The recent weakness in USD helped pushed USD/INR lower. But it should be noted that INR has been strengthening steadily against the Greenback even before the NFP disappointment. Furthermore, USD didn’t really weakened that significantly, 0.0385% weaker than the basket of 7 other major currencies since the start of this year. And that is after taking into account the post NFP weakness which drove USD weaker by 0.855% D/D. Hence, we can safely say that the steady decline in USD/INR is attributed more to INR’s strength since the beginning of Jan.

This increase in strength can be attributed to the gains in Sensex last week, which attracted inflow of foreign funds into India and drove INR higher. However, it should be noted that Sensex was actually bearish from 2nd Jan all the way through 7th Jan, but INR did not weaken much more beyond the initial USD/INR rally which sent prices from 61.7 – between 62.1 – 62.4, underlining the inherent strength of INR that is in play currently. Latest easing of rules by Central Bank RBI with regards to Foreign Direct Investments (FDI) also helped both Sensex and INR, and it is no surprise that Sensex started recovering after the relaxation of FDI rules which gave investors option to exit their investments by selling their holdings of equity or debt given some conditions. This is a welcomed move as it instilled greater confidence in investors that they’ll be able to exit their India exposures if things do not go well – allowing investors to take higher market risk as the liquidity risk is now lower.

Instead of restricting outflow of funds which is the obvious thing to do, RBI has actually made it easier for foreigners to exit their funds – thus instilling a sense of security and traders end up feeling much more assured. Besides providing other Emerging Economy countries the textbook response on how to address leaky foreign funds, this also increases market confidence that RBI will be able to resolve the ultimate issue – high inflation and low economic growth. Even if there isn’t any concrete plan revealed by Governor Rajan on how RBI will address this, Rajan is building up goodwill which will buy him some more time. As it is, market seems to be rather forgiving towards last month’s rate decision surprise where RBI has chosen to hold rates. With this additional goodwill, it is possible that USD/INR will remain stable even if RBI hold rates this month, and the likelihood of INR rallying strongly should a rate hike occur is high.

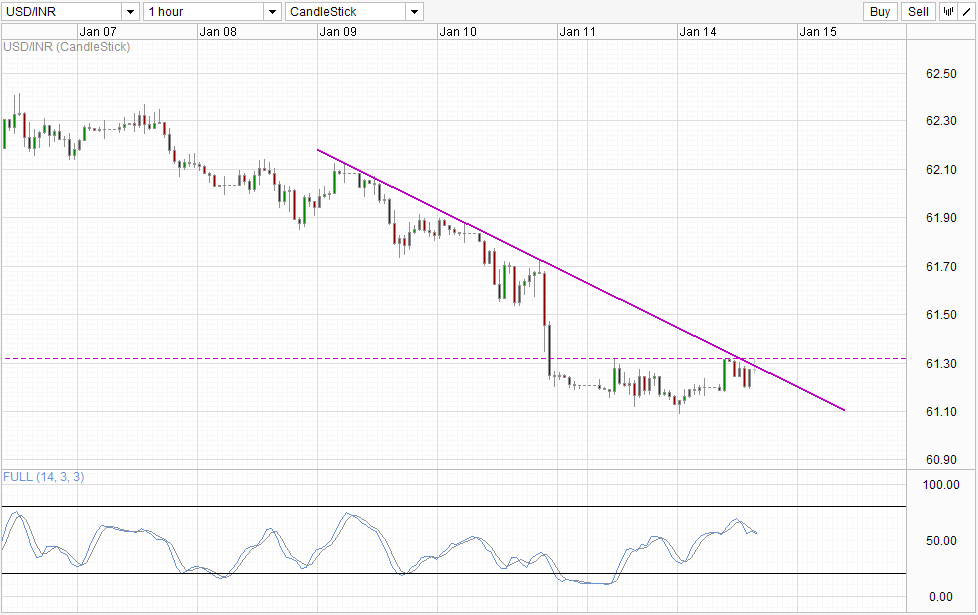

Hourly Chart

From a pure technical perspective, prices have rebounded off the 61.3 resistance (seen on Weekly Chart as well) and is being eased lower by the descending trendline. Stochastic readings appear to have topped as well, agreeing with a bearish scenario where a retest of 61.1 is possible leading to further bearish extension.

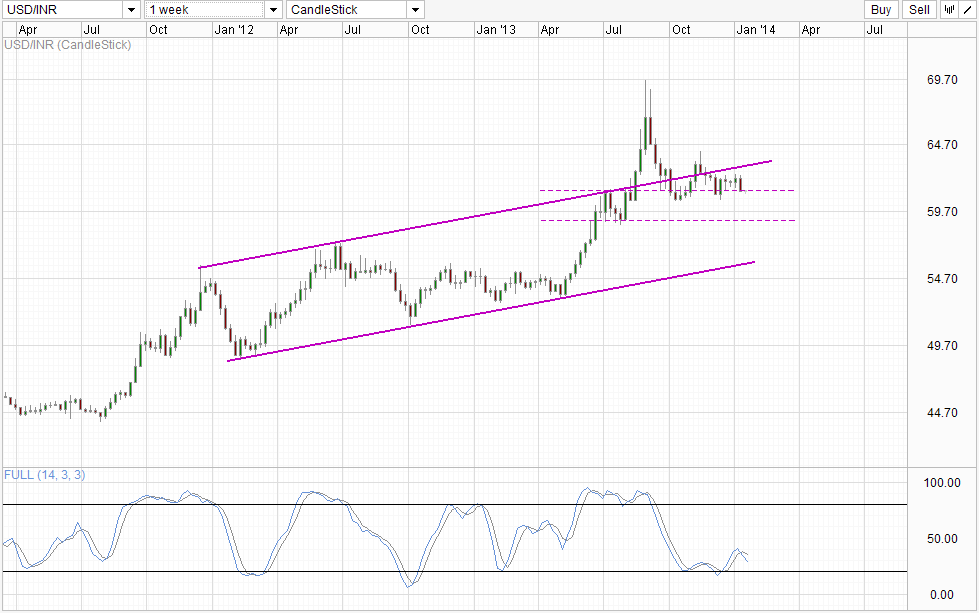

Weekly Chart

Should the breach of 61.3 is confirmed, a push towards the consolidation zone’s floor around 59.0 becomes the clear bearish objective. Beyond 59.0 becomes a little bit harder as Stochastic readings should be deeply within Oversold region when that happens. Furthermore, a long-term bearish outlook for USD/INR does not really fit fundamentals that favors continued strengthening of USD in 2014 and 2015 due to the tapering of Fed’s stimulus. Besides the obvious impact on USD, QE tapering will also increase Treasury yields, which will gravely reduce interest in carry trade. As such, RBI’s rate hike for Rupee will become less and less impactful in the future as long-term carry investors will require much higher carry premium in order to compensate their market and FX exchange risks for holding USD/INR. Hence, long-term uptrend for USD/INR is likely to remain intact in the long run, and even if 61.0 is broken, it is likely that Channel Bottom will hold.

More Links:

EUR/USD – Resistance Level at 1.38 still Looms Large

AUD/USD – Moves to One Month High above 0.9080

NZD/USD Technicals – Seeking 0.84 Consolidation Top

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014