The ongoing trade turmoil and its implications for global growth is helping to boost precious metals. The energy sector is struggling however, while agricultural commodities have taken a hit following the latest USDA WASDE report.

Precious metals

Speculative investors boosted net long GOLD positions to the highest since September 2016, according to the latest data as at August 6 from CFTC. Gold soared the most in seven weeks last week amid falling global yields, global recession fears and potential currency turmoil. The metal was given an additional lift after Trump said Friday the proposed US-China trade negotiations scheduled for next month could be canceled. Exchange-traded funds (ETFs) had increased their physical holdings of gold for a 10th straight day, Bloomberg reported yesterday.

Gold has extended the gains into this week, hitting the highest level versus the greenback since April 2013. Gold is rising toward the 61.8% Fibonacci retracement of the 2011-2015 drop at 1,587.

Gold Monthly Chart

Source: OANDA fxTrade

SILVER likewise is benefiting from the global turmoil, rising to the highest since February 2018 in early trading this morning. Speculative investors used last week’s rally to book some profits as they were net sellers of silver for the first time in four weeks, the latest CFTC data show. That pulled net long positions from their most bullish since November 2017.

The gold/silver (Mint) ratio has been trading within the parameters of resistance at the 55-day moving average at 89.85 and support at the 200-day moving average of 86.25 since July 18.

PLATINUM has been trading conservatively over the past week, with moves and volatility kept to tight ranges, which meant speculative accounts turned net sellers of the precious metal for the first time in four weeks.

PALLADIUM has started this week positively, adding to last week’s gains. The commodity is slowly climbing from two-month lows and has eyes on the 55-day moving average at 1,479.5. That moving average has capped prices since the beginning of the month.

Base metals

COPPER is struggling to maintain any upward momentum after touching seven-month lows last week. With no discernable satisfactory conclusion to the US-China trade war in sight, demand expectations for the industrial metal continue to be scaled back. Speculative investors are most bearish on the metal since records began in 1993. This bearish mood continues despite data showing that copper stocks in warehouses monitored by the London Metal Exchange are the lowest in more than a month as at August 9.

