Dealers want volatility, investors like volatility and we have volatility across the pond, in sterling. The first trading session after non-farm payrolls historically tends to be the quietest of the month. Yesterday, did not disappoint as the dollar gave back some of its over exuberant climb in an orderly fashion. The same cannot be said for cable this morning. Before the release of UK industrial and manufacturing data, the pound was happily trading on the front foot. Post data release, sterling support has fled to higher ground with cable initially falling three-quarter of a cent outright and half-a-cent against the 17-member unit.

The UK’s industrial sector performed poorly last year, and the recovery this year is admittingly proving to be a slow process. A competitive and buoyant UK manufacturing and export sector is an integral part of Prime Minister Cameron’s big plan to shift the economy away from consumer spending and the financial service sector. The latest trade deficit numbers were little changed, a little wider at -£8.5b in May from April’s -£8.4b print. Despite the deficit increasing, oil exports continue to offer a bright spot, growing +27.7% on the month in May. This happens to be the largest increase in a dozen years. Despite the marginally larger pickup in imports over exports on the month, analysts believe the overall trend is improving.

UK industrial growth grounded to a halt in May, and this despite a sharp pick up in oil and gas extraction (+4.9%). The trade deficit was little changed from April, further emphasizing the slow pace of the UK recovery. Industrial production was unchanged month-over-month, but was down -2.3% from a year earlier. Analysts note that with the broader calculation for output, manufacturing fell -0.8% in May and was down -2.9%, y/y. The market had expected IP to rise +0.1% on the month and fall -1.4% on the year, while manufacturing was forecasted to rise +0.3% in May and drop -1.6% on the year.

EUR/GBP has risen half-a-penny to a four-month high following the UK’s industrial and manufacturing disclosure. The move has opened the way for the bulls to again contemplate testing the March 12 lows north of 0.8719. For Cable, despite falling a cent so far this morning, bids are located ahead of 1.4850 and 1.4800 option barrier territory. This area also happens to be in proximity of the four-month low last visited ahead of Friday’s NFP release.

The market has also been taking its cues from overnight Chinese inflation data. In recent months, disappointing economic figures from the globe’s second largest economy, most notably the HSBC’s manufacturing index, has lowered market expectations for the country’s Q2 growth numbers. The inflation data did not disappoint, it provided some relief to the Asian markets in particular – investors were getting use to some disappointing data of late.

China’s consumer price index rose +2.7%, y/y, in June from the median estimates of +2.5% and previous reading of +2.1% in May. It is not surprising that the headline print was driven by food inflation (+4.9%, y/y, from +3.2% in May), while non-food inflation was unchanged (+1.6%, y/y). This evening, China will release monthly trade data and the market is anticipating the trade surplus to have widened in June to $27.75b.

Positive developments concerning Portugal and Greece yesterday has helped to support EUR sentiment for a second consecutive session. Continued signs of political stability in the Iberian peninsula, along with ECB’s Draghi’s assurance that they policies will remain accommodative for the foreseeable future, has gone some ways to reassure investors.

The overnight Euro session opened up with a few speculators deciding to pare back on some of their short positions taken after last week’s ECB meeting and NFP print. The buying was fuelled by the disappointment in the EUR fall. There is market talk of decent supply of the single currency on offer at 1.2900, hence a rejection first time around this morning. From an option perspective, large expiries close to the aforementioned levels will provide further supply of the single currency for now. On the downside, and a bit of a distance away, stop losses are again beginning to accumulate just south of another option related handle at 1.2850.

Other Links:

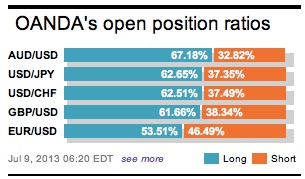

Everything Bar The Price Suggests EUR Head South

Dean Popplewell, Director of Currency Analysis and Research @ OANDA MarketPulseFX

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019