Thursday November 8: Five things the markets are talking about

Equity euphoria continued in the overnight session as global stock markets extended their U.S midterm election rally, again supported by strong corporate earnings results.

However, U.S futures suggest a softer open to the North American session ahead of today’s Federal Open Market Committee (FOMC) monetary policy decision (02:00 pm EDT). The market will be looking for any signals on the pace of policy tightening over the next 12-months.

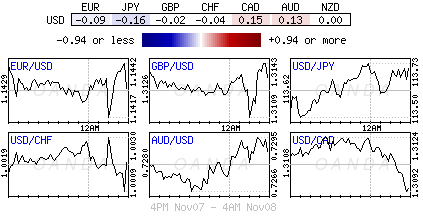

Elsewhere, currency markets saw a relatively tight range with the U.S dollar trading on the stronger side, again looking for cues on direction.

China trade data overnight showed a surge in exports and imports for last month, well ahead of the next round of tariff hikes in the trade war with the U.S.

Crude oil prices have found some traction after sliding for eight consecutive days. The continuing drop in prices is becoming a concern for OPEC and its allies, with the alliance now talking about reversing course and cutting production when they meet in Abu Dhabi this weekend.

1. Stocks get the green light for now

Equities have got the green light in the overnight session on optimism that U.S President Trump’s planned measures to boost business growth would continue despite the midterm election results.

In Japan, the Nikkei surged, tracking North American equities rally after Tuesday’s U.S midterm elections produced no major surprises. The Nikkei share average ended +1.8% higher at just over its two-week closing high, while the broader Topix rallied +1.7%.

Down-under, Aussie stocks also closed higher overnight, supported mostly by financial stocks. The S&P/ASX 200 index closed +0.53% higher, trading atop of its three-week high. In S. Korea, the Kospi rallied as Sino-U.S trade concerns eased a tad as China’s October exports beat market expectations. At close of trade, the index was +0.67% higher.

Note: China’s October exports rose +15.6% y/y, while imports expanded +21.4%.

In China, stocks gave up earlier gains and closed lower for a fourth consecutive session overnight, as the market remains anxious over the trade outlook and seeks reassurance of policy support for a slowing economy. The blue-chip CSI300 index was down -0.3%, while the Shanghai Composite Index lost -0.2%.

In Hong Kong, stocks edged higher, the Hang Seng index rallied +0.3%, while the China Enterprises Index gained +0.6%.

In Europe, regional bourses are trading mixed, with some indexes fading earlier gains following Asia’s mostly positive session.

U.S stocks are set to open in the “red” (-0.4%).

Indices: Stoxx600 +0.2% at 367.2, FTSE +0.1% at 7123, DAX -0.1% at 11563, CAC-40 -0.1% at 5134, IBEX-35 -0.1% at 9088, FTSE MIB -0.5% at 19451, SMI +0.4% at 9088, S&P 500 Futures -0.4%

2. Oil rises after record Chinese imports, gold lower

Oil is a tad better bid; recovering from this week’s three-week lows, after record Chinese crude imports eased some investor concerns that demand from the world’s largest buyer may be waning just as global supply is rising.

Data overnight showed that China’s crude imports rose +32% in October y/y to +9.61M bpd.

Brent crude futures have rallied +71c to +$72.78 a barrel, while U.S light crude (WTI) futures have gained +55c to +$62.22.

Record U.S crude production and signs from Iraq, Abu Dhabi and Indonesia that output will grow more quickly than expected over the next 12-months has managed to pressure crude prices over the past fortnight and is expected to cap further gains.

OPEC meets this weekend, and there are market whispers that a production cut could be in the works to support crude prices.

Ahead of the U.S open, gold prices have fallen to trade atop of this week’s low as the dollar and stocks rally. Investors are turning their attention to the Fed rate decision this afternoon. Spot gold is down -0.3% at +$1,222.31 per ounce, after hitting its lowest since Nov. 1 at +$1,221.1 earlier in the Euro session.

U.S gold futures are -0.2% lower at +$1,226.3.

3. Fed expected to stick to gradual interest rate hike

The market is expecting little change to the U.S Fed interest-rate announcement this afternoon. The Fed is expected to maintain the target range for the key rate at +2% to +2.25%.

With the consensus pricing in a +25 bps December hike, the board is expected remain consistent with its “gradual” hiking communication. The U.S’s strong growth outlook and tightening labor market will allow for hikes to continue in 2019, but its the pace of hikes that the markets want to see – has their views changed with the recent equity volatility?

Elsewhere, the yield on U.S 10-year notes has eased -2 bps to +3.22%, the biggest fall in almost two-weeks. In Germany, the 10-year Bund yield has climbed +1 bps to +0.46%, the highest in almost three-weeks, while in the U.K, the 10-year Gilt yield is unchanged at +1.559%.

Finally, the 10-year Italian BTP-German Bund spread continues to hover around +300 bps – rising above or falling below this level depending on the political news flow and Italian budget updates.

4. EUR and Sterling beginning to struggle again

The EUR (€1.1407) is starting the N. American session at its overnight lows, paring back most of the gains it made in yesterday’s session on the back of the U.S midterm elections.

With no immediate change expected to U.S trade policies or an infrastructure program as a result of the Democrats winning the House, it should be difficult for the single unit to gain any significant traction outright in the short-term.

The E.U Commission updated its forecast (see below) and saw the Italian budget deficit rising to +3.1% in 2020. The Italian government has yet to submit a revised budget plan approach, but have stressed they would not change the budget law for 2019.

The pound (£1.3100, down -0.3%) cannot find any meaningful support as long as the Irish border issue is not solved. Media reports this morning indicate that the U.K cabinet were asked to look at a draft copy of the Brexit withdrawal agreement yesterday, which did not include the final working on the Irish border backstop.

5. E.U economic forecasts

In its quarterly economic forecast, the EU expects eurozone economy to “cool” this year, and over the coming years as global demand regions exports fades, with a sharper slowdown possible if the U.S economy overheats or trade wars escalate.

The EU still expects GDP for the 19 blocs that use the EUR to grow by +2.1% this year, having expanded by +2.4% in 2017 – the best year in a decade.

The bloc has cut its 2019 growth forecast to +1.9% from +2% in July and now projects a further slowdown to +1.7% in 2020.

The EU also used this quarterly economic forecasts to increase the pressure on Italy’s government over its borrowing plans, projecting the country’s budget deficit will exceed the upper limit set by the bloc in 2020.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019