- Cyclical sectors have underperformed, and Real Estate is the worst.

- No clear signs to indicate the resurgence of a major bearish trend.

- China A50 is at risk of further downside pressure to retest key support at 12,300.

China’s stock market has started to show signs of fatigue after a magnificent three-month rally of 22% from the October 2022 low to January 2023 high as seen on its benchmark CSI 300 Index. Since 18 April 2023, it has declined by close to -4% and underperformed a basket of developed nations’ stock markets.

The recent bullish up move from the October 2022 low of 3,495 in the CSI 300 has been fueled by optimism from the removal of prior Covid-zero lockdown measures, the introduction of stimulus measures to boost domestic consumption and reduce the credit crunch faced by embattled property developers as well as the toned down of draconian regulatory measures imposed on Chinese technology platform firms.

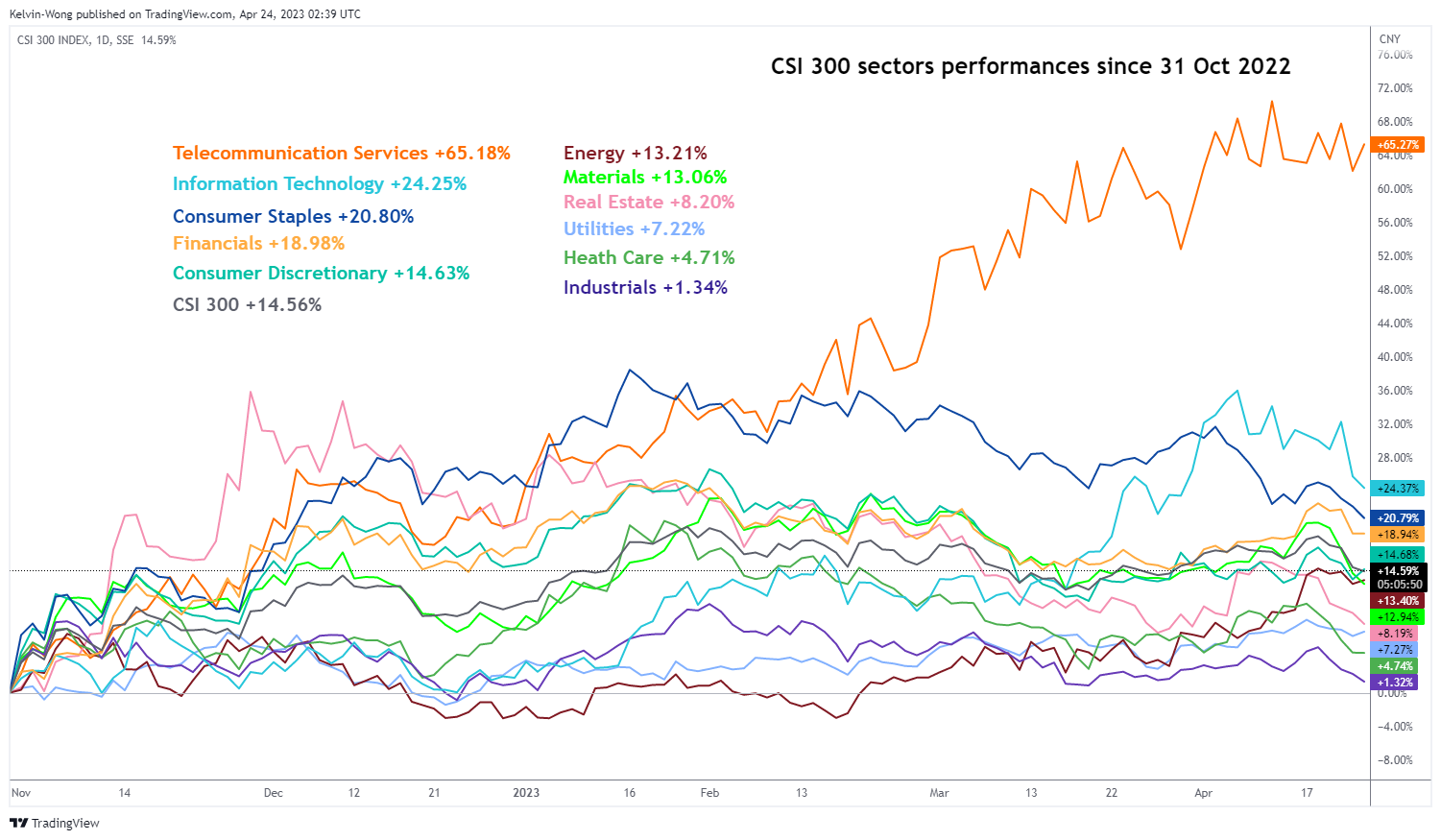

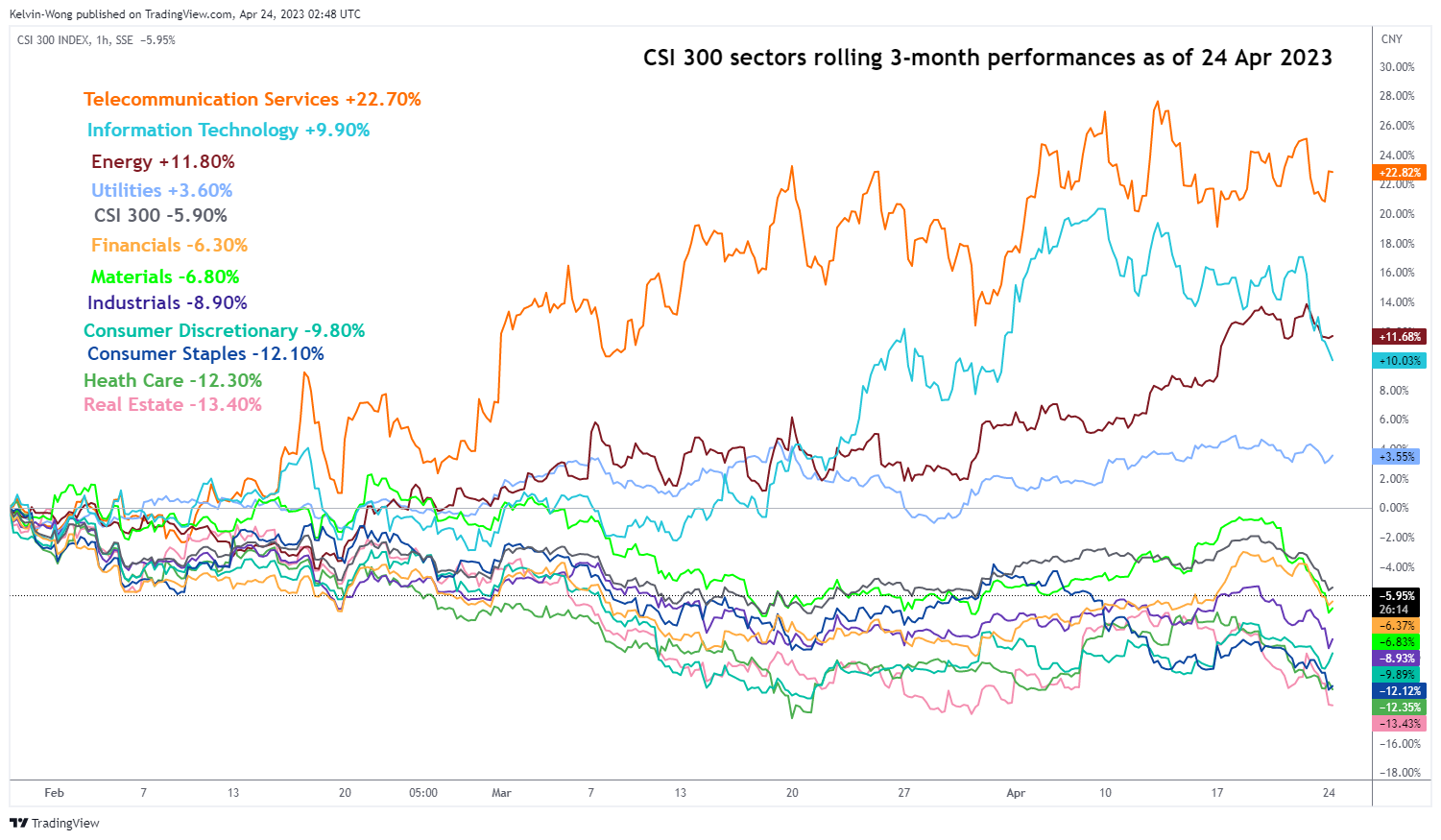

Cyclical sectors are the worst performers with Real Estate at the bottom

Source: TradingView as of 24 Apr 2023 (click to enlarge charts)

As seen from the charts above, cyclical sectors such as Materials, Financials, Industrials, Consumer Discretionary, and Real Estate have underperformed against the benchmark CSI 300; the worst is the Real Estate which recorded a three-month rolling performance of -13.40% versus -5.90% recorded in the CSI 300.

Meanwhile, two defensive sectors; Telecommunication Services and Utilities together with Energy and Information Technology have managed to outperform with positive gains of 22.70%, 3.60%, 11.80%, and 9.90% respectively over the same period.

It’s all about liquidity and investors’ positioning

The latest slew of robust economic data; China’s Q1 GDP, industrial output, and consumer spending for March coupled with a rebound in new home prices over the same period that recorded its fastest pace of recovery in 21 months on a month-on-month basis; a 0.5% increase in March from a 0.3% rise in February has allowed China’s policymakers some breathing space to a adopt a “wait and see” approach.

