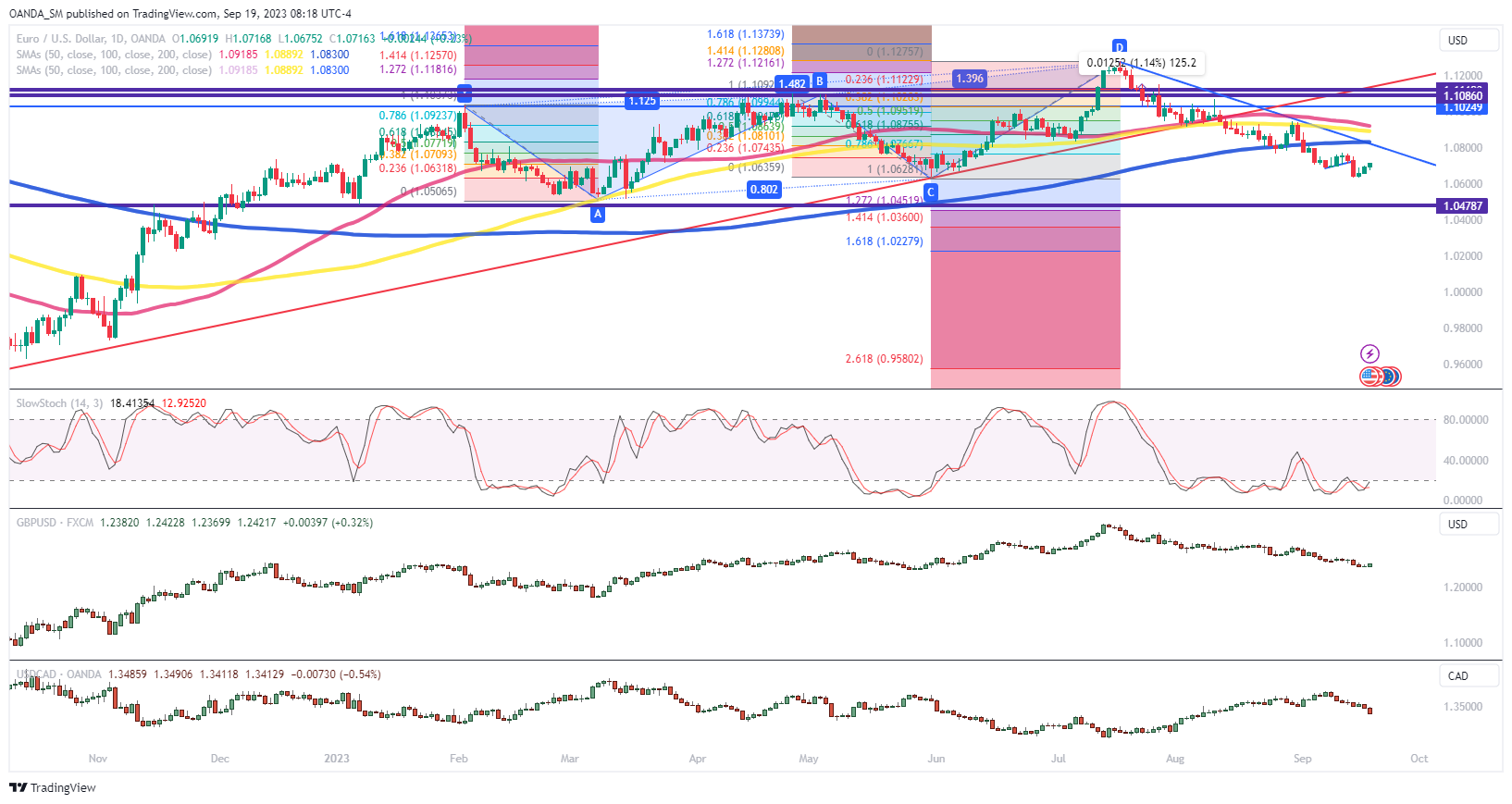

Modest dollar weakness is emerging as the Fed begins their two-day policy meeting; the euro is back above the 1.07 level, while the loonie is advancing below the 200-day SMA, and as the British pound rises above the 1.24 level. Positioning into the FOMC meeting is seeing rate options traders increase hedges, which means some traders are worried that the expected mid-year pivot could be in jeopardy.

FOMC

Inflation has come down a lot, but the Fed’s inflation isn’t quite over yet. The market is assuming that inflation will come down all the way down to the Fed’s 2% target and that rate cuts will happen before next summer starts. The risks for headline inflation to heat up over the next couple of months are rising and that should complicate what the Fed does. Do policymakers become convinced that despite a resilient labor market, pricing pressures will continue to ease? If core inflation shows it is struggling to continue to drop, the higher-for-longer rate regime will last a lot longer than the market is pricing in.

To have a weaker dollar, the Fed’s projections will need to show policymakers don’t believe inflation will be too complicated to bring prices back down close to target. For stock market bulls, it seems if optimism remains that the Fed is likely done raising rates, that could help keep equities supported a little while longer. If the peak is in place Wall Street will anticipate that peak tightness in financial conditions is here and that it will only get better going forward. The problem for stocks is that double digit earnings growth will not be easy given revenue growth will be soft given the long and variable lags from the Fed’s tightening.

Where the market is getting the stock market wrong is the current belief that a soft landing means we can just count on the AI trade, improved productivity, and economic resilience for earnings to hold up. The problem is that the risk of a soft landing becoming hard landing is there. Stocks will struggle as the fastest rate hiking cycle into a leveraged system with quantitative tightening means we might not have enough excess liquidity to keep driving real money growth and economic growth.

USD outlook

Near-term action for the dollar will depend on the Fed and if the market believes the risks are growing for higher-for-longer to last deep into next year. The dollar could be supported over the short-term if the Fed seems likely to deliver one more rate hike at the end of the year.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Ed Moya

His particular expertise lies across a wide range of asset classes including FX, commodities, fixed income, stocks and cryptocurrencies.

Over the course of his career, Ed has worked with some of the leading forex brokerages, research teams and news departments on Wall Street including Global Forex Trading, FX Solutions and Trading Advantage. Prior to OANDA he worked with TradeTheNews.com, where he provided market analysis on economic data and corporate news.

Based in New York, Ed is a regular guest on several major financial television networks including CNBC, Bloomberg TV, Yahoo! Finance Live, Fox Business, cheddar news, and CoinDesk TV. His views are trusted by the world’s most respected global newswires including Reuters, Bloomberg and the Associated Press, and he is regularly quoted in leading publications such as MSN, MarketWatch, Forbes, Seeking Alpha, The New York Times and The Wall Street Journal.

Ed holds a BA in Economics from Rutgers University.

Latest posts by Ed Moya (see all)

- Market Insights Podcast – Powell struggles to deliver a hawkish hold - 1 November 2023

- Fed React: USD/JPY softer after Fed fails to deliver hawkish hold - 1 November 2023

- EUR/USD: Dollar wavers on slower pace of Treasury Refunding Sales and mixed labor data - 1 November 2023