- 10-year JGB implied volatility has tapered downwards since the implementation of flexible YCC in October 2023, lowering the odds of disorderly movements in the JGB

- Elevated demand-pull inflation (excluding fresh food & energy) in Japan may prompt BoJ to upgrade its inflation (excluding fresh food & energy) forecasts for FY 2024 & FY 2025.

- Technical analysis has detected bearish elements in USD/JPY where JPY may start to strengthen in the short term towards 146.25 and a break below it exposes 144.55 next.

Bank of Japan (BoJ) will conclude its first monetary policy meeting for 2024 tomorrow, 23 January. In the past three months, calls from the Japanese private and public sectors and even ex-BoJ officials have urged the Japanese central bank to ditch its current -0.1% short-term interest rate in place since 2016 as such a level is irrelevant and does not reflect the current fundamentals of the Japanese economy.

Since BoJ’s prior monetary policy meeting outcome on 31 October, the central bank has taken “baby steps” to guide market participants on the ending of its short-term negative interest rate policy and kickstart normalization of its current ultra-easy monetary policy stance.

BoJ has allowed more flexibility of its Yield Curve Control Programme on the 10-year Japanese Government Bond (JGB) yields as it scrapped the prior hard-capped upper limit of 1% to make it as a reference level now where BoJ’s will “nimbly conduct its market operations” around that 1% level.

Current flexible YCC model has lowered 10-year JGB implied volatility

Fig 1: 10-year JGB implied volatility with JGB futures & USD/JPY as of 19 Jan 2024 (Source: TradingView, click to enlarge chart)

This flexibility of allowing the 10-year JGB yield more breathing space to fluctuate on the upside has enabled BoJ not to be “boxed in” when it eventually removes the YCC programme as a non-committal stance to any perceived hard-capped upper limit is likely to reduce undesirable speculative activities in the JGB futures market that is likely to trigger adverse reflexive loops into other asset classes and the real economy.

The current YCC modus operandi to deter rampant speculation activities in the JGB futures market seems to be working as the implied volatility of the 10-year JGB has dropped from a high of 7.98 before the 31 October 2023’s new YCC flexible implementation to 3.79 as of last Friday, 19 January (see Fig1).

Forward guidance will be key for tomorrow as demand-pull inflation remains elevated

