Is the demand for oil increasing or decreasing? Last week both Department of Energy and American Petroleum Institute reports hinted at increasing demand with lower inventories, allowing Crude Oil bulls to transform its then bullish correction to a full blown bullish reversal above 89.0. Yesterday,the DOE Crude Oil inventories indicated that inventories has grown by 6.7 million barrels in the week ending 26th April. This puts crude oil inventories at record highs, suggesting that the previous surge in demand was not a structural shift but merely volatility spikes.

But is it?

Gasoline inventories have been steadily declining. The latest report showed that recent decline was at 1.8 million barrels, twice that of analysts estimate of 900,000 barrels. This suggest that energy consumption remain high, and this in theory should result in stronger demand of crude that we are not seeing right now. So what is actually going wrong?

Perhaps we are looking at the situation incorrectly. Demand of crude oil rides heavily on demand on its refined products, crude oil itself isn’t really useful to the rest of the world. The usual understanding is that higher usage of Gasoline (and other distillate products) will result in higher demand for Crude oil as refineries will want to convert more distillate products to sell more while they still can. However there is a huge assumption in this relationship – refineries do not have enough stockpile to keep up with the increase in demand.

Looking at historical data, even though gasoline inventories are dropping, current levels of Gasoline remain higher than the historical average (since 1990). This suggest that refineries believe they are able to meet current demand and perhaps more. The fact that rate of decline is higher than expected paints a chilling tale – refineries want to bring down their overall stockpiles because they believe overall demand will decline in the near future, and hence are not interested to replenish their stockpile and prefer to feed extra demand (if any) from their reserves.

This spells bad news for Crude bulls, as price may continue to be depressed until refineries are comfortable to produce more again. Production of Crude in US has increased by 20% Y/Y, and that will certainly not help the prices of crude in 2013.

Hourly Chart

From a Technical perspective, price was already pulling back after the rising trendline was unable to propel price higher. Price manage to break the previous swing low of last Friday even before the disappointing ISM Manufacturing data. The subsequent Crude Oil inventory numbers only served to entrench price below the support of 25th April. The pullback from the recent lows has failed to bring price back above 91.0, allowing current bearish pressure to be still in play.

Daily Chart

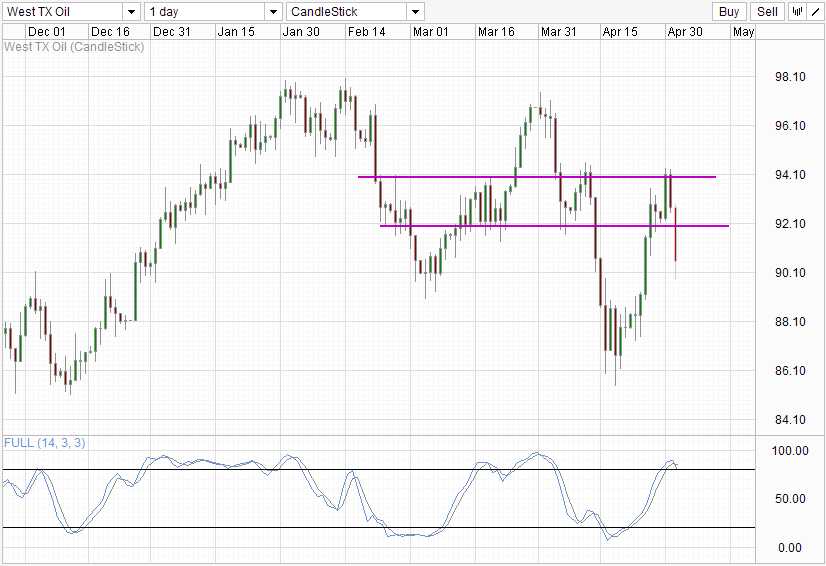

Things are equally bearish on the daily chart. Even though price managed to bounce off 90.0, it seems possible that a retest of the interim support may occur again with Stoch readings peaking and heading lower now. The quick manner which the 92.0 – 94.0 right handle has been broken is also equally disconcerting, suggesting that the underlying bears are still strong despite the incredible rally we’ve seen from 86 – 94. Should 90.0 gets broken, 86.0 may be reopened as plausible bearish objective but preferably price should break 89.0 as well in order for bearish acceleration to occur.

Moving forward, it seems that the weekly DOE inventory report may not be a good representation of actual primary demand of energy consumption, perhaps we may need to wait till inventory levels fall back to historical averages before the report can be interpreted with reliability. This would also mean that the report may swing wildly from over to under expectation w/w and that would mean higher volatility in Crude prices moving forward.

More Links:

AUD/USD – Falls Sharply Back Under 1.03

EUR/USD – Reaches Highest Level in Two Months Above 1.32

GBP/USD – Moves Higher Again to Above 1.56

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014