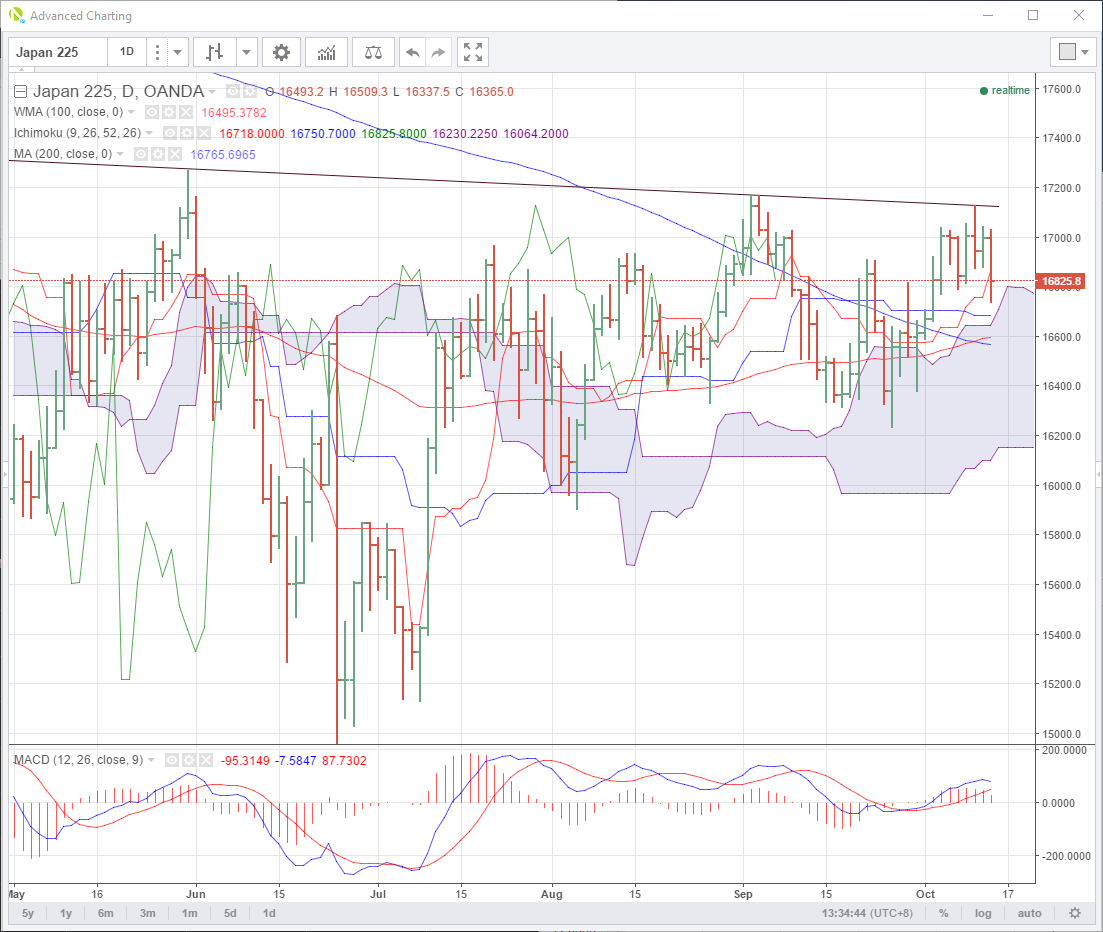

Disappointing trade data from China this morning saw Asia equities marked lower with a knock-on weaker USD in the G10 space.

China’s trade data showed exports falling to their lowest levels in six months this morning. Import growth also missed to the downside, both in USD and CNY terms.

10:00 *(CN) CHINA SEPT TRADE BALANCE (USD): $42.0B (6-month low) V $53.0BE;

Trade Balance (CNY): 278.4B (6-month low) v 364.5Be –

USD/ZAR

Speaking of headline driven currencies. USD/ZAR had another one of those nights. Following on a massive move higher Tuesday driven by the arrest warrant of the Finance Minister, see APAC Corner: GBP Jumps While ZAR Crashes, overnight the prosecutor has said he is prepared to review the entire fiasco. The result has been predictable…

USD/ZAR fell 30 big figures from 14.5000 to 14.2000 before settling mid “range” at 14.3000. USD/ZAR has resistance here at 14.3370 the daily Ichi moko cloud top with support at 14.1200 the bottom of the daily cloud.

Summary

China data surprises continue to move high beta stock indices in the absence of other news. This has a selective knock-on to equally high beta currencies such as the JPY. Other pairs continue to be driven by “headline bombs” keeping traders on their toes.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Jeffrey Halley

Latest posts by Jeffrey Halley (see all)

- Oil slides, gold rally continues - 5 August 2022

- US dollar retreat continues - 5 August 2022

- Pelosi relief rally in Asia - 5 August 2022