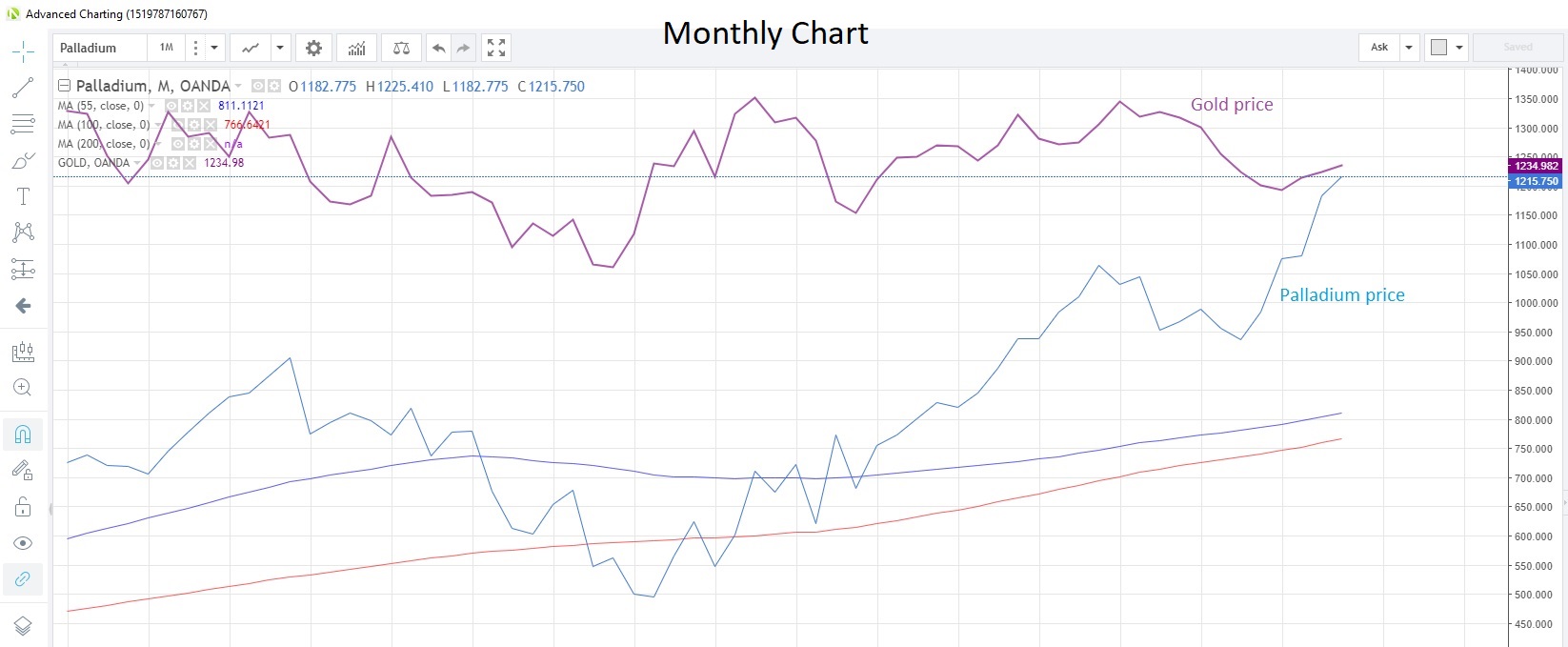

PALLADIUM continues to reach for the skies, touching its highest since Oanda began monitoring prices in 2005, and is now the closest ever to the gold price. News that China may rescind all tariffs on auto imports helped boost the commodity amid perceived additional demand for the metal in catalytic converters, going forward. Combined with a current shortage of the metal, prices embraced the path of least resistance.

Speculators believe the precious metal has more upside, as the latest data to November 27 shows investors adding to net long positions for the fourth straight week. Long positioning is now at is highest in nine months, at 14,476 futures contracts.

Gold/Palladium Daily Chart

Source: OANDA fxTrade

SILVER advanced to a 3-1/2 week high yesterday, though it failed to test the 100-day moving average at 14.653. Silver has traded below this moving average since June 15.

PLATINUM likewise is struggling to gain an advantage from the G-20 announcements. The metal managed its first up-day in five days yesterday, pulling prices from a 10-week low on Friday. Speculative accounts increased their net long positions for the first time in three weeks, latest CFTC data as at November 27 shows.

Base metals

COPPER surged to a two-month high post-G-20, but momentum quickly waned and the metal closed near to the opening price. Concerns about the details of the G-20 deal, and whether any concrete progress can be made in 90 days, has pulled the industrial metal off its highs. Speculative traders also trimmed their net long positions from 4-1/2 month highs in the week to November 27, according to CFTC, suggesting investors think booking some profits at these levels may be prudent.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Andrew Robinson

Latest posts by Andrew Robinson (see all)

- RBA cuts rates on virus impact - 2 March 2020

- Commodities Weekly: Oil rises first time in eight days - 2 March 2020

- Daily Markets Broadcast 2020-03-03 - 2 March 2020