Surprise surprise surprise. RBNZ kept policy rate as expected, but the accompanying statement by Governor Wheeler was anything but. First off the bat, he said that removal of monetary stimulus (e.g. current low interest rate) will “likely be needed in the future”, but tried to downplay the immediacy of any rate hike, saying that RBNZ will keep the Official Cash Rate unchanged for the rest of 2013. The corallary implies that we WILL see rate hike in 2014, resulting in speculators increasing bets that the OCR will be raised as early as Jan 2014.

It seems that the rising Housing bubble has Wheeler’s neck in a noose. According to Wheeler, NZD “remains high”, and it is clear that he would have pushed the OCR lower if he could help it. Unfortunately, the growth in housing market remains sticky, and hence using a lower OCR To push NZD lower is certainly not an option here. To put into perspective the tough fight RBNZ is having with regards to the housing gains, we can simply look at the latest round of policy changes that is currently being proposed – Banks may be limited to lend only 20% of a property’s value in the near future. In comparison, Singapore’s ratio is 60% after the latest round of tightening, while US and China were basically giving out easy 100% loans prior to their respective credit crisis. Hence the only proper response RBNZ can have against the strengthening NZD would be to intervene directly by selling the currency, whose effectiveness is highly suspect.

One begin to wonder if the threat of rate hike is simply aiming at the rampaging housing market only. But looking at NZ fundamentals, it seems that there is good reason for rate to increase in the long run. According to RBNZ’s data, NZ economy is picking up across various sectors. Consumption has also increased, while reconstruction efforts for disaster recovery will continue to help boost the economy. What this means is that the rate cut is not solely to counter gains in housing prices, but perhaps a good reflection of the economy’s strength, and imply that any rate hikes next year may be permanent, with rate curve pointing higher.

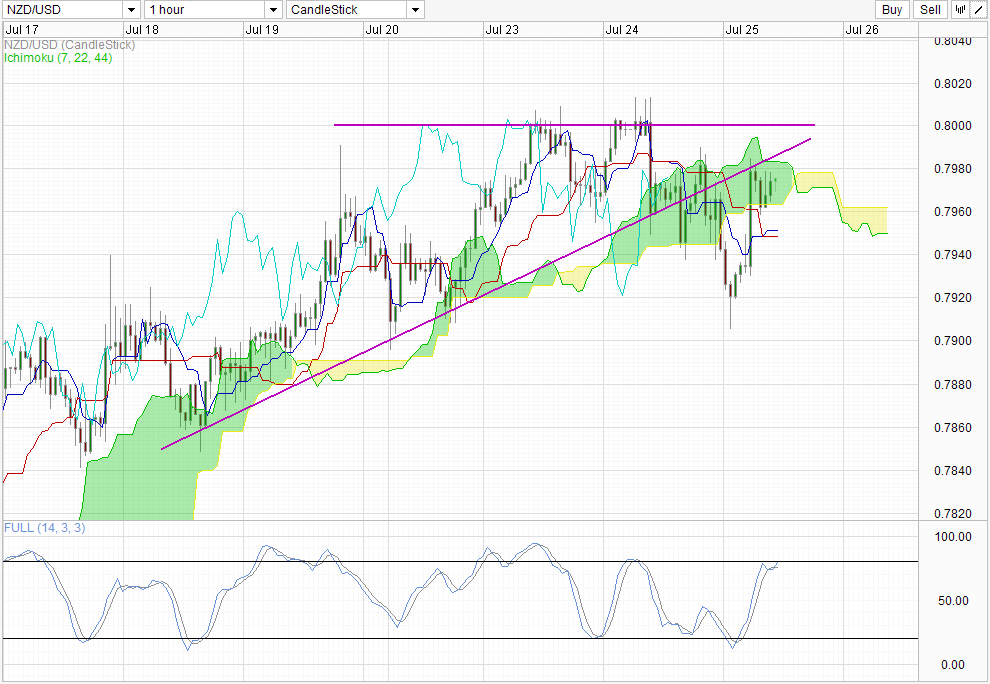

Hourly Chart

From a technical perspective, NZD/USD is not entirely bullish as of now. The rally post RBNZ decision only managed to push into the overhead Kumo, with the rising trendline continue to reject any attempt to break higher. The pullback from the rally is kept afloat by Senkou Span B, keeping price above 0.796. However, given the continued bearish Kumo twist ahead, and the failure of current rally to test Senkou Span A coupled with Stoch readings reaching Overbought, the signs are not good for a move back towards 0.80. Furthermore, risk appetite in Asia is bearish, continuing the sell-off seen during US market session yesterday. This will add more weight in favor of bears, and we could potentially see a push lower in the short-run.

Fundamentally, RBNZ has announced previously that they will sell NZD when a bear trend is clear. If price does break 0.796 and preferably break 0.792, the short-term bullish pressure will be alleviated, and could afford RBNZ the window of opportunity to push prices lower. However, all these are simply short-term pressures. As price is still trading comfortably within the multi-year support Channel , we could still see long-term bulls winning the day eventually given a steeper forward yield curve and improving NZ fundamentals.

More Links:

GBP/USD – Resistance at 1.54 Stands Tall

AUD/USD – Falls Sharply Away from the Resistance Level at 0.93

EUR/USD – Settles Back in Familiar Territory around 1.32

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014