Energy

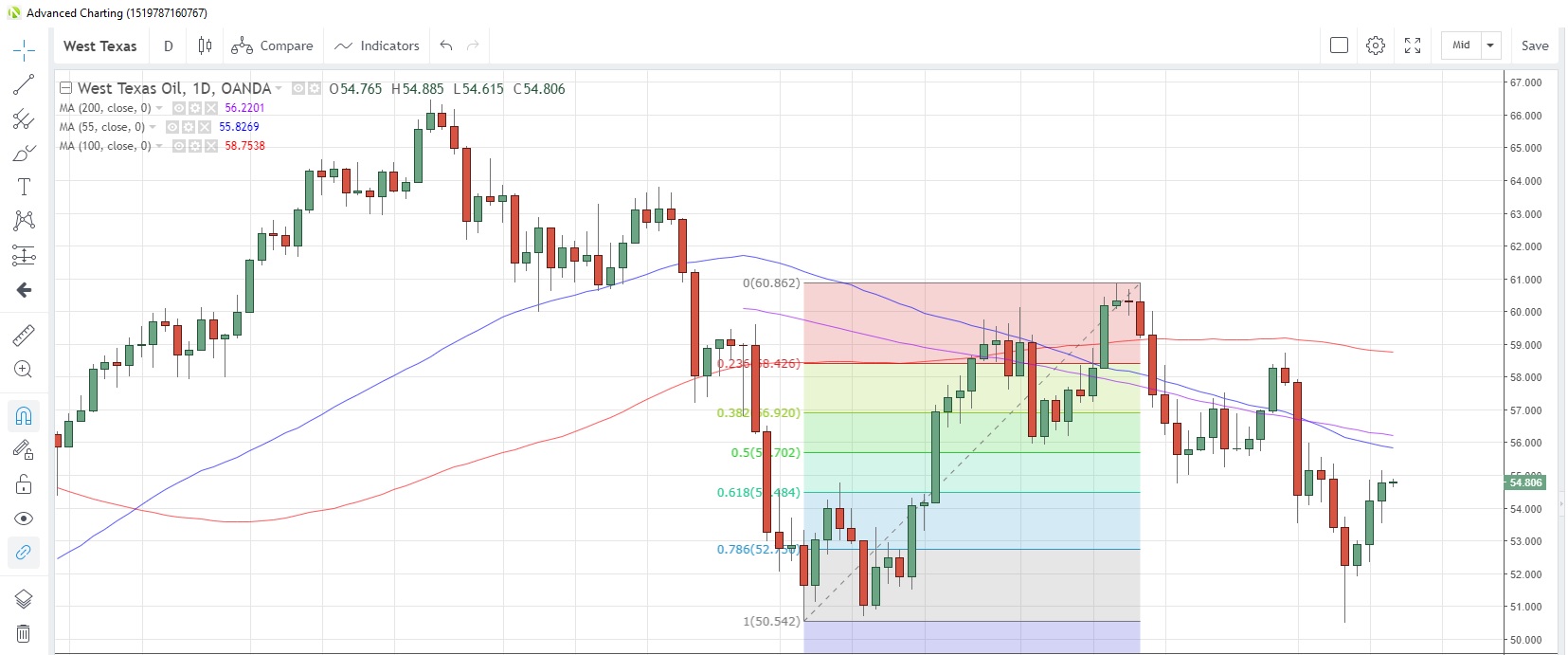

CRUDE OIL looks set for a fourth daily gain in a row today ahead of the weekly crude oil stockpiles data from the American Petroleum Institute. Last week saw a drawdown of 3.4 million barrels, the eighth consecutive weekly drain. On the supply front, weekly data from Baker Hughes highlighted that the number of US oil rigs in production fell for a sixth week and are now at the lowest since January.

West Texas Intermediate (WTI) is currently at $54.78 after touching $55.16 yesterday, the highest in a week. The current rebound in oil prices has helped WTI recover from losses of as much as 12.7% this month as demand fears remained elevated by the US-China trade standoff. IEA has trimmed its 2019 and 2020 demand forecasts to 1.1 million barrels per day (bpd) for this year and to 1.3 million bpd for next year.

WTI Daily Chart

Source: OANDA fxTrade

NATURAL GAS remains under pressure with this month’s losses contributing to a nine month losing streak, the longest negative period since 2008/09. Gas prices may find some support at current levels amid forecasts of higher than normal temperatures across the entire US for the August 17-21 period. Data from the EIA showed an increase in stockpiles of 55 billion cubic feet (bcf) in the week to August 2, less than the 59 bcf forecast but the 19th consecutive increase in reserves.

Agriculturals

CORN prices slumped Monday after the US Department of Agriculture (USDA) published its latest World Agricultural Supply and Demand Estimates (WASDE) report. In the report, the USDA raised the average US corn yield while increasing overall corn production.

Corn acreage was trimmed to 90 million from the previous estimate of 91.7 million, while production was seen at 13.9 billion bushels, up from the July estimate of 13.8 billion. Some suggest that the data provides further evidence that, as a result of the trade war, more farmers are switching to corn production from soybeans. On the demand side, China’s Agriculture Ministry raised its 2018/19 imports forecast by 700,000 tonnes to four million tonnes.

Corn fell the most since July 2013 yesterday and has extended losses in early trading this morning, to touch the lowest level since May 17. From a technical perspective, the commodity is heading toward the measured objective of a head and shoulders reversal pattern below 3.60.

Speculative investors trimmed their net long positions for a third straight week in the week to August 6, according to CFTC data. Net longs are now at the lowest since the week of May 28.

Corn Daily Chart

Source: OANDA fxTrade

WHEAT prices posted the biggest daily loss on record yesterday after the USDA WASDE report. The report bumped up US wheat production by 3% to 1.98 million bushels while boosting its forecast for 2019/20 season-end stocks by 1.5% to 27.6 million tons.

Saudi Arabia announced last week that it was relaxing its import rules, including stipulations about the maximum percentage a batch can suffer bug damage. This would open the way for Russian suppliers to tender for shipments. While on Russia, the USDA WASDE report cut its estimate for Russian wheat output for the 2019/20 season by 1.6% to 73 million tons.

Wheat prices slumped to the lowest since May 24 yesterday and opened below the 100-day moving average for the first time since August 2.

SOYBEAN prices were also dragged lower by the WASDE report, which halted a three-day rising streak. China cut its 2018/19 soy imports estimates by 1.5 million tonnes to 83.5 million tonnes due to lower shipments in July. Speculative investors were net sellers for a third consecutive week.

SUGAR attempted a rebound from 10-month lows late last week but the two-day rally was halted yesterday. Sugar is now at 0.1146 with the 55-day moving average at 0.1201.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Andrew Robinson

Latest posts by Andrew Robinson (see all)

- RBA cuts rates on virus impact - 2 March 2020

- Commodities Weekly: Oil rises first time in eight days - 2 March 2020

- Daily Markets Broadcast 2020-03-03 - 2 March 2020