Europe is expected to open lower again on Friday as the sell-off in commodity markets continues to take its toll. Weak data from China this week appears to have been the latest trigger as figures appeared to once again confirm that growth in the country is slowing despite numerous rounds of monetary stimulus from the PBOC and of course, the apparent strong GDP readings for the first three quarters.

It’s also worth noting that the market was primed for some form of correction following a good five weeks for investors. Given the light data flow from the U.S. and Europe this week and focus on China, it should hardly be a surprise that this is where the run has come to an end. In fact, we should count our blessings that the sell-off this week hasn’t been more severe.

There was a risk that last week’s U.S. jobs report could have created more instability in emerging markets, given what we saw back in August. The jobs report not only dramatically increased the odds of a December rate hike, based on market pricing, but also of a second in relatively quick succession, possibly as early as August. So far, that doesn’t appear to have spooked investors which would be a big relief for the Fed.

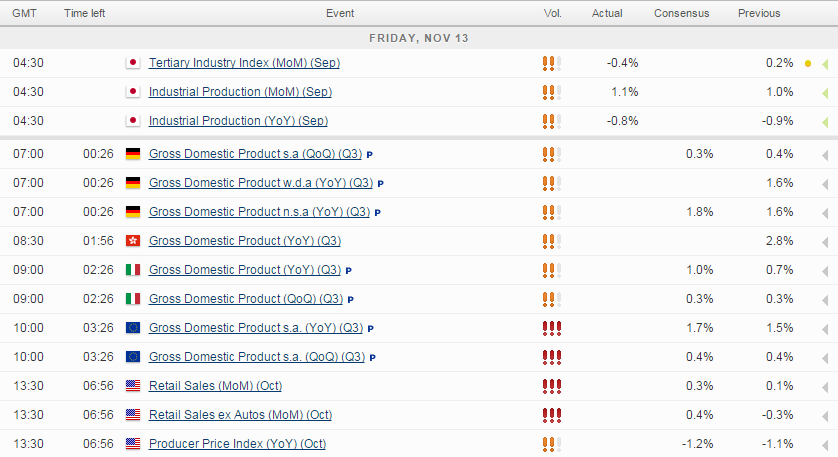

With the jobs hurdle now cleared, the next big test for the Fed will be the October retail sales report. The consumer is extremely important for the U.S. economy and so far this year, it has been quite reserved, despite the boost to disposable income from lower oil prices. As wages pick up, we should expect to see spending pick up as well, the problem being that wage growth has been quite subdued so far. Core retail sales are expected to have risen by 0.4% last month, in line with the jump in average hourly earnings figures that were released last week. While this isn’t great, it is definitely an improvement but we’d need to see more data to support it.

Growth in the eurozone has been very sluggish this year and the latest data for the third quarter is expected to confirm this, with GDP seen rising by only 0.4% again, in line with the previous quarter. Prior to this release we’ll get GDP figures from Germany and France which may offer insight into what we can expect from the overall reading but as with the region as a whole, both are expected to show sluggish growth yet again, at 0.3%.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024