Thursday January 3: Five things the markets are talking about

The U.S dollar fell aggressively on Wednesday evening (17:30 pm EDT), causing a brief currency crash in the U.S/Asian desk handover, on risk aversion rising due to falling equities in the U.S and after Apple’s warning that sales in China have been weak.

Apple cut its Q1 guidance for the first time in 20-years, citing an unforeseen slowdown in China and fewer upgrades to its flagship mobile device.

Coupled with weaker Chinese manufacturing data this week, Trump’s U.S protectionist confrontation is starting to have an impact on economic activity, and this despite U.S President implying, via rhetoric and social media, that a Sino-U.S trade deal is within grasp.

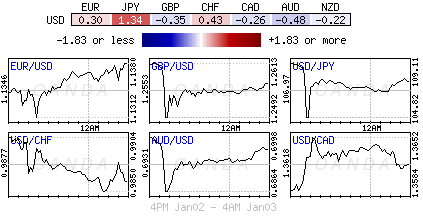

The dollar fell outright versus the safe-haven yen to a nine-month low of ¥104.79 and is last trading down by -0.8% at ¥107.73. EUR/USD is up by +0.2% at €1.1370.

The lack of market liquidity – Tokyo has been on holiday all week and does not return until this evening – and some assertive short-yen positioning, has helped to push some aggressive currency moves in what is know as the ‘twilight zone,’ as trading shifted from the North American session to the open of the Australasian markets. Also, various algorithmic programs exacerbated the moves.

Elsewhere, U.S Treasuries trade steady, while most Euro sovereign bonds have climbed. WTI crude futures have again slipped as it reversed some recent gains on the back of Saudis’ lowering exports. Gold prices have rallied.

On tap: PM Theresa May will today meet with EC President Tusk, German Chancellor Merkel and Dutch Prime Minister Rutte. She is reportedly hoping to win concessions on the Irish border backstop.

1. Apple earnings warning rocks global shares

Asian and Euro equities have fallen sharply, led by a sell-off in the tech sector, and U.S stock futures point to a weaker open on Wall Street this morning, after Apple cut its revenue forecast, its first downgrade in nearly a dozen years, citing weaker iPhone sales in China.

Note: In Japan, the Nikkei was closed in observance of the four-day Bank Holiday.

Down-under, Aussie shares closed +1.4% higher overnight as a ‘flash crash’ in the AUD (AUD/JPY fell -8% at one point) boosted the appeal of export-oriented stocks, with gold stocks topping the gains. In S. Korea, the Kospi stock index fell to a two-month low, down -0.81%, on Apples Q1 forecast news.

In China and Hong Kong, regional bourses falter as economic concerns take over. The Shanghai Composite index ended nearly flat, while the blue-chip CSI300 index fell -0.2%. In Hong Kong, the Hang Seng index edged down -0.3%, while the Hang Seng China Enterprises index closed flat.

In Europe, regional indices are trading mostly lower across the board with the tech sector in focus following Apples cut in Q1 revenue forecasts for iPhone sales in China.

U.S stocks are set to open deep in the ‘red’ (-1.65%).

Indices: Stoxx600 -0.69% at 334.50, FTSE -0.50% at 8,410.50, DAX -1.06% at 10,468.56, CAC-40 -1.02% at 4,641.50, IBEX-35 -0.39% at 8,517.00, FTSE MIB -0.81% at 18,182.50, SMI -0.20% at 8,410.50, S&P 500 Futures -1.68%

2. Oil prices decline on swelling oversupply, gold higher

Crude oil prices remain under pressure amidst volatile currency and equity markets, coupled with concerns that economic slowdowns this calendar year will cut into fuel demand just as global crude supplies are surging.

Brent crude futures are down -50c at +$54.41 a barrel, while U.S. West Texas Intermediate (WTI) crude oil futures have dropped -75c to +$45.79 a barrel ahead of the U.S open.

Note: Oil prices registered their first yearly decline in three-years in 2018 – Brent tumbled -20%, while WTI slumped -25%.

A number of factors are expected to provide further heightened volatility in the commodity space in Q1, 2019. There is the markets uncertainty on Sino-U.S trade; there is Brexit, as well as political instability and conflict in the Middle East. There is U.S shale output numbers and there is OPEC’s and Russia’s supply discipline. Oil markets are also under pressure from a surge in supply just as demand growth is expected to slow.

Note: U.S crude production stood at a record +11.7M bpd in late 2018, making the U.S the world’s biggest oil producer.

Ahead of the U.S open, gold prices scaled to a new six-month high earlier this morning as investor worries about a global economic slowdown, couple with equity markets volatility is supporting investor safe-haven buying, while a weaker dollar also offered some support.

Spot gold touched +$1,292.32 per ounce, and was up +0.4% at +$1,289.10. U.S gold futures are up +0.6% at +$1,291.20 per ounce.

3. Euro sovereign yields remain under pressure

Eurozone government bond yields have extended their fall in this holiday shortened trading week, as global growth concerns convince nervous investors to seek safe havens.

The rally in the core E.U bond markets may be overdone, however, given the economic and political uncertainty in markets, the risk is that yields will continue to decline.

After falling to levels unseen in two-years, the 10-year German Bund yield is trading just below +0.16%, down -1 bps overnight. Bond bears believe that the bounce higher in Euro bond prices is perhaps owed more to a lack of liquidity than any real turn in market sentiment, especially when considering that the ECB terminated its net asset purchases last month and that the usual start-of-the-year supply wave is about to begin.

Elsewhere, the yield on U.S 10-year Treasuries has rallied less +1 bps to +2.62%. In the U.K, the 10-year Gilt yield has dipped -2 bps to +1.191%, the lowest in more than three-weeks, while Italy’s 10-year BTP yield has jumped +4 bps to +2.728%, the biggest surge in almost two-weeks.

4. Dollar demise remains on track

Investors continue to err on the side of ‘risk aversion’ trading strategies now that Apples has cut its Q1 earnings guidance – this sent the markets safe haven currency of choice, the yen, higher across the board.

During the thin Asian trade, the yen spiked higher by over +7% against AUD (¥73.07) and while the USD/JPY pair tested below ¥105 handle (¥104.96).

Note: USD/JPY has since managed to re-approach the ¥108 level in the early part of the E.U session and after the ‘stops’ were triggered in Asia.

Elsewhere, EUR/USD is at €1.1365 and marginally higher with key resistance still seen at €1.15 level.

GBP/USD remains soft on investor concerns over a potential ‘no-deal’ Brexit ahead of the upcoming meaningful vote in the U.K parliament. The pound is at £1.2575 just ahead of the open stateside.

5. Sterling lower as U.K construction PMI falls to three-month low

The pound (£1.2575) has declined a tad after this morning’s U.K purchasing managers’ survey on construction activity fell to a three-month low of 52.8 in December, from 53.4 in November.

Note: Market consensus was looking for a headline print of 52.9.

“U.K. construction firms indicated a disappointing end to 2018 as business activity growth eased to a three-month low and new orders expanded at a relatively subdued pace,” the report said. However, “survey respondents cited hopes of a boost to growth from work on big-ticket transport and energy infrastructure projects in 2019.”

Note: U.K services PMI, due tomorrow (04:30 am EDT), is more important for pound investors given that the U.K. economy is heavily reliant on services.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019