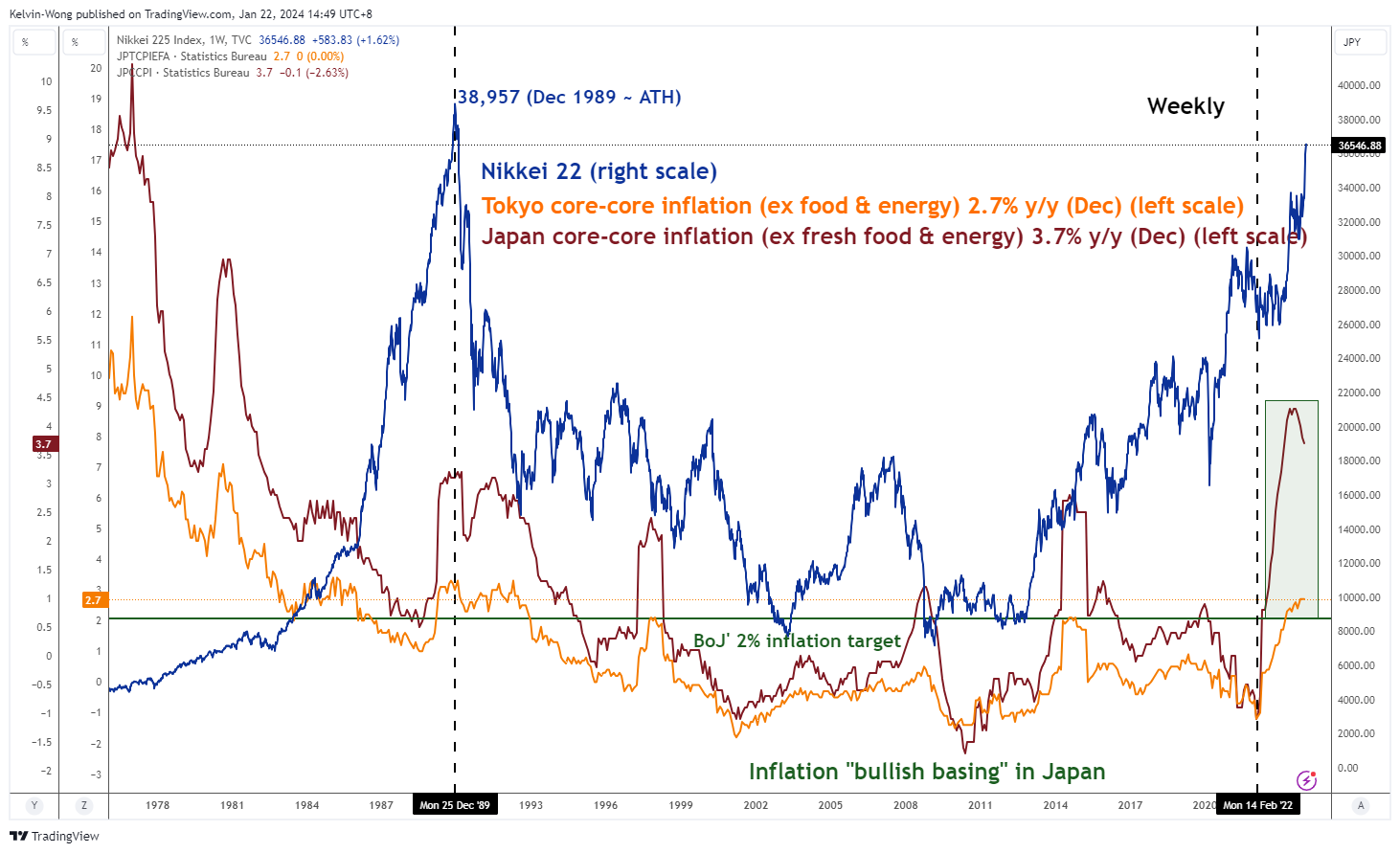

Fig 2: Tokyo & Japan core-core inflation trends with Nikkei 225 as of 22 Jan 2024 (Source: TradingView, click to enlarge chart)

In the run-up to tomorrow’s BoJ monetary policy decision outcome, market participants have toned down significantly the expectations of the removal of short-term negative interest rates due to the recent Japan’s Noto earthquake that occurred at the start of the new year. Right now, expectations on BoJ’s stance to scrap short-term negative interest rates have shifted down the calendar to the next meeting in April where BoJ will also have the release of preliminary results of annual wage negotiations between unions and companies that are still ongoing till the end of March. Stable and rising wages are key criteria for Japan to enable a forceful and sustainable exit from its decade-plus of deflationary spiral according to BoJ Governor Ueda.

Even though inflation growth has eased off in December due to cost-push factors such as lower oil prices as indicated by the Tokyo and nationwide Japan CPI data, demand-pull related inflation excluding fresh food and energy in Japan has remained elevated at 3.7% y/y, a 42-year high, and above BoJ’s 2% target for the 15th consecutive month. Services inflation in Japan also grew by 2.3% y/y for the second consecutive month in December, its fastest pace in three decades.

Therefore, market participants will be scrutinizing the BoJ’s monetary policy statement, its latest inflation projections in its updated quarterly outlook report as well as BoJ Ueda’s press conference for hints of “comfortability” to finally set the stage for the removal of short-term negative interest rates.

In the previous quarterly outlook released in October, BoJ upgraded its inflation forecasts (excluding fresh food & energy) to 1.9% y/y for fiscal years 2024 and 2025 from 1.7% y/y and 1.8% y/y respectively. A further potential upgrade on inflation (excluding fresh food & energy) towards 2% y/y for 2024 and 2025 suggests a potential signal to the market that the end of short-term negative interest rate is imminent and baby steps are in the pipeline for the normalization of ultra-easy monetary policy.

Watch the 149.30 key short-term resistance on USD/JPY

Fig 3: USD/JPY short-term minor trend as of 22 Jan 2024 (Source: TradingView, click to enlarge chart)

The recent 5-day rally of USD/JPY from 12 January to 19 January 2024 intraday high of 148.81 has started to show signs of exhaustion ahead of tomorrow’s risk event (BoJ’s monetary policy decision outcome).

The hourly RSI momentum indicator has flashed out a bearish divergence signal at its overbought region while its daily price actions as of the close of last Friday, 19 January have formed a bearish daily “Spinning Top” candlestick pattern after prior three consecutive appearances of bullish candlesticks right below a key short-term pivotal resistance at 149.30.

The intermediate support zone will be at 147.30/146.25 and a break below 146.25 may trigger a potential impulsive down move sequence to expose the next support at 144.55 (also 50-day and 200-day moving averages) in the first step.

On the other hand, a clearance above 149.30 invalidates the bearish tone to see the next intermediate resistance coming in at 150.20/70.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Kelvin Wong

Passionate about connecting the dots in the financial markets and sharing perspectives around trading and investment, Kelvin Wong is an expert in using a unique combination of fundamental and technical analyses, specializing in Elliott Wave and fund flow positioning, to pinpoint key reversal levels in the financial markets.

In addition, over the last ten years, Kelvin has conducted numerous market outlook and trading-related seminars, as well as technical analysis training courses, for thousands of retail traders.

Latest posts by Kelvin Wong (see all)

- Gold Technical: The recent sell-off may have reached a potential bullish reversal level at US$2,353 - 26 July 2024

- SPX 500: Further weakness may trigger a medium-term global risk-off event - 25 July 2024

- Nasdaq 100: Potential bullish reversal looms ahead of Alphabet and Tesla earnings results - 23 July 2024