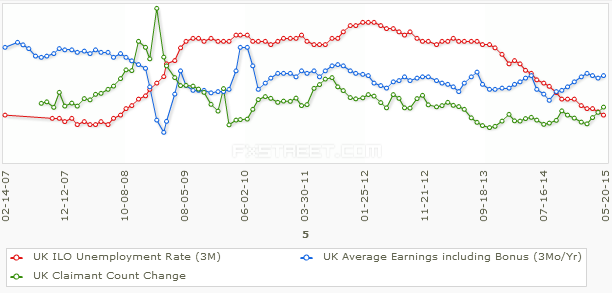

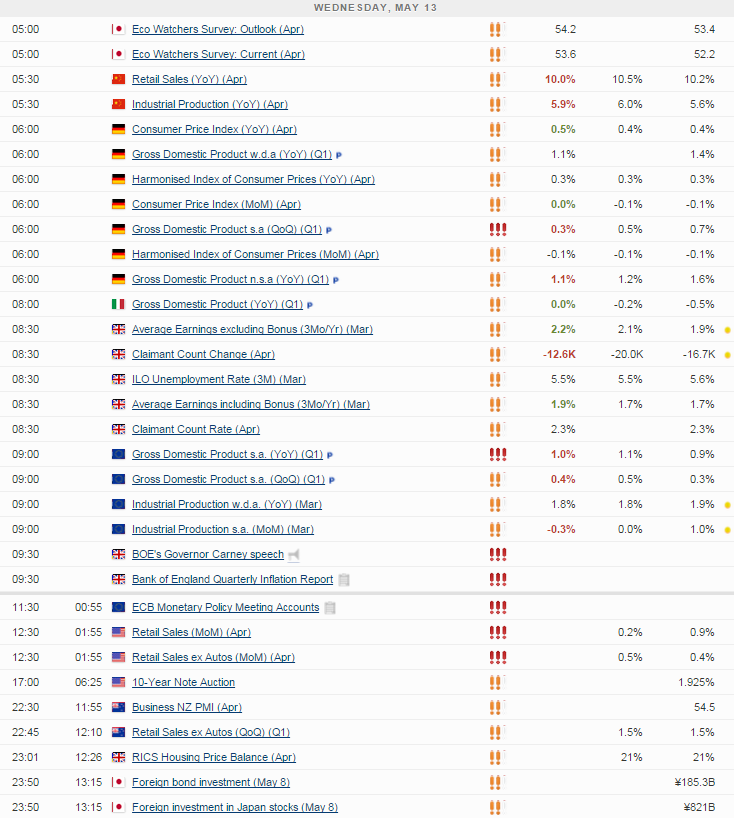

The recovery in the UK labour market is showing no signs of easing up, as unemployment fell to 5.5% in the three months to March. Of course, there remains some underlying problems in the labour market that is to be expected following such an enormous shock to the economy. Productivity remains a problem which isn’t being helped by the rise in the number of self-employed and underemployed. But this will naturally improve as the economic recovery gathers speed, those in part-time employment move into full time permanent work and businesses invest more. This may be helped in the short term by the election result although maybe not as much as it would if the country wasn’t facing a referendum on EU membership in the next couple of years.

Source: OANDA economic calendar

Even with these underlying issues there remains many positive points in the UK labour market. The number of people employed once again rose to a record high in the first quarter of the year. At the same time, average earnings both including and excluding bonus’s improved by more than was expected. This should create more inflationary pressure in the economy and ensure that any dip into deflation, if we see it, will be temporary. At the same time, wage growth is likely to comfortably exceed inflation for some time but are unlikely to grow too fast because of the slack that still remains in the economy. All in all, I think this is a very good jobs report.

Source: OANDA economic calendar

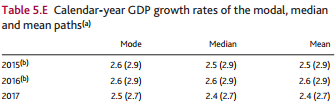

Despite the improvement in the labour market, the Bank of England’s inflation report showed reduced forecasts to growth in the UK through to 2017 while forecasting a first rate increase in the middle of next year.

Source: BoE Inflation Report

This was more dovish than the markets were expecting, prompting heavy selling in the pound which is currently down around one cent against the dollar since the release. The central bank did highlight the stronger pound as a headwind and stressed that it is relevant in its policy horizon which again weighed on the pound during the press conference.

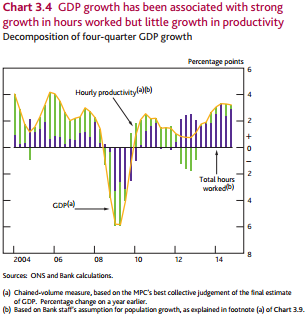

Governor Mark Carney stressed that the new forecasts don’t take into consideration the result of the election and the impact it will have on fiscal plans, which raises great doubts over the reliability of the growth and interest rate forecasts. Especially when the EU referendum – a result of the election outcome – is likely to weigh further on investment in the coming years. One thing that appears clear is that Carney sees productivity as the issue that needs to be overcome before rates can rise and he sees both of these occurring in the next 12 months.

Source: BoE Inflation Report

It’s been a busy start to the European session on a data front, with GDP figures from the eurozone being released throughout the session. The figures were better than expected for France and Italy, but a greater than expected slowdown in Germany weighed on the overall reading for the region. That said, it did grow by 0.4% in the first quarter, when compared to the previous, which is the fastest rate of quarterly growth in four years. This is encouraging when you consider that the economy has ground to a halt in recent years.

The data continues to come as we enter into the US session, with retail sales figures being released ahead of the open. Consumer spending is extremely important to the US economy and therefore these numbers, more so than many others, should give us early signs that the economy bounced back in the second quarter. A 0.9% improvement in spending in March helped make up for much of the decrease in the months before and may impact the month on month improvement we see this month, as we saw in the same period last year. We’re expecting a 0.2% rise in sales, 0.5% in core retail sales, which I think is consistent with the UK recovering strongly in the second quarter, as it did last year.

Crude oil inventories will be another key release today given the moves seen in oil markets for some time now. We have seen a significant rise in oil prices recently as the impact of closing oil rigs starts to impact production and expectations. Today we’re expecting another decline in inventories which could support oil prices again today, although it is worth noting that prices are at the upper end of what many consider to be the new range and therefore unless we see a significant decline in inventories, any rallies may run into heavy resistance.

The S&P is expected to open 7 points higher, the Dow 54 points higher and the Nasdaq 22 points higher.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024