I think it’s safe to say this has been a week to forget in the financial markets as a lack of significant economic data or news flow has left investors to balance the books ahead of the end of the quarter and the start of earnings season.

Investors appear to have played it very safe this week and who can blame them. Poor trading volumes can make markets uncomfortably volatile, which we’ve seen on numerous occasions in recent weeks. We all love volatility but it can reach a point when it becomes too much and when lower volumes are partially responsible, it can make for some difficult market conditions.

The fact that this has come towards the end of the quarter, ahead of an earnings season that investors are less than optimistic about also feeds into this. I think we’ve seen a lot of profit taking this week, some balancing of the books and basically, preparation for the weeks ahead which could be quite rocky if earnings are as weak as is widely anticipated.

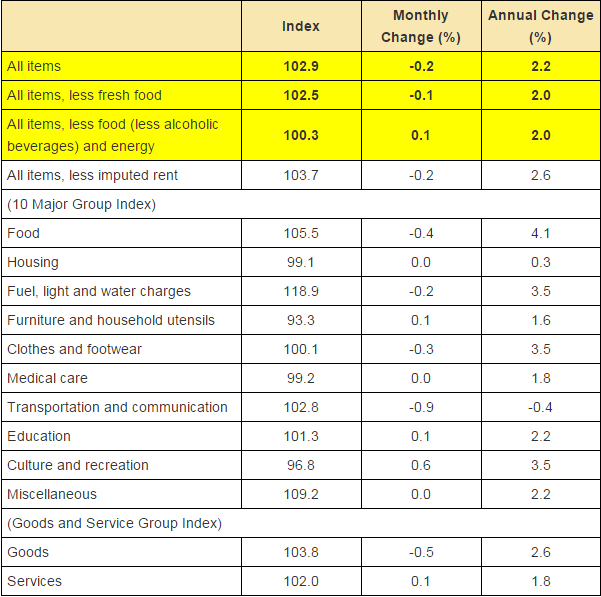

In a market of low sentiment, Japanese inflation data offered little comfort, as the national core CPI fell to 2%. This equates to a 0% rise in inflation compared to last year if you strip out the effects of last April’s sales tax hike. It’s also the seventh consecutive month that this number has fallen which is devastating for the central bank given the amount of cash it is currently pumping into the system in order to hit its 2% target.

*The above table was taken from the Statistics Bureau CPI Report. The full report can be found here.

While I don’t necessarily think this means Abenomics has failed, the central bank and government do have a massive job on their hands now. The sales tax hike has been a complete disaster, more so than even the most pessimistic among us will have expected. Retail sales fell by 1.8% when compared to last year, although it should be noted that we saw unusually large sales ahead of the tax hike which is distorting the figures somewhat. Consumer spending has been disappointing in most months since the hike which must be concerning.

Of course, there are other factors playing into this including the global disinflationary environment we find ourselves in, driven in part by a huge decline in oil prices. With this seen persisting for much of this year, it seems it’s only a matter of time until Japan finds itself back in a deflationary environment with an enormous uphill battle on its hands.

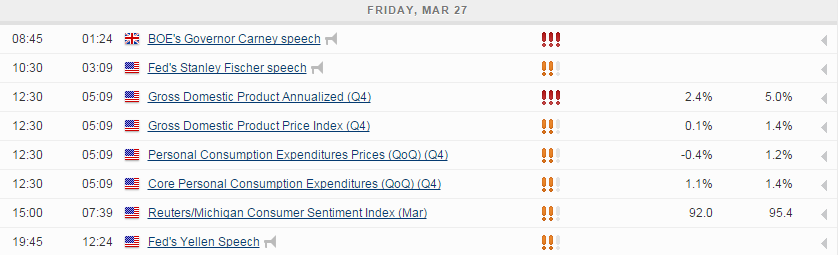

We’ll hear from a few members of the Monetary Policy Committee this morning, including Governor Mark Carney, which could bring about some increased volatility in the pound and UK government debt. Rate hike expectations for the UK seem to change by the week and therefore any clarification from policy makers on this will be welcomed by the markets. As it stands, I think last this year is the most likely timing of the first rate hike but forecasts do vary massively and go as far out as 2017, with some pointing to the low inflation environment as being a far bigger threat than Carney is suggesting.

Later on we’ll get the final fourth quarter GDP reading from the US, which is expected to rise to 2.4% from 2.2% previously, followed by the revised Universite of Michigan consumer sentiment reading for March. Federal Reserve Chair Janet Yellen will wrap things up for the week as she speaks at the Federal Reserve Bank Conference. I don’t expect anything new from Yellen but there is always a heightened risk of extreme volatility when she speaks.

The FTSE is expected to open 11 points higher, the CAC 10 points higher and the DAX 36 points higher.

For a look at all of today’s economic events, check out our economic calendar. www.marketpulse.com/economic-events/

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024