Thursday March 14: Five things the markets are talking about

Market focus remains on the U.K and they are not done voting yet.

Yesterday, U.K MP’s voted to reject a no-deal Brexit, it’s not a legally-binding decision and it does not rule out the U.K leaving the E.U, but it means MP’s now get to vote on delaying Brexit.

And guess what? That vote takes place later today (03:00 pm EDT), and if it is passed and the E.U agrees to it, the UK will not leave the E.U as planned on March 29. PM May is expected to ask for an extension lasting about two months.

Elsewhere, equities were mixed in Asia and little changed in Europe after Chinese retail sales data was in line with expectations and industrial production data slightly below. Sovereign yields are steady while the ‘big’ dollar trades mixed and crude prices are higher, supported by a decline in U.S crude and fuel stockpiles, adding to evidence of a tightening market.

On tap: Later this evening, BoJ Governor Kuroda will give a press conference after the board conclude their discussions on monetary policy.

1. Stocks mixed showing

In Japan, the Nikkei ended little changed overnight after China reported a mixed bag of data that renewed investor worries about the global economy. The Nikkei share average ended -0.02% lower, while the broader Topix dropped -0.2%.

Down-under, Aussie shares snapped four days of losses as miners gain, while financials capped gains on regulatory uncertainty. The S&P/ASX 200 index ended up +0.3%. The benchmark was down -0.2% yesterday. In S. Korea, the Kospi stock index rallied +0.34% overnight as foreigners turned net buyers.

In China, stocks fell overnight, extending this week’s losses, after data showed that growth in industrial output plunged to a 17-year low in the first two-months of 2019, reinforcing investor concerns over a slowing economy. At the close, the Shanghai Composite index was down -1.2%, while China’s blue-chip CSI300 index was down -0.69%.

In Hong Kong, stocks edged a tad higher after China reported stronger-than-expected investment in its slowing economy, but gains were capped on a disappointing industrial output number. The Hang Seng index ended +0.2% higher, while the Hang Seng China Enterprises index rose +0.4%.

In Europe, regional bourses are trading higher across the board, with the exception of the FTSE 100, which is underperforming on continued strength in the pound.

U.S stocks are set to open in the ‘black’ (+0.13%).

Indices: Stoxx600 +0.72% at 378.00, FTSE +0.36% at 7,184.71, DAX +0.43% at 11,622.16, CAC-40 +0.70% at 5,343.77, IBEX-35 +0.90% at 9,274.99, FTSE MIB +0.93% at 20,941.50, SMI +2.01% 9,447.50, S&P 500 Futures +0.13%

2. Oil hits four-month highs on tighter supply numbers, gold prices fall

Crude oil futures have reached a four-month high earlier this morning, as a production curb agreement by OPEC, coupled with U.S sanctions on Iran and Venezuela tightened global supplies.

The ‘black stuff’ also found support from yesterday’s unexpected dip in U.S crude oil inventories.

In the euro session, Brent crude oil futures hit an intraday high of +$68.14 per barrel before easing to +$67.05, up +50c or +0.74% from yesterday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$58.62 per barrel, up +36c, or +0.62%.

Oil prices have been receiving broad support this year from supply cuts by OPEC aimed at tightening markets. Earlier this week, Saudi Arabia announced further plans to cut its crude oil exports in April to below +7M bpd, while keeping its output “well below” +10M bpd. That compares to production of around +10.14M bpd last month.

Also supporting prices is the political and economic crisis in OPEC-member Venezuela, while stateside, the U.S Energy Information Administration (EIA) indicated yesterday that commercial crude oil inventories fell last week as refineries hiked output.

Note: U.S crude oil production also dipped, falling by -100K bpd to +12M bpd.

Ahead of the U.S open, gold prices have eased a tad as the ‘big’ dollar regained some ground and uncertainty over Brexit eased, but the ‘yellow’ metal trades atop of its two-week high hit yesterday as tepid U.S inflation data strengthened market expectations that the Fed remains on hold. Spot gold is down -0.5% at +$1,302.90 per ounce. U.S gold futures have also dipped -0.5%, to +$1,302.40 an ounce.

3. Euro-sovereign yields push higher

Investors seem keen on selling safe-haven eurozone government bonds this morning, pushing sovereign yields higher, as the U.K’s parliament’s rejection of a “no-deal Brexit” is boosting risk sentiment. However, the markets uncertainty over the next steps is limiting the sell-off.

The German 10-year Bund yields has backed up +2 bps to +0.086%, but still not far from its two-year lows of +0.048% hit earlier this month. Other high-grade eurozone bond yields are also +1-2 bps higher.

In the U.K, Gilt yields are sharply higher, with 10-year yields up nearly +5 bps on the markets expectations that a favourable outcome on Brexit would allow the BoE to hike rates later in 2019.

Elsewhere, the yield on 10-year Treasuries are little changed at +2.62%.

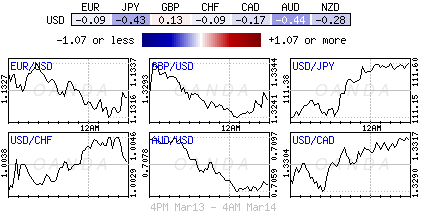

4. Sterling off highs, waiting for extension vote

The pound (£1.3233) has pulled away from its multi-month highs against the USD and EUR reached yesterday after the U.K parliament voted against leaving the E.U without a deal. Market focus now turns to another parliamentary vote this afternoon (03:00 pm EDT) on a short extension to Article 50. Delaying Brexit further is more or less fully priced in. GBP is down -0.3% at £1.3246, off a nine-month peak of 1.3382 reached late Wednesday.

The JPY is a tad softer ahead of this evening’s Bank of Japan (BoJ) rate decision. Current market thinking believes the BoJ could take a more “dovish” stance with growing expectations that the next policy move could be towards another easing. It would be the first in three-years. Policy makers are expected to cut their overall assessment due to the recent slowdown in Chinese economic data. USD/JPY is higher by +0.3% at ¥111.60.

5. German inflation holds steady

Data this morning from the Federal Statistical Office showed German inflation remained stable last month, endorsing a preliminary estimate.

The annual inflation rate (measured by harmonized E.U standards) measured +1.7%, the same rate as in January and in December 2018.

Digging deeper, energy prices in Germany rose +2.9% y/y, while prices for food and services both increased by +1.4%.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019