After last week’s RBNZ’s dovish statement that sent NZD/USD below 0.82, price has recovered significantly, with Friday close narrowing missing the weekly high on Mar 12th. This is a strong bullish showing, and suggest that momentum may continue early next week.

Then Cyprus happened.

The Cyprus bailout package turns out to be less of a blessing and more of a curse. Risk correlated assets tank heavily on Monday morning, and NZD/USD was not sparred. However, due to the strong inherent bullishness, price managed to rally off early lows and reached Friday closing levels briefly, before bearishness took off again, pushing price lower. The reason for the decline is not immediately clear, as news wires pertaining to New Zealand were silent, but looking at other risk currencies and stock indices, it is clear that risk aversion plays a huge part in keeping price depressed.

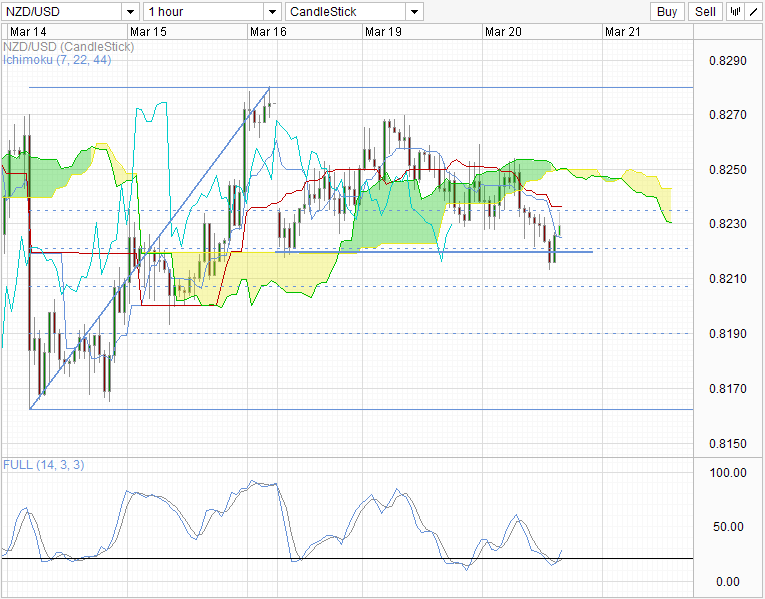

Hourly Chart

Today’s worse than expected Current Account pushed Kiwi lower, reducing earlier gains earned after voting results showing zero support for the levies from Cypriot Parliament. Current Account balance came in at -3.255B NZD, showing a larger deficit than expected. Deficit to GDP ratio has increased to 5%, from previous 4.7% and higher than analysts forecast of 4.9%. The news tended not to invoke strong directional follow-through, but given the current bearish context, it is not surprising to see price pushing lower, trading below Monday’s low at one point.

Nonetheless, bulls still remain robust in the short-term as current support around 0.822 remains. Not only is this level just around Monday’s low, it is also the confluence of Kumo support, and the 50% Fib retracement of the rally post RBNZ lows. Stochastic readings are showing lower and lower peaks, but current readings appears to be heading upwards and that will provide some short-term support on top of the various support trendlines. However, this does not mean that price is bullish. Resistance in the form of the overarching Kumo remains. Also, 38.2% Fib retracement which is also the confluence with Monday’s structural support may still provide resistance against short-term upside.

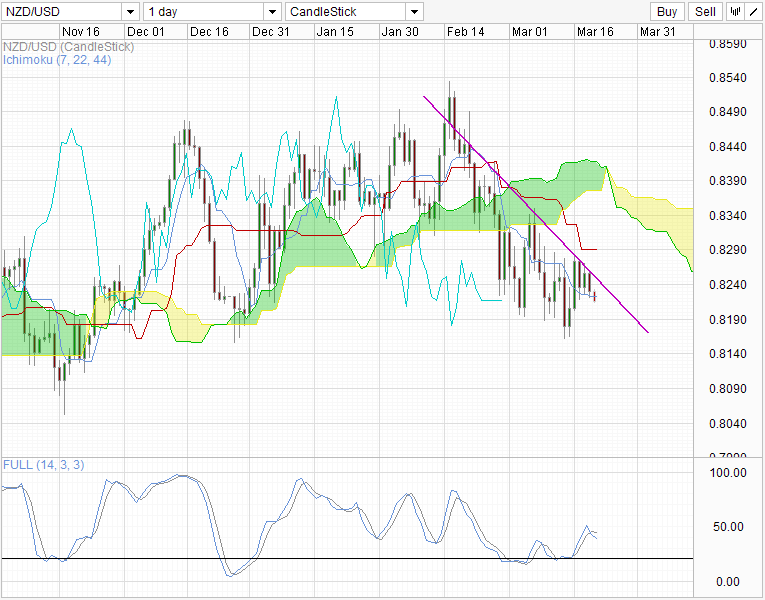

Daily Chart

Daily chart is still bearish, as price is still trending below the descending trendline. Stochastic readings suggest that price may be entering a short bear cycle with an interim peak. However, support can still be found around 0.820 which is near the support found back late Dec. It is also highly likely that Stoch readings may reach Oversold regions when price hit such levels.

Fundamentally, a prolonged Cyprus impasse will help in fueling the bears as fear strengthens USD. However, there might be short-term bullish surprise. Cyprus Finance Minister Michael Sarris has indicated that the is “hopeful” ahead of his trip to Russia, with market watchers anticipating that a deal may be in place as an alternative to ECB’s bailout funds. Also, stance of EU appears to have softened with Austrian FinMin Fekter saying that they are waiting for new proposal from Cyprus. This has eroded the certainty of Levies on deposits and market will have something to cheer about (at least in the short-term) as the hunt for a better solution begins.

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014