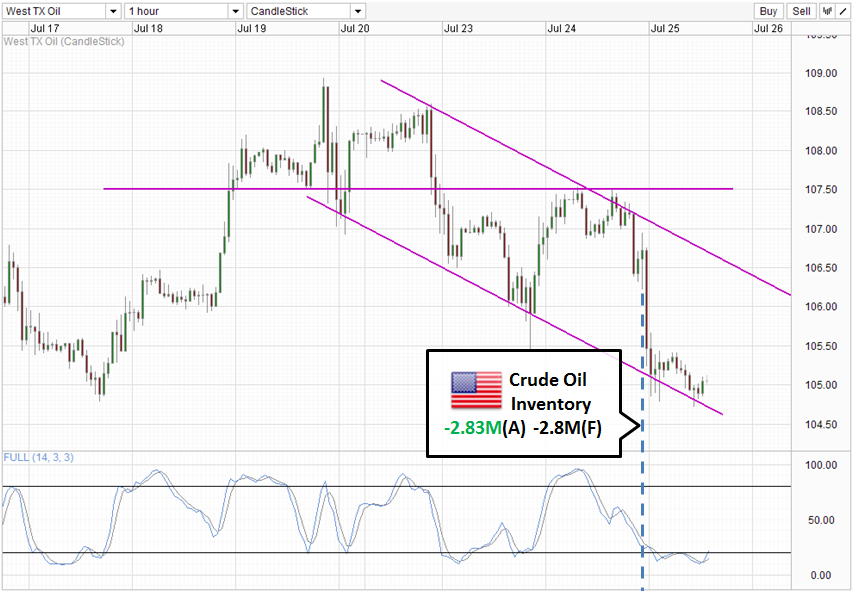

Latest Inventory Data from US Department of Energy showed yet another week of higher implied demand. Inventory stock fell by 2.83 million barrels, higher than the expected 2.5-2.8 million quoted by analysts. This brought the sequence of higher implied to 4 weeks, an incredible run by any standard. However, this result did not push crude oil prices higher, with WTI prices actually falling heavily yesterday, hitting below 105.0 during US trading session. In some cases, this lack of bullish follow through can be explained away by looking at the implied demand of refined products. However, in this case it seems that all the refined demand remains robust – Distillate Inventory fell by 1.2 million barrels vs a +1.85 million increase. Gasoline fell by 1.4 million vs expectations of +1.65 million. Having low refined inventories suggest that the demand for crude will continue in order to back-fill the shortfall, which should support WTI prices.

Perhaps, a better explanation would be that bulls have had it good for too long, and hence is looking for an even bigger upset. After being treated to 3 consecutive weeks of huge shortfall of inventory vs expectations (an average of 6.5 million barrels each week), bulls are no longer impressed with the paltry 0.03 – 0.3 million barrels this week. Furthermore, looking at the previous 3 weeks, the gap between shortfall and expectations appear to be tightening, suggesting that the rate of increase in implied demand is actually declining. Traders being a forward looking bunch, understandably would be less than thrilled at this week’s numbers.

Furthermore, the fundamentals for Oil is still looking week. Global industrial activities remain lower on a Y/Y basis. The only reason demand actually increase this time round is actually due to seasonality impact, where most of the world factories are running round the clock due to favorable weather conditions in summer. Industrial activities are also higher in order to meet the year end holiday demand where consumer purchases are expected to pick up. Moving forward from here, manufacturing output can only decline from here out with Autumn coming, and this could spell the end of crude’s current purple patch. A suspected change in risk appetite is also not helping,

Hourly Chart

From a technical perspective, price has rebounded from the Channel Top and 107.50 resistance, finding support from Channel Support. Stochastic readings suggest that a bullish cycle may be in play soon, with stoch readings currently peaking above the 20.0 mark. This opens the possibility of price heading towards Channel Top, which is standing around 106 – 106.5 now. However, price should clear 105.5 interim resistance in order to signal its bullish conviction, as short-term pressure is downwards with price posting lower lows and lower highs since the start of the week. Downside wise, should price break the 17th July low of 104.8, 104.0 will open up as immediate bearish target, which may signal further bearish acceleration if broken as the longer-term bull trend will be severely compromised.

More Links:

NZD/USD – RBNZ Record-Low Interest to End in 2014

EUR/USD – Settles Back in Familiar Territory around 1.32

AUD/USD – Falls Sharply Away from the Resistance Level at 0.93

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

centers on forex and macro-economic trends impacting the Asia Pacific region.

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014