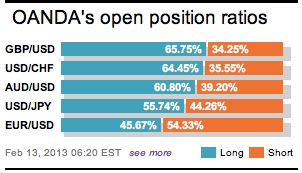

An “unnamed official” is not getting their due credit for some of the recent market movements in forex-land. These individual have added to the quality of volatility for dealers and investors alike in this ‘economic summit season.’ Characteristically, they are consistent and have appeared after most high profile policy points have been delivered in recent times. Thankfully, they are the individual’s that are translating some of these policy’s meanings and insisting on what market movements should be.

Last week the single currency fell awkwardly after ECB’s Draghi’s communiqué was delivered. In some corners it was viewed as a feeble attempt by the Central Banker to talk his currency down from elevated heights. The “unnamed source” was there to interpret his comments more accurately for the layperson. In translation, they highlighted that the value of the currency should be considered when assessing monetary conditions.

On Monday this week, the market took its cue from ECB’s Weidmann comments; who suggested that the 17-member currency was “not seriously overvalued.” The yen was allowed into the mix after one individual at the US Treasury heavily hinted that US supports Japan’s deflation efforts. Even a prime ‘dove’ candidate for the Bank of Japan’s top job was allowed to influence the yen value after suggesting that their currency value was “naturally adjusting” from extremely high rates of exchange to a more desirable or appropriate level.

Yesterday was perhaps the “unnamed source’s” biggest cameo thus far. The G7 issued a statement to dampen the recent discussion of “currency wars” so heavily covered by all news sources. More importantly, the G7 was able to show solidarity ahead of the G20 later this week, as their ‘commanding’ influence is under threat from the emerging markets. That ‘source’ again appeared, muddying one of the G7’s primary objectives by suggesting that the G7 is indeed concerned about the yen’s value. This happened to unravel some of weakening premium that the yen had acquired.

Central Bankers are always concerned about excessive currency weakness; however, they are more concerned by the speed of currency movement. More so now than ever, because of the season that is in it, the forex markets will remain susceptible to comments from credited and “unnamed” sources. Is this currency manipulation? It’s certainly a grey area, but market volatility has heightened mostly by increased trading from the “less” fearful investor. The apparent lack of cohesion amongst officials is now putting further pressures on other officials to clarify their position at the upcoming G20 meeting. No matter what, this market can expect a rather apprehensive long weekend.

A couple of other European Central Banks, non EUR dependent, happened to take off some this market heat in early European trading this morning. The SEK managed to climb to its strongest position against the EUR in four-months after the Riksbank left interest rates at +1%, disappointing a segment of the market who were looking for a -0.25% ease. Bullish rates have led to a bullish Krona. The Central Bank made no changes to future rate expectations. Expect the futures market again price in a cut for April.

The “Old Lady’s” inflation report this morning confirms Governor King’s view of high inflation and lower growth projections. The Bank of England views that the above target inflation projections “are consistent with its mandate.” Inflation has been explained away as being due to temporary factors. Despite inflation being above target, the BoE has managed to coordinate further QE along the way. This confirms that policy maker’s focus is on growth not inflation as being the key to exit a triple-dip recession. This nicely leaves the door ajar to Governor Carney for more QE to support UK growth.

Recent market focus has become rather myopic to yen price movements. The “he said she said” has yen weakening and strengthening at will. Lack of cohesiveness and clarity does this easily to any market; however, Japan is in a strong position to argue that it complies with yesterday’s G7 statement. Their policy initiatives to date have been domestically focused. Once realized, the current weak yen momentum should get back on track. The market should expect the recent yen buying to be limited if theory holds true.

Other Links:

Obama’s 2013 State of the Union Address: Summary and Reaction

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019