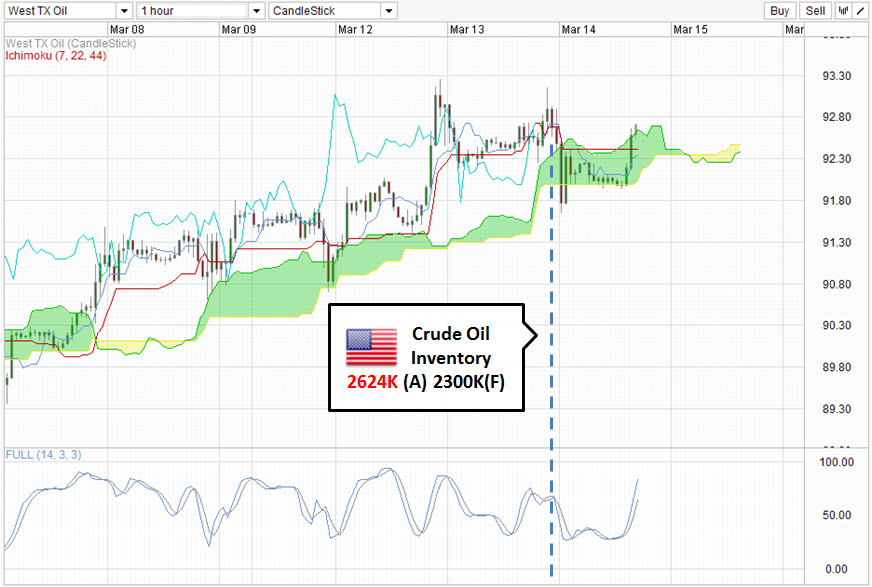

Some say the mark of a person’s character is not in how he react during success, but how he pick himself up after a fall. If that is true, then it seems that Crude Oil is made up of firmer steel then we thought. Prices traded lower after the US Department of Energy released the outstanding Crude Oil inventories at 2625K barrels in the week of 8th Mar, much higher than expectations of 2300K. Prices saw some significant follow through on the downside as US Business Inventory also showed higher than expected growth as well – indication that demand for stock is lower. Nonetheless, bulls recovered quickly and simply dusted themselves off, showing their underlying resilience which will certainly be useful for price to hit higher highs once more.

Hourly Chart

Price was threatening to breakout from the Kumo but was rebuffed immediately after closing under the Kumo. Price traded into the Kumo directly, with the Senkou Span B (Kumo bottom) providing good support during Asian hours today. Currently, price is threatening to breakout of Kumo on the upside, to regain bullish momentum once again. Even though the forward Kumo is bearish, it is interesting to see Senkou Span B rising, diminishing the bearish bias and suggesting that a bullish Kumo Twist may happen down the road soon.

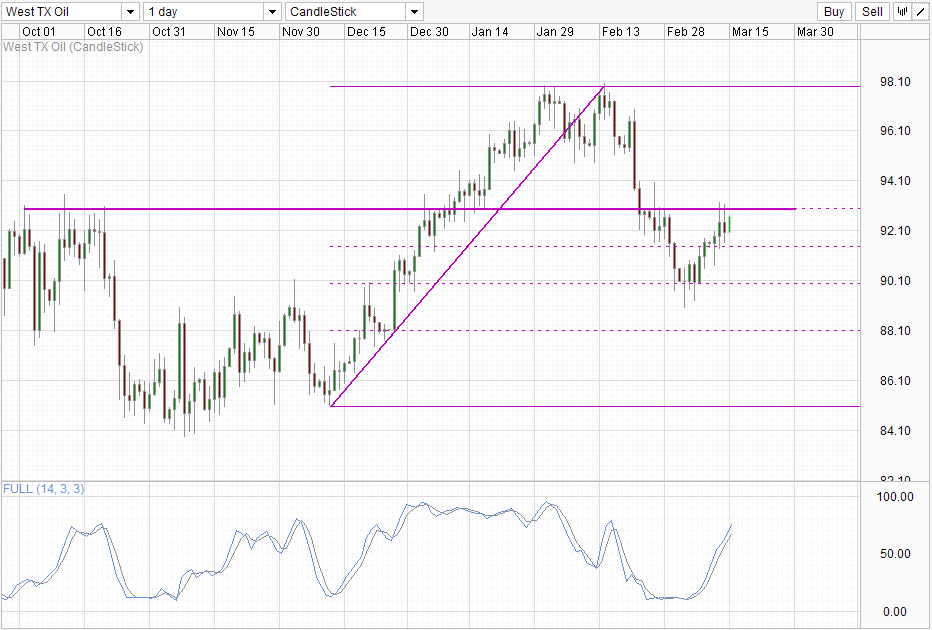

Daily Chart

Daily Chart is moderately bullish. If price is able to clear the 38.2% Fib retracement which is also the confluence around the peak of late Feb consolidation channel, bulls may treat it as a confirmation that the pullback from Feb High is over. Stoch readings suggest caution though, with readings approaching Overbought region just as price is approaching the significant resistance.

It is also pertinent to point out that WTI Oil is much better supported as compared to Brent Crude. Brent-WTI spread has narrowed significantly, pushing Brent’s premium to less than $17 USD a barrel at one point during Asian trade. This suggest that the rise in WTI is not really due to increase global demand, but instead due to the starting of the Longhorn pipeline system – which will deliver 75,000 barrels of oil from Texas in mid March. This dramatically reduce the cost of delivery for WTI and attract more traders to purchase WTI. What this means is that we could potentially see the impact of the enhanced delivery system normalize, and may result in WTI following the trend of Brent in the future if global trend of oil has not recovered by then.

More Links:

Gold Technicals – Bears still at play but Bulls lurking

NZD/USD – RBNZ wants lower NZD

AUD/USD – Tremendous Employment Data send Aussie Soaring

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014