Tuesday September 4: Five things the markets are talking about

In the last week of August, it was trade and tariff wars along with EM currency capitulation that were the driving forces behind asset prices.

Thrown into the mix, G10 central banks and geopolitical risks, the month of September volatility should not disappoint.

Topping investors’ agenda this week is the Sino-U.S trade dispute and Canada Nafta talks, which are both threatening to escalate along with EM fallout as Argentina’s austerity measures shake emerging markets.

Note: Trump may announce implementation of tariffs on as much as +$200B in additional Chinese products as soon as Thursday.

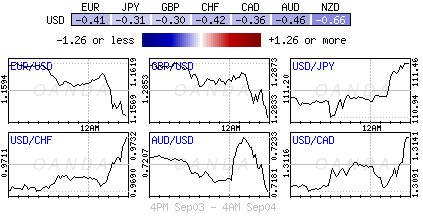

Brexit discussions are again pressuring sterling (£1.2830), now that the market is pricing +25% odds that Britain could leave the E.U next March without a deal.

Currently, Euro stocks are climbing and U.S futures point to a higher open this morning after a listless session in Asia. The ‘big’ dollar again has found some momentum and EM stocks have pushed higher for the first time in a week

On the data front, the first of the month brings final PMI readings for manufacturing, services and a composite reading. Down-under, Australia releases Q2 GDP data this evening and Canada will release its important merchandise trade (Sep 5) and employment report (Sep 7). The Bank of Canada (BoC) is expected to hold rates steady tomorrow (Sep 5).

Stateside, international trade, construction spending, factory orders and Friday’s non-farm payrolls (NFP) are the key releases this week.

1. Some Asian stocks rally after early losses

On the whole, Asian shares rallied overnight, but investors remain apprehensive as the Sino-U.S trade dispute threatens to escalate this week.

In Japan, the Nikkei edged a tad lower, falling -0.1%, after trading often between positive and negative territory. The broader Topix also fell -0.1% as investors wait to take their cue this week from the states.

Down-under, Aussie shares fell overnight as reports of fresh investigations into financial institutions kept investors on edge. The S&P/ASX 200 index dropped -0.3% at the close of trade. In S. Korea, the Kospi stock index rallied +0.38%, following the turnaround in Chinese shares, despite the escalation of a Sino-U.S tariff war.

In Hong Kong, stocks ended higher as telecom shares rallied on merger speculations. The Hang Seng index ended +0.9% higher, while the China Enterprises Index closed up +0.7%.

In China, equities snapped a five-day losing streak, as investors hunted for bargains in beaten-down real estate and banking stocks. However, pending U.S tariffs capped gains. The Shanghai Composite index closed up +1.1%, while the blue-chip CSI300 index ended +1.27% higher.

In Europe, regional bourses are trading mixed and are off their intraday high open. The FTSE trades little changed after outperformance yesterday ahead of testimony from BoE members in front of the Treasury select committee.

U.S stocks are set to open in the ‘black’ (+0.1%).

Indices: Stoxx600 -0.4% at 381.2, FTSE -0.2% 7493, DAX -0.7% at 12259, CAC-40 -0.7% at 5373, IBEX-35 -0.7% at 9380, FTSE MIB +0.2% at 20436, SMI -0.3% at 8980, S&P 500 Futures +0.1%

2. Oil rallies as Gulf of Mexico rigs evacuated, gold lower

Oil prices have rallied aggressively overnight on news of the immediate evacuation of two Gulf of Mexico oil platforms in preparation for a hurricane (Gordon).

U.S light crude has rallied +$1.31 a barrel from Friday’s close to +$71.11, its highest since mid-July, while Brent crude is up +$1.00 at +$79.15 a barrel.

Note: the jump is more significant since U.S crude did not trade Monday due to the Labour Day holiday.

Oil markets have tightened over the past four weeks, pushing up Brent prices by more than +10% as investors anticipate less supply from Iran as U.S sanctions on Tehran begin to hurt.

Ahead of the U.S open, gold prices are under pressure as the ‘big’ dollar hits a one week-high on the back of intensifying global trade tensions and economic worries in emerging markets. Spot gold is down -0.3% at +$1,196.90 an ounce, while U.S gold futures have dropped -0.4% at +$1,202.10 an ounce.

Note: The yellow metal is down -8% this year amid rising U.S interest rates, trade disputes and the Turkish currency crisis – the U.S dollar remains the safe haven currency of choice.

3. RBA to eventually raise interest rates

Reserve Bank of Australia (RBA) left their cash rate target unchanged at +1.50% as expected overnight and the accompanying statement was little changed from the last go-around. Policy makers reiterated their stance that low rates were supporting the economy and inflation, and that progress on unemployment/inflation is expected to be gradual. They saw GDP to average slightly higher than +3% in both 2019 and 2020.

In Europe, tame Swiss inflation data support the view that the Swiss National Bank (SNB) will not be raising rates before the ECB does (currently expected in September 2019). Data this morning showed that annual Swiss inflation was 1.2% last month, while core inflation was just +0.5%.

Elsewhere, the yield on 10-year Treasuries has gained +2 bps to +2.88%, the biggest advance in a week. In Germany, the 10-year Bund yield has climbed +2 bps to +0.35%. In the U.K, the 10-year Gilt yield has declined -2 bps to +1.404%, the lowest in more than a week.

4. EM rout not yet complete

The USD continues to find safe-haven support related to concerns about trade tensions as EM currency pairs suffer.

Yesterday, Argentine President Macri announced new taxes on exports and steep cuts to government spending in what he termed “emergency” measures to balance next year’s budget. The Argentine peso closed -3.14% weaker and is expected to face further pressure this week.

In Turkey, the Central Bank of the Republic of Turkey (CBRT) signalled yesterday that it would take steps to combat “significant risks” to price stability and also hinted of interest rate hikes. Investors have lost fait in the central banks independent authority – the TRY is trading down another -1% at $6.6920.

USD/INR has hit a fresh record high as the pair approaches $71.54 level. It’s expected that state banks have been selling U.S dollars on behalf of the Reserve Bank of India (RBI).

In South Africa, the country has officially entered a recession after this morning’s GDP data. Q2 GDP annualized q/q: -0.7% vs. +0.6%E; y/y: +0.4% vs. +1.0%E (moves into recession for first time since 2009) – USD/ZAR is up +2.25% at $15.2520.

In Europe, GBP/USD is lower for the fifth consecutive session, probing the lower end of the £1.28 handle as doubts continue to linger on Brexit negotiations and weaker UK PMI data (see below). Focus for the pound now shifts to the BoE Treasury-select testimony this morning where Governor Carney (08:15 am EDT) would likely be questioned on whether he plans to stay on beyond his June 2019 term end-date.

5. UK PMI data continues to miss expectations, but holds onto growth territory

Data this morning shows that the U.K’s latest purchasing managers’ index on construction activity fell to 52.9 in August, well below July’s 55.8 and below market expectations for a smaller fall to 54.9. Nevertheless, the index does remain in expansion territory.

Digging deeper, Markit reported a weak performance in housing activity, while civil engineering work decreased for the first-time in five-months. New business growth slowed, with Markit citing reports that Brexit-related uncertainty “continued to hold back investment spending.”

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019