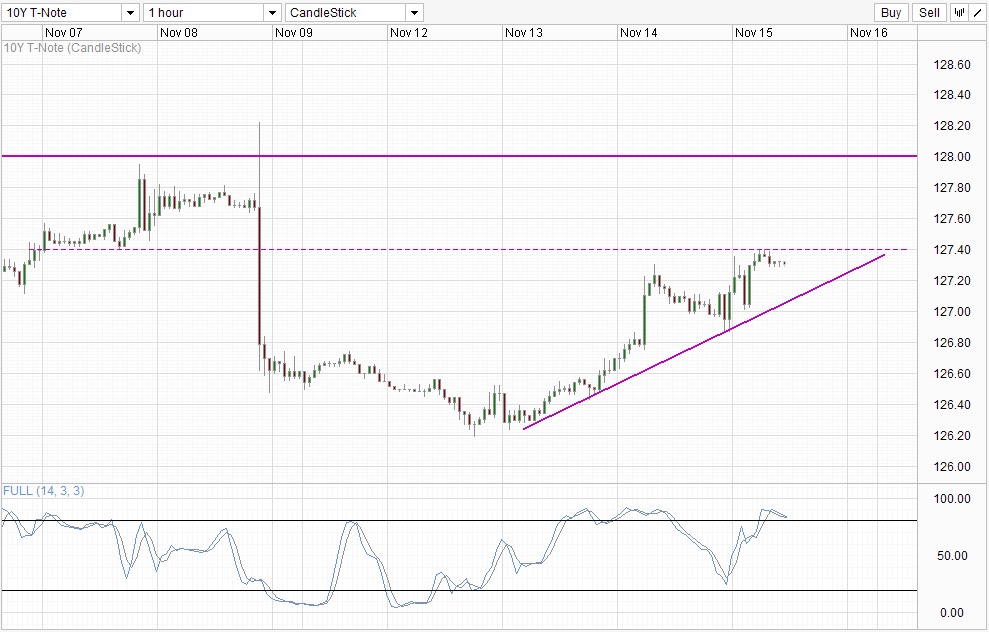

Treasury prices grew this week on speculators hoping that the Fed will not be tapering QE anytime soon (read: December), and what Fed Chairperson Nominee Janet Yellen said in the past 2 days fueled this speculation further, pushing US10Y prices to a high of 127.40 during early Asian hours today.

It is interesting to see market reacting so heavily on Yellen’s comments, as Yellen was always a known dove and some regarded her a tad more dovish than Ben Bernanke himself. Furthermore, Yellen will not be able to change the opinions of the other Fed members that have indicated their preference for some sort of tapering action soon, and she only has 1 vote just like everybody else. It should be noted that chances are Bernanke does not want to taper QE in any magnitude during his term, but was forced to mention about potential taper scenario back in May because he feared that the majority of the FOMC members would want a tapering action soon. Simply put, Yellen statements does not change anything, and even if her latest statements suggest that we are no longer moving towards a Dec Taper, the same fears and concerns will come back in early 2014 once again.

Hourly Chart

Therefore, current bullish response seems a bit unreasonable, and there is a risk of strong bearish pullback. The same charge applies to stock prices as well, which are currently at record highs, but 10Y prices seem to be a tad more reasonable compared to equities right now – the gains yesterday/this morning are not as high compared to Wednesday’s when Yellen’s prepared statements were released – statements which were much more dovish compared to the comments she made during yesterday’s Q&A where she mentioned that QE 3 cannot last forever. Hence at the very least fixed income traders are reacting “more correctly” than their equities counterpart, suggesting that downside risks on 10Y prices may come in earlier than stocks (this fits the age-old perception that bond prices tend to reflect trend reversals better than other financial assets).

This hypothesis is also be reflect by technicals, with prices facing the 127.4 resistance with Stochastic readings pointing lower, looking likely to form a bearish cycle signal soon. Should prices break the rising trendline coupled with stoch curve pushing below 80.0 by end of today, coupled with a bearish Monday, a longer-termed bearish push will be in play, with 126.2 as short-term bearish target.

Weekly Chart

Similarly, long term chart remains bearish despite this week’s rally. Prices remain below 128.0 and more importantly below the rising trendline that represents the previous bullish correction that was in play. A new bearish cycle signal has been formed on Stochastic, favoring a move back towards 124.0 and beyond.

This fits well in the long-term fundamental outlook where yields will be expected to increase in the long run – pulling out of QE plug will naturally send rates higher (price lower) due to the decrease of artificial demand. Alternatively, assuming that QE continues forever, market will start to lose confidence in Fed’s ability to turn things around which will result in market demand for Treasuries (perhaps turning to Chinese bonds?) However, it is important that momentum swings back to bears’ favor before traders start to short aggressively. Patience is of utmost importance here as sentiment may take days or weeks to change.

More Links:

GBP/USD – Pound Keeps Rolling, Shrugs off Weak Retail Sales

USD/CAD – Pushes Above 1.05 on Weak Unemployment Claims

AUD/USD – Lower on Weak Aussie Data

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014