Market enthusiasm seems weary at best, despite the various asset classes taking their cue from an upbeat overnight Asian session. Even the new Chinese leader, Xi Jinping, made some encouraging statements about his country’s own economy, raising expectations that the newly elected leadership will ensure the appropriate support for current economic policies will remain in place over the coming quarters has had a limited response. Investors remain cautious ahead of data releases both side of the Atlantic today and ahead of upcoming Central Bank announcements.

The UK service sector continues to slow with this morning’s PMI reading for last month showing 50.2 compared to expectations for a 51.1 release. When looking at the previous months reading of 50.6, the weakness was modest, but still taking the UK economy towards contraction. The worsening outlook is further highlighted by that economy’s new order index that slipped below 50 towards 49.6 in November. It’s difficult to see an immediate economic upturn when ‘new-order’ releases are under pressure. The market is beginning to expect further assistance from the BoE, although maybe true, it’s more likely that the current policy pause may continue until the new BoE governor takes residence in July. The UK Chancellor’s autumn statement, later this morning, is likely to draw significant market attention given the renewed risk of a UK downgrade.

Euro-zone private sector business activity shrank in November, but at a slower pace that the previous month (the PMI print rose to 46.6 from 46 in October). Although higher, the composite remains in contraction territory, indicating that the Euro-zone again has faltered in Q4. Apparently, Ireland was the only member to record a pick up in private sector activity. While the pace of contraction may be easing, there remain limiting signs that the regions economy is returning to growth. Tomorrow’s ECB meeting should be more forthcoming in picture painting, despite the already expected rhetoric and accompanying communiqué.

When most of us are window-shopping later this month, the Japanese politicians and the electorate will be kept busy and distracted to varying degrees. The official campaigning for Japan’s general election began in haste yesterday. Currently, the main opposition party is leading in voter support. Many analysts expect this crowded race to result in a coalition government, one that most likely to be plagued by “gridlock and policy stagnation.” This time around a record number of parties are expected to register more than 1,400 candidates to compete for the 480 seats in the lower house. The value of the Yen will especially become everyone’s concern over the coming weeks.

Has President Obama sketched out a potential year-end deal pairing tax increases and spending cuts to avert the so-called fiscal cliff, while insisting Republicans must accept higher tax rates for top earners as a condition for negotiations? It would be rather imprudent of him not to have. Market continues to squirm on the ‘cliffs’ concern. Time is shortening; the market may be required to experience a period of self induced ‘free-falling’ before all concerned can come to some mutual agreement that’s expected to kick that ‘can’ further down the road.

With November’s US employment report out on Friday, expect the market to focus on this morning’s Stateside ADP employment release. Currently, investors are looking for a +125k print, a tad below last months, but a print that that could nudge the median consensus to think about readjusting their employment expectations a tad higher this Friday from their current expectations of +93k to +100k reading. When it comes to employment, a higher number suits just about everybody.

Later this evening, and similar to its largest trading partner, Australia, earlier in the week, the RBNZ is widely expected to leave their overnight cash rate unchanged at an historical low of +2.5%. The plethora of reasons being applied is supportive of said outcome. Kiwi data released since the last policy meet has been slightly better on balance; while Q3 employment was weak, activity outlook and the housing market have continued to improve, leading many to expect a better tone in the statement on domestic activity. Similar to most Central Bank rhetoric of late about their currencies, the following press conference will likely indicate that NZD strength has and is dampening New Zealand’s recovery. Be weary, market participants are trying to get a better handle on the new governor’s policy stance. A dovish RBNZ will again put massive pressure on NZD.

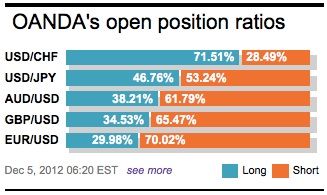

EUR price action continues to track the Bollinger Bands higher. The day indicators are retaining a bullish bias. Many participants are concerned that they may be missing out and it seems that some individuals are contemplating raising their single unit bid. Chasing a market is not always a fruitful strategy. As long at the ECB’s OMT program keeps market sentiment well supported, EUR bulls may have their opportunity to achieve their upper echelon.

Again this morning, the EUR has found itself in new territory. The single currency looks to have room for further upside movement as the short positions in EUR remain significant and the recent upwind of further bets against the currency could push the EUR outright higher. Consensus has found that intraday traders are looking to reload and go long the single unit on reasonable dips. The trend remains with the buyer above the 1.2881 low mid-last week. Be weary that the further we go deeper into the month of December, fundamentals and technical can sometimes be easily tossed to the wayside!

Other Links:

EURO’s course of action has not changed

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019