Tuesday October 9: five things the markets are talking about

The first day back in a holiday-shortened trading week again sees U.S Treasury yields creeping higher, trading atop of their seven-year high yields. This aggressive backing up of sovereign yields this month is again putting pressure on risk assets.

However, overnight, equities traded mixed, with Asian bourses and U.S futures on the back foot, while Euro stocks have been able to move higher.

Yesterday saw the biggest one-day sell off in three-months of China stocks despite the People’s Bank of China (PBoC) cutting its RRR for the third time this year. Their easing actions have again put pressure on the yuan, which is sure to annoy Washington.

The IMF has cuts world 2018 and 2019 GDP forecast by -0.2% to +3.7%. It’s the first cut in two-years as the risk of balance has shifted to the downside due to escalating trade conflicts and tighter financial conditions.

On tap: The U.S Treasury is auctioning +$230B worth of debt this week. On Friday, the IMF and World Bank will hold meetings in Bali, with the world’s finance chiefs.

1. Stocks mixed results

Global risk aversion has put the yen (¥113.17) in demand, which is hurting Japanese stocks. Overnight, the Nikkei fell to a three-week low after stocks of firms with exposure to China weakened on worries about its economy while chip equipment makers tumbled, tracking weakness in U.S tech firms’ overnight. The Nikkei share average ended -1.3% lower, while the broader Topix dropped -1.8%.

Down-under, Aussie shares have also extended their sharp declines from Monday overnight; trading atop of their four-month lows, on investor concerns over growth outlook for the country’s largest trading partner China hurt sentiment. The S&P/ASX 200 index fell -1% at the close of trade, after losing -1.4% yesterday. In S. Korea, the Kospi was closed for a holiday.

In China, stocks rebounded overnight from Monday’s steep losses as authorities took further steps to support the economy and contain the effects of an escalating trade war with the U.S. The Shanghai Composite index closed +0.2% higher, while the blue-chip CSI300 index was up +0.3%. In Hong Kong, the Hang Seng closed down –o.1%.

Note: Dealers attribute yesterday’s steep losses in China to investors playing catch-up after a weeklong holiday, during which a sharp sell off in global bond markets had dragged down equity markets.

In Europe, regional bourses are trading mixed in quiet trading thus far.

U.S stocks are set to open in the ‘red’ (-0.3%).

Indices: Stoxx600 0% at 372, FTSE +0.1% at 7238, DAX -0.1% at 11938, CAC-40 0% at 5301, IBEX-35 +0.3% at 9232, FTSE MIB +0.3% at 19900, SMI -0.2% at 8951, S&P 500 Futures -0.3%

2. Oil prices rise as Iranian crude exports fall, gold higher

Oil prices remain better bid, as further evidence emerges that crude exports from Iran, OPEC’s third-largest producer, are declining before the imposition of new U.S sanctions. Also providing price support is a slow hurricane in the Gulf of Mexico.

Brent crude is up +55c at +$84.46 a barrel, after having fallen as low as +$82.66 yesterday. Brent hit a four-year high of +$86.74 last week. U.S light crude (WTI) is up +45c at +$74.74.

According to tanker data and an industry source, Iran’s crude exports fell further in the first week of October, as buyers sought alternatives ahead of U.S sanctions that are to take effect on Nov. 4.

Iran exported +1.1M bpd of crude in the first week of October, down from at least +2.5M bpd in April – before President Trump imposed sanctions.

Saudi Arabia, the biggest producer in the OPEC, said last week it would increase crude output next month to +10.7M bpd, a record. The market will wait to see if they follow through.

Meanwhile, oil companies operating in the Gulf of Mexico have closed -20% of oil production as Hurricane Michael moves toward the eastern Gulf States including Florida.

Ahead of the U.S open, gold prices are better bid on risk aversion amid concerns over a potential slowdown in China’s economic growth. Spot gold is up +0.2% at +$1,189.58 an ounce.

Note: Yesterday, it fell -1.2%, its biggest one-day percentage fall since the middle of August, and also touched a more than one-week low of +$1,183.19.

3. Sovereign yields on the move

On the weekend, China cut its Required Reserve Ration (RRR) for major banks by -100 bps to +14.50% to prevent the country’s credit conditions from getting too ‘tight.’ The PBoC’s easing bias highlights their policy divergence with the Fed.

The impact from Sino-U.S trade tensions is to become more noticeable in coming quarters, so an easing bias in monetary policy, coupled with an expansionary fiscal policy is expected to support China’s economy. The PBoC stated that it would continue with “prudent and neutral” monetary policy. Will investors buy into Beijing’s policy-easing measures or do they require more market-orientated reforms?

In Italy, BTP yields have backed up to new highs after Economy Minister Giovanni Tria addressed the parliament on the government’s budget plans. He called for a “constructive discussion with Brussels over the budget” and said Italy’s “structural deficit will recover once GDP and employment returns to pre-crisis levels.”

Italy’s five-year bond yield rose to +3.042%, its highest level in almost five-years, while 10-year bond yields hit a new 5-year high at +3.63%.

Elsewhere, the yield on 10-year Treasuries has advanced +2 bps to +3.25%, hitting the highest in more than seven-years with its fifth consecutive advance.

Note: The U.S treasury is to auction +$230B worth of debt this week.

In Germany, the 10-year Bund yield has climbed +3 bps to +0.56%, while in the U.K, the 10-year Gilt yield has increased +4 bps to +1.714%.

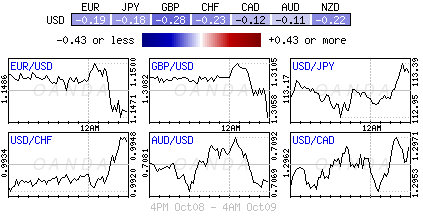

4. Dollar supported by yields

The USD is maintaining its firm tone across the G10 currency pairs as U.S Treasuries are still holding last week’s gains in yields.

Rising Italian bond yields continue to weaken the EUR (€1.1460), but major falls are not in the cards as long as the ‘single’ unit’s existence is not threatened, and as long as the ECB indicates ‘whatever it takes’ promise is in place. EUR/USD is last down -0.25% at €1.1460 even though 10-year Italian yields reach +3.628%, just shy of yesterday’s 2018 high of +3.631%

China’s effort to support its decelerating economy continues to heap pressure on the yuan. The yuan weakened beyond ¥6.93 this week, coming within striking distance of its lowest level in nearly two-years, after China moved over the weekend to free more funds for domestic banks. The currency briefly recovered to around ¥6.91 earlier this morning.

5. German exports slipped in August

Data this morning showed that German exports slipped for the second-straight month in August, which may suggest that, the Sino-U.S trade conflict are dampening demand for goods.

According to the Federal Statistical Office, the total exports of goods fell -0.1% in August from the month before, while imports of goods dropped -2.7% in the period.

Note: German exports stumbled in August despite a weaker EUR. The EUR traded around $1.14 in mid-August compared with levels around $1.25 in early February.

Germany’s adjusted trade surplus stood at €18.3B in August, undershooting a consensus forecast of €19.0B and a surplus of €21.3B in August last year.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019