Hence, China’s central bank, PBoC is likely in a no hurry mode to further loosen its liquidity taps to stimulate economic growth at this juncture. The latest monetary policy action of PBoC has shown evidence of such a “controlled accommodating” stance where it has left the key one-year medium-term lending facility interest rate (MLF), that is PBoC’s lending rate to big commercial banks unchanged at 2.75% for the fifth consecutive month.

In addition, it injected the least amount of medium-term cash into the banking system; a 20-billion-yuan net injection via the MLF facility in April, the smallest amount since November 2022. Also, it left its other benchmark interest rates; the one and five-year loan prime rates unchanged at 3.65% and 4.3% respectively for eight consecutive months.

To put a halt to the credit crunch problem that resurfaced in 2021 for property developers and prevent contagion and systemic risk outbursts in the domestic financial system, Chinese policymakers have allowed indebted property developers easier access to the onshore corporate bond market for fundraising with a slew of regulatory easing measures introduced in 2022. One of them was the full guarantees for property developers’ issued bonds backed by the state-owned China Bond Insurance Company.

However, this key guaranteed initiative has started to lose its fanfare, property developers have managed to raise only 5.9 billion yuan of guaranteed onshore corporate bonds; down by -29% from 8.3 billion yuan recorded in December 2022.

Interestingly, some of China’s top-performing hedge funds such as Shanghai Bulls Asset Management and Shanghai Silver Leaf Investment have exited from their lucrative bets on high-yield property bonds that reaped more than 100% returns in 2022 as per reported by Bloomberg News.

Hence, a lack of further liquidity-pumping measures from PBoC and dwindling optimism in the Chinese property developers have reinforced the recent round of profit-taking activities seen in the various China benchmark stock indices such as the CSI 300 and FTSE China A50.

Is it the start of another major bear market for China equities?

Right now, it is still too early to put an “all-out” warning that we are witnessing the start of another major bearish trend phase to breach below the October 2022 low of the mainland benchmark stock indices as recent economic data as per mentioned earlier are indicating a recovery stage and inter-market analysis via a potential further weakening of the US dollar in the medium-term tends to support the China stock market.

The next key economic data to watch to have a clearer picture of the crystal ball is the release of the official NBS Manufacturing and Non-Manufacturing PMIs for April on Sunday, 30 April 2023. Forecasts are expecting a continuation of manufacturing growth to 52 from 51.9 printed in March; likewise, for the non-manufacturing activities where it is expected to increase to 58.3 in April from 58.2 in March, and if it turns out as expected, it will be the fourth consecutive month of expansion.

Also, consumer spending data during the upcoming Golden Week holiday for the Labour Day celebrations that kickstarts on 29 April to 3 May to have the latest gauge on consumers’ optimism and spending power.

The main inherent risk is geopolitical where the relationship between US and China is still frosty. The US-China High Tech war is still “alive” since 2018, the Biden administration is set to unveil new investment curbs on China in the next upcoming G-7 meeting in May for endorsement. These new measures cover the fields of semiconductors, artificial intelligence, and quantum computing that limit investments from US firms, including venture capital and joint ventures.

China A50 Technical Analysis – at the risk of short-term bearish pressure to retest a key support

Source: TradingView as of 24 Apr 2023 (click to enlarge chart)

Since its 27 January 2023 swing high of 14,437, the China A50 Index (a proxy for the FTSE China A50 futures) has declined by -11% and evolved into a short-term bearish trend with an intermediate resistance at 13,470.

Downside momentum remains intact as indicated by the daily RSI oscillator where it has just staged a bearish breakdown below a former corresponding ascending support at the 44% level and has the potential to inch lower before it reaches the oversold region of less than 30%.

If the 13,479 intermediate resistance is not surpassed to the upside, the Index may see the continuation of the short-term downtrend with support coming in at around 12,300, a medium-term pivotal level that also coincides with the former major descending resistance from the 27 May 2021 high.

A point to note is that the Index is still evolving in a potential long-term bullish impending “Inverse Head & Shoulders” configuration since the 15 March 2022 low.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Kelvin Wong

Passionate about connecting the dots in the financial markets and sharing perspectives around trading and investment, Kelvin Wong is an expert in using a unique combination of fundamental and technical analyses, specializing in Elliott Wave and fund flow positioning, to pinpoint key reversal levels in the financial markets.

In addition, over the last ten years, Kelvin has conducted numerous market outlook and trading-related seminars, as well as technical analysis training courses, for thousands of retail traders.

Latest posts by Kelvin Wong (see all)

- Gold Technical: The recent sell-off may have reached a potential bullish reversal level at US$2,353 - 26 July 2024

- SPX 500: Further weakness may trigger a medium-term global risk-off event - 25 July 2024

- Nasdaq 100: Potential bullish reversal looms ahead of Alphabet and Tesla earnings results - 23 July 2024