Capital markets are still waiting for common sense to prevail. It’s the most basic of ingredient that is required by Washington to resolve the federal budget impasse and to tackle the federal debt ceiling debate whose deadline for many is becoming too close for comfort (October 17th). Some members of Washington are playing ‘high stakes poker’ apparently blind. This is somewhat similar to many investors who have been left with less economic news and guidance due to the partial shutdown of the federal government. The market continues to hold a view that the US situation will find a resolution.

The market will be expecting this mid-week release to provide some extra clarity on when the Fed’s monthly $85b bond buying program may begin to taper. Next up will be the US retail sales release this coming Friday – it remains a key reading on the domestic consumer sector. However, do not be surprised to find that various Federal government indicators release dates may continue to change due to a fiscal budget impact on both the Commerce and US Labor Department work schedules. Any indicators produced by the Fed’s and any private companies remain not affected. Investors should remain alert that indicators not released this past week might be released this week on an “unscheduled” basis if Washington politicking and federal budget issues are resolved.

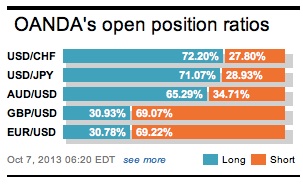

The 17-member single currency currently remains entrenched in a three-cent scope, 1.34-1.37 consolidation range, with some dealers believing its upside could run out of steam and while a re-test of the 1.3645 and 1.3710 peaks cannot be ruled out in the near term. Against sterling, the GBP has rebounded from last week’s late sell-off (1.6059), with dealers noting that the gains have mostly been driven by the plethora of positive economic UK data surprises. The BoE meet this week – governor Carney’s “lower rates for longer” will surely be challenged, again. The current yen direction is mostly been swayed by the direction of its domestic equity indexes. In the overnight session USD/JPY was able to print a fresh one-month low below 96.90 after the Nikkei225 again slumped by -1.2% to close below +14k. So far, the mighty dollars decline remains gradual as traders remain reluctant to bet heavily against it while not knowing when lawmakers may make a compromise. Any heighten concerns of US debt default will only push US Treasury yields higher and have global bourses trading further into the ‘red.’ Investors will try and remain tight with their “wait and see” approach.

Is the EUR’s near term strength on borrowed time?

Dean Popplewell, Director of Currency Analysis and Research @ OANDA MarketPulseFX

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019