Support or a dressing down?

In the aftermath of the conflicting press reports about a possible shift in the US stance on tariffs, risk appetite was still buoyant during the Asian session, though not aggressively so. As a follow-on from yesterday’s headlines, is was announced that Treasury Secretary Mnuchin is due to meet President Trump at the White House later today. Is it to set a plan in motion to cut tariffs to get a deal or will he be asked to explain his thoughts? It could get interesting.

Meanwhile Trump has pulled the US delegation out of the global economic forum in Davos just after he’d prevented House Speaker Pelosi a plane to visit Afghanistan, reportedly “out of consideration for” the 800,000 government workers who aren’t being paid. Coincidentally, Mnuchin was scheduled to lead the delegation.

Markets like the idea

Indices and equity futures were positive across the region in Asia, with gains ranging from 0.15% for the NAS100 to 0.62% for the Japan225 index. Risk currencies were better bid, with AUD/USD retesting the 0.72 level, while USD/JPY crawled higher to 109.32, still testing the 50% retracement level of the December 13 to January 3 drop at 109.292.

USD/JPY Daily Chart

Source: OANDA fxTrade

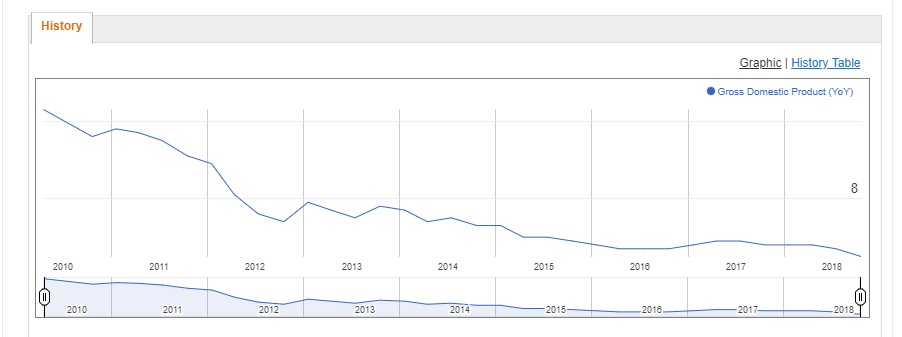

China growth to hit the spotlight next week

Ahead of Monday’s scheduled release of China GDP growth data for the fourth quarter, Chinese newspaper China Daily has repeated reports from January 11 outlining that China will target 2019 growth of between 6.0% and 6.5%.

The data for Q4 is expected to show a slowdown in growth to 6.4% y/y from 6.5% in Q3, which was the lowest since Q1 2009. China’s 2018 official growth target is about 6.5%. Separately, the National Bureau of Statistics today announced a downward revision to 2017’s growth to 6.8% from 6.9%.

China’s downward growth trajectory

Source: MarketPulse

Retail sales to confirm a difficult UK Christmas

UK retail sales data for December are due today, and are expected to show a drop of 0.8% m/m in the headline and -0.6% excluding fuel. This would confirm anecdotal evidence from High Street retailers for the period.

In other data, Canada releases consumer price data for last month, which are expected to decline 0.4% m/m, matching the decline seen in November while the US has industrial production and capacity utilization on tap.

Analysts are currently not expecting the surprise jump in the Philadelphia Fed manufacturing survey yesterday to be repeated in the Michigan consumer sentiment index today. It is expected to fall to 97.0 from 98.3, which would be the lowest since August last year.

The full MarketPulse data calendar can be viewed at https://www.marketpulse.com/economic-events/

Have a great weekend.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Andrew Robinson

Latest posts by Andrew Robinson (see all)

- RBA cuts rates on virus impact - 2 March 2020

- Commodities Weekly: Oil rises first time in eight days - 2 March 2020

- Daily Markets Broadcast 2020-03-03 - 2 March 2020