It’s remarkable, Capital Markets remain composed; most likely due to the fact that investors have gotten used to the last minute Euro solutions. From current levels, the recovery potential for the ‘single’ currency is limited if a solution is found. Failure and the EUR will come under considerable downward pressure, as it will almost become unavoidable that Cyprus will leave the Euro-zone. The EUR weakness could be brief as the ECB will be quick to react to calm the markets through their OMT or the ELA programs.

This is going to be a long weekend for three certain interested parties, Cyprus, Russia and the ECB. The fact that the Cypriot bank holiday has been extended until next week is telling the market how far apart all concerned parties have been from the original plan. The so-called ‘contained situation’ has the three looking at each other for an alternate solution. Talks with Russia and Cyprus ended with no agreement yesterday. The Cypriot alternative did not suit the Troika contingent even with the ECB in the background threatening to pull its liquidity.

Monday is D-day. If Cyprus cannot agree on a bank levy for deposits as part of a EU bailout, then it will have to either wind down its biggest banks – potentially wiping out depositors – or leave the Euro-zone. The island has three days to get their house in order before the ECB cuts off emergency funds for troubled Cypriot financial institutions. Without these funds it would lead to the collapse of the country’s biggest lenders. Euro policy makers are rolling the dice and are banking on the country’s small size making their domestic problems ‘containable.’

Up until now, the market has been rather complacent with the Cypriot issues, and for good reason. We have been told time and time again that it’s a ‘special case and contained’. A +EUR10b blip is just that in the Euro grand scale of things. The Cypriot government is set to vote today on an alternative deal that involves restructuring the country’s second largest lender and placing restrictions on other financial transactions. Other peripheral debt issues this week went very well, resulting in a healthy bid-to-cover ratio, in fact both Spanish and Italian bonds have managed to rally a tad. However beware, with little macro data to feed the frenzy this Friday, we should expect some prudent risk pairing as we head into the weekend without a solution.

Upbeat US data is being drowned out by Cyprus. This supposedly ‘isolated’ case is putting Draghi’s do “whatever it takes” to preserve the 17-member to the test. The small, but not insignificant +EUR10b problem, without ECB backing, could possible raise contagion fears throughout the periphery region. This would pressure periphery bond yields to rally higher, again putting the onus back onto the ECB to stick to its original pledge. In fact, the Cypriot tensions could be described as “continuing political risks to the Euro-zone’s diminishing pro-euro consensus.” Another issue is that Euro-policy makers repeatedly make the same mistake, it seems that they do not take into consideration human nature and reactions or if they do they are not very good at it.

The possibility of a negative impact on public opinion is significant – even if the Cypriot deposit levy were to be discarded. Failure to pass the measure may lead the ECB to exert its threat and decide to stop the emergency liquidity assistance to Cypriot banks, which could have significant consequences for country – ranging from bank default, capital flight (especially from Russia) and, perhaps most significantly, the risk of capital outflows in other Euro-zone member states. It’s humane nature to be concerned –however humane reactions are not pre-measurable.

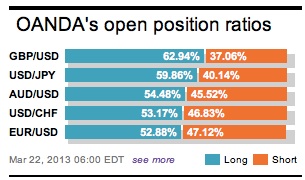

The EUR’s upside potential is beginning to look increasingly limited, as the currency starts to price in the greater economic and systemic risks, even if a bailout is formulated and agreed upon over the weekend. Both JPY and CHF are beginning to feel the heat of “appreciation,” a factor that both central banks, BoJ and SNB, have worked tirelessly to weaken. The USD/JPY is lower not entirely for risk aversion, but with a market that is disappointed that the new BoJ head, Kuroda, did not announce any new measures at his first press conference. The fact that the Yen is being bought after stronger US data is revealing. Investors seem to want to pair back their exposure on the short Yen “lemming” trade. Even Japan’s fiscal year end should be Yen positive.

German business confidence deteriorated unexpectedly this month, the first time in five-months. The Ifo business survey fell to 106.7 from 107.4-m/m. Digging deeper, the current conditions component and expectation index were also below forecast. This will certainly cast doubt about Germany’s ability to recover from a weak Q4. Combined with other data this week, the Ifo probably suggests subdued German growth this quarter. Even though Germany is the backbone of Europe, it cannot isolate itself entirely from the economic woes of its neighboring Euro-partners, eventually the bad does penetrate.

The EUR remains above its 200-DMA at 1.2880. The weight of the Euro bad data and Euro negative news (Cyprus and Italy’s 5-star to seek referendum on the EUR) should limit recoveries as market sentiment prefers to sell the single currency on rallies at the moment. Below 1.2880 the market is looking at a new playing field, with a lot of open territory.

Other Links:

Flashing Red Data Knocks the Wind Out Of The EURO

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019