Friday August 31: Five things the markets are talking about

The threat of global growth taking a hit from a damaging U.S-China relationship remains ‘front and center.’

Global equities trade under pressure in the last session of the month after U.S President Trump stepped up his tough talk on trade. The ‘big’ dollar and Treasuries both trade steady.

Ahead of the open, the Euro auto sector is again one of the big losers as Trump casts doubt on the scope of the E.U-U.S trade deal and after he suggested moving towards further tariffs on Chinese goods as soon as next week.

Emerging market currencies continue to experience the fall out of a plummeting Argentina peso. On contagion fears, the Indian rupee has dropped to a new record low outright, while South Africa’s rand slid to the lowest in two-years.

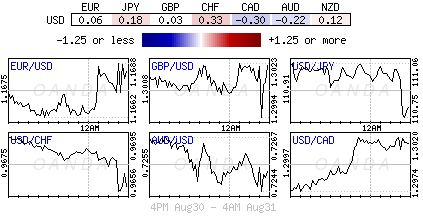

Elsewhere, the EUR (€1.1673) has edged a tad higher, while and the yen (¥110.75) trades somewhat steady. An exception, the Turkish lira, TRY (down -0.9% at $6.5822) has rallied after Turkey announced measures designed to encourage local currency saving, cutting a tax on lira deposits and increasing a tax on foreign currency deposits.

1. Stocks see red

In Japan, the Nikkei ended flat overnight, snapping an eight-session rally after President Trump said he is ready to quickly intensify ‘his’ trade war with China. The Nikkei has ended the day -0.02% lower after gaining +1.2% for the week and +1.4% for the month.

Down-under, Aussie shares fell on Friday, as investors feared an escalation in global trade wars. The S&P/ASX 200 index closed -0.5% lower, but added +1.2% for the week. In S. Korea, the Kospi closed down -0.07%. The index is down around -6.5% so far this year, and up by +0.75% in the previous 30 days.

In Hong Kong and China, stocks fall in renewed Sino-U.S trade war fears. Investor sentiment was also hurt by a slump in the index heavyweight Tencent, as Beijing’s proposed tougher measures against online gaming hit game operators. The Hang Seng index fell -1.0%, while the China Enterprises Index lost -0.8%. In China, the CSI300 index fell -0.5%, while the Shanghai Composite Index dropped -0.45%.

In Europe, regional bourses have opened lower across the board on global trade concerns. The Euro-auto sector is under pressure from reports that President Trump felt E.U tariff s are “not good enough,” while Italian stocks are under pressure due to the country’s exposure to Argentina.

U.S stocks are set to open in the ‘red’ (-0.04%).

Indices: Stoxx50 -0.8% at 3,404, FTSE -0.3% at 7,496, DAX -1.0% at 12,374, CAC-40 -0.7% at 5,438; IBEX-35 -0.7% at 9,400, FTSE MIB -0.5% at 20,391, SMI -0.5% at 8,993, S&P 500 Futures -0.04%

2. Oil prices dip on Sino-U.S trade worries

Oil prices are under pressure amid concerns that the Sino-U.S trade war could intensify, although looming U.S sanctions against Iran is limiting the decline.

Brent oil futures are at +$77.55 per barrel, down -22c, or -0.3% from Thursday’s close. U.S West Texas Intermediate (WTI) crude futures are down -6c at +$70.19 a barrel.

Nevertheless, with Venezuelan supply falling sharply and concerns around U.S. sanctions against Iran that will target its oil exports from November, crude prices this month are expected to record +4% rise for Brent and a +2% increase for WTI.

Note: The central theme for Q4 should be global trade disputes and their effects on economic growth and, by extension, fuel demand.

Ahead of the U.S open, gold prices rise, but are set for longest monthly losing streak in nearly six-years. Spot gold is up +0.6% at +$1,207.06 an ounce, after touching a near one-week low of +$1,195.95 yesterday. Prices are down -1.3% so far this month, and are on track for a fifth straight monthly decline. U.S gold futures are up +0.7% at +$1,212.80 an ounce.

3. Yields lower on risk aversion

Euro trade tensions are again at the forefront and are pushing 10-year German Bund yields back below +0.40% at +0.36% as investors seek safe havens.

Note: There is no government bond supply in the eurozone today but France and Spain will announce the details of their upcoming bond auctions to be held on Sept. 6.

More importantly, Italy’s battered bond market is steady as investors wait for a today’s Fitch Ratings review – there are market concerns that the Italian government’s spending plans will put further strain on already high debt levels.

Note: Fitch Ratings is expected to release its review after markets close. It rates Italy BBB with a stable outlook.

Elsewhere, the yield on 10-year Treasuries has climbed less than +1 bps to +2.86%, while in the U.K, the 10-year Gilt yield has dipped -1 bps to +1.455%.

4. Thus far, dollar steady on month-end

EUR (€1.1673) received some support in late Asia trading as ECB’s Nowotny believed that the central bank should focus on moving the “deposit” rate out of negative territory as he saw “no immediate risks arising due to Italy.” Investors are wary that the single unit could find late afternoon support if Italy’s sovereign rating is not cut by Fitch. Also, providing some support was this morning’s Eurozone “flash” CPI print (see below) remaining above the ECB’s target for the third consecutive month, but it did come in below expectations.

Elsewhere, investor focus remains on EM FX pairs as various central banks take action to address their recent currency weakness.

Brazil’s central bank announced FX intervention – first intervention in two months – Argentina Central Bank (BCRA) raised its LELIQ Rate by +1500 bps to +60.00% for its fifth intra-policy move this year. Indonesia’s Central Bank reiterated its commitment to guard against volatility in FX and bond markets and continue with its duel interventions, while in Turkey, the government revised its withholding tax related TRY deposits which cut the withholding tax on lira deposits while raising tax on FX currency deposits of up to 1year

5. Eurozone inflation eases

Data this morning showed that Eurozone inflation cooled slightly this month, which could suggest that the ECB may remain cautious its approach to dialling back monetary stimulus.

The E.U’s statistics agency said in a preliminary estimate today that consumer prices in the eurozone rose +2% on the year in August, a tad weaker than the +2.1% recorded in July.

Digging deeper, energy prices rose at a slower pace than in July, as did prices for services and industrial goods.

Last month, ECB officials concluded that the Eurozone economy still needed “significant” stimulus from monetary policy to ensure inflation continues to climb and today’s data will likely reinforce that thinking.

Officials in July felt that “monetary policy had to remain patient, prudent and persistent,” the ECB’s minutes said.

Note: In June, the ECB reiterated that it expects to phase out its bond-purchasing program by the end of 2018, although it has signalled that its policy rates will remain unchanged at least through next summer.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019