Investor’s primary objective is to get through tomorrow-in one piece. Another Fed policy will have come and gone, with ‘helicopter’ Ben again having the opportunity to leave a different legacy ‘footprint’ in his press conference tomorrow. The small percentages of remaining ‘weak’ short EUR positions are being tested this morning. Despite many speculators having already decided to wade to the asset class sidelines, few remain in the single currency stop loss crosshairs. So far this morning, the talk of stronger data has been accompanying the 17-member single currency’s rise, perhaps a speculators ruse to trigger some stop losses? The remaining pre-FOMC unwinding would most likely be the paring of longs EUR’s – a far cry from the recent record long dollar position.

The major currency pair’s price action has tried to remain mostly range bound ahead of tomorrow’s FOMC announcement. Despite some of the to-fro action around European fundamental releases earlier morning, this market will take the first opportunity to sit the remaining sessions out until things are made much clearer to them. The Financial Times is already reporting that the Fed will taper sooner, though not on any new fresh insights or tips from Fed officials. This is a tricky meet for the Fed. All its communication skills will be put to the test and they had better be sharp, any miscommunication and the asset bleeding will return with a vengeance.

Investors will be looking for any changes in the regular statement and forecasts from the Fed’s policy makers. Despite having already done some significant pre-meeting asset price damage and rebalancing last week, the market hemorrhaging only stopped after a few Fed watch reports. They suggested that any bond tapering would be gradual in nature, and that rates would remain “low” for a considerable period of time. It was more about who delivered the message rather than the message itself that had market impact – Hilsenrath’s piece (the Fed’s friend) at the WSJ. All investors are looking for is greater clarity on US monetary policy before they ‘ply their wares’ again.

This morning’s German ZEW sentiment beat expectations this month, printing 38.5 versus a consensus of 38.1. Digging deeper, the current conditions component undershot, coming in below expectations and also the previous reading of 8.9. The improved headline reading comes despite a weakening in global bourses – one would have expected the opposite result. Today’s print is well short of this year’s German high mark produced in March (48.5) and the post crisis high of four-years ago (57.7). However, the survey still suggests that the German economy is to pick up speed in H2. By day’s end this indicator is not always a reliable predictor for German GDP.

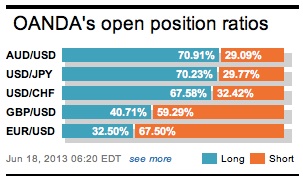

On-forecast data is the last thing that a true speculator wants to hear. With this morning’s German ZEW release behind us, speculators may now try and curb market risk and lead the single currency lower. The speculators have been long EUR’s, a reverse of positions driving recent moves, mostly accumulated in earlier morning action. The market’s natural inclination is to expect FOMC event risk to now curtail market activity and this could lead to further single currency profit taking as the 1.34 barriers have survived. Failing to knock out the barriers leaves some speculators longer heading into the Fed rate decision tomorrow. The record dollar longs of late have been hugely pared – a tad ironic as we head into the event that has every chance of being more “hawkish.”

UK inflation accelerated last month, certainly not something that the new BoE governor Carney will really want to hear. Economists’ are worried that any squeeze on consumer incomes now could potential derail the UK’s fledgling recovery. Consumer prices rose at an annual rate of +2.7% in May versus +2.4% in April. The usual culprits are to blame; May’s pickup was driven mostly by energy prices and airfares. The data confirms that inflation continues to outpace wage increases, a scenario, if continued, will only impede UK consumer spending and the possibility of growth for the economy.

The BoE has been preaching, despite their consumer inflation target of +2%, are on record stating that UK inflation was to accelerate further this year before gradually slowing down to target in 2015. Sterling, after it’s knee jerk inflation boost, met fresh headwinds at its four-month high above 1.57. The market continues to tangle with the 200-DMA at 1.5697; a series of closes above here will point to a structural shift to the upside. Today’s report is another blow for the BoE dove. The market will now be focused on tomorrows MPC minutes and King’s speech.

Other Links:

Squeezed To Square: A False EUR Bid Into FOMC?

Dean Popplewell, Director of Currency Analysis and Research @ OANDA MarketPulseFX

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019