Tuesday February 26: Five things the markets are talking about

Global equities are trading under pressure in the overnight session, while sovereign bond prices have found a bid as investors pare back a portion of their initial euphoria surrounding the Sino-U.S trade talks. The pound (£1.3208) has found its ‘sea legs’ after U.K PM Theresa May is said to be considering a plan to delay Brexit.

Brexit agenda

PM May is expected to allow her cabinet to discuss extending the deadline beyond March 29 at a meeting this morning and then reveal the cabinet’s conclusions in an announcement to Parliament later (07:30 am ET).

On the central bank front, Fed Chair Powell will deliver his semi-annual testimony on monetary policy and the state of the U.S economy over the next two-days (Feb 26/27) to House and Senate committees. In addition, several of his colleagues will also be speaking this week.

Elsewhere, crude oil prices have extended their losses after tumbling the most in over a month so far this week on criticism from President Trump that prices are too high.

On tap: U.S consumer confidence at 10 am EDT and New Zealand trade balance (04:45 pm ET). President Trump and North Korea leader Kim Jong Un are expected to meet later today for a second summit.

1. Stocks see red

In Japan, the Nikkei share average closed a tad weaker overnight, under selling pressure ahead of Japan’s fiscal year-end in March. The Nikkei ended the session down -0.37%, while the broader Topix shed -0.23%.

Down-under, Aussie shares have snapped a three-session winning streak overnight, with financials and resources stocks leading broad-based losses. The S&P/ASX 200 index fell -0.9% at the close of trade, its worst session in nearly eight-weeks. The benchmark rallied +0.3% yesterday. In S. Korea, the Kospi index traded essentially flat at -0.15%.

In China, stocks fell overnight in heavy volume as a percentage of investors took profits on heavyweight financial shares, believing that Monday’s “spectacular surge” is unsustainable. The CSI300 settled down -1.2% lower, while the Shanghai Composite Index fell -0.7%. The CSI300’s rise in yesterday’s session was its biggest one-day gain in three-years.

In Hong Kong it was a similar story. Stocks fell, tracking other regional bourses, as investors waited to see if the U.S and China can clinch a trade deal. At the close, the Hang Seng index fell -0.7%, while the China Enterprises Index lost -0.8%.

In Europe, regional indexes are following suit and trade lower along with Asia. However, the U.K’s FTSE 100 index is underperforming its regional counterparts, falling -1% as the sterling rallies against both the dollar and the EUR.

U.S stocks are set to open in the ‘red’ (-0.23%).

Indices: Stoxx600 % at #, FTSE -1.00% at 7,112.25, DAX -0.24% at 11,478.33, CAC-40 -0.27% at 5,217.61, IBEX-35 -0.32% at 9,174.72, FTSE MIB -0.05% at 20,426.50, SMI 0.00% at 9,402.70, S&P 500 Futures -0.23%

2. Oil eases after Trump urges OPEC to curb prices, gold unchanged

Oil prices are again a tad lower, extending yesterday’s losses of more than -3% after President Trump called on OPEC+ to rein in its efforts to boost prices.

Brent futures are at +$64.70 a barrel, down -6c, or -0.1% from Monday’s close, while U.S West Texas Intermediate (WTI) crude futures are at +$55.26 per barrel, down -22c, or -0.4%.

Note: Brent plunged -3.5% in yesterday’s session.

Tweeting yesterday, President Trump expressed his concern about higher oil prices (supported by production cuts) and repeated his previous calls on OPEC+ to keep prices steady.

Aiding Trumps tactics is the fact that oil markets were trading higher on Sino-U.S trade optimism. With some investors cashing in on the recent equity rally overnight have naturally put commodity prices on the back foot.

However, sanctions by the U.S against oil exporters Iran and Venezuela have contributed to the recent gains and should also provide a floor for prices.

Ahead of the U.S open, the ‘yellow’ metal is little changed despite President Trump stating that he would delay an increase in tariffs on Chinese goods. Spot gold is flat at +$1,327.40 per ounce, while U.S gold futures are steady at +$1,329.9 per ounce.

Elsewhere, Palladium hit a record high this morning, surging above +$1,550 as a threatened strike by South African mineworkers added to supply concerns in an already tight market.

3. French yields at two-year low as “yellow vest” effect wanes

In this morning’s Euro session, France’s 10-year government bond yield has dropped to its lowest level in over two-years as the effect of the country’s “yellow vest” protests fade. Also aiding French bond prices is the fact that French President Macron’s popularity has recovered to levels not seen since the protests broke out three-months ago.

Elsewhere, broader eurozone yields are under pressure from next week’s European Central Banks (ECB) monetary policy expectations.

French 10-yea yields have dropped to +0.506%, down nearly -2 bps in the session, while the German 10-year Bund yield are hovering atop of the +0.10% mark, slightly lower on the day.

Fixed income traders will take their cue from the Fed this morning (09:45 am ET). Fed chair Jerome Powell will testify to the U.S Senate on the semi-annual monetary policy report before the Senate Banking Committee. Markets will be looking for signs on potential interest rate hikes this year and that U.S policymakers will stop running down the central bank’s balance sheet.

The yield on 10-year Treasuries has declined -1 bps to +2.65%, while in the U.K, the 10-year Gilt yield has advanced less than +1 bps to +1.18%.

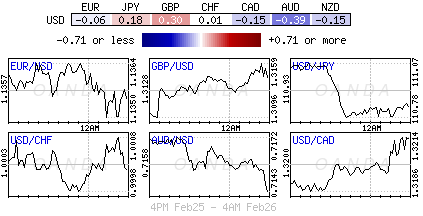

4. Sterling finds support on Brexit delay talk

The pound is rallying after reports that U.K PM Theresa May is considering a plan to delay the country’s scheduled departure from the EU next month. Sterling (£1.3203) was recently +0.7% stronger against the U.S dollar.

With a little more than a month to go before the UK’s scheduled exit from the E.U, lawmakers have yet to settle on a deal with the bloc. Yesterday, the Labour Party said it would be prepared to back a second Brexit referendum, adding to uncertainty about the path the UK will take in the coming weeks.

Elsewhere, the ‘big’ dollar continues to hover atop of its one-month lows (C$1.3207, €1.1362, ¥110.86) and seems well contained within recent quarterly ranges for G10 currency pairs.

Dealers have shifted their focus to Fed Chair Powell’s semi-annual testimony to Congress – will we hear more ‘dovish’ comments from the central banker?

5. Hong Kong exports down for a third consecutive month

Data earlier this morning showed that Hong Kong’s export-oriented economy suffered further from Sino-U.S trade tensions as outbound shipments fell year-over-year for a third consecutive month in January.

The headline print showed a -0.4% decline which was still better that the December -0.5% drop.

The city’s government says the external environment is “still challenging,” noting moderating economic growth in many key trading partners will likely weigh on Hong Kong’s merchandise exports near-term.

Note, imports dropped -6% from January 2018.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019