Is there a strong ‘silent’ currency war in play? If so, the real investor needs to be officially invited so they can avoid betting against Central Banks this year. Looking at the yen, it remains one of the surest bets!

Yesterday, the dollar managed to record its largest one-day rise against the currency from the ‘rising sun’ in 13-months. The yen weakness was again mostly fuelled by stoic comments from the Japanese Vice-Finance minister Nakao, who indicated that ‘appropriate action’ would be taken if the currency resumed its strong trend after this weeks Bank of Japan announcement.

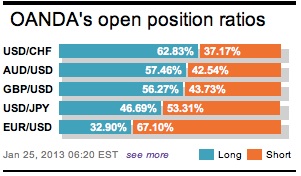

On the street, the word is that hedge funds have been well positioned to profit from the yen’s decline, while real-money investors have mostly missed out on this -15% move outright and -25% against the EUR. The real-investors seem to have been too hung up on the EUR and its periphery concerns. The fact that the yen crosses remain under pressure, despite the BoJ falling somewhat short of expectations earlier this week, is strong proof that the Central Bank really does like yen at 100.

Despite watching German business confidence climbing to a seven-month high this month (Ifo survey-104.2), lenders remain the main focus, as the ECB is about to reveal early details of how much banks are willing to pay back in their long-term refinancing operation loans (LTRO). The data will provide an indicator of liquidity requirements within the European banking sector. It should also deliver enough information to understand how quickly the ECB balance sheet will shrink; a strong directional driver for the single unit. A healthy repayment schedule would be EUR supportive.

However, it will not be just the size of repayment that matters. If banks that pay the loans are required to sell peripheral bonds that were been held as collateral at the ECB, then peripheral bond spreads would widen, most likely sending the EUR lower. If banks were capable of holding onto this collateral, it may force-short term rates to back up, supporting the EUR. Market estimates around +EUR100b of repayments, with the bulk of the repayment schedule coming from the stronger economies.

Does today’s German data release prove that the contraction, in the backbone of Europe’s economy, is over? The better than expected release (104.2 vs. 103.1) suggests that the German economy will return to growth in spring after a weak Q4. 2012. For the EUR bears, this data contrasts with the ongoing weakness the other euro-zone countries. Markit released data yesterday indicated that business activity plunged in France.

In the UK, the early rumored leak of +0.2% proved to be false with Britain’s Q4 GDP coming in much weaker at -0.3% compared to market expectations of a -0.1% print. The “Old Lady” has been somewhat prepared, anticipating a -0.2% read. This release should not have a huge impact on the BoE or on its current outlook. However, the rest of us can perhaps start worrying about a threat of a triple-dip recession and UK rating shenanigans?

It’s probably not a bad bet to believe that the BoE will remain on hold until King has departed in early summer. The new ‘wonder’ banker Carney may have to look at expanding BoE QE program immediately, say an extra +GBP50b? Sterling, so far today has managed to break to fresh new lows against the majors.

Stateside today, December new home sales closes out this week in data, and a few expect the release to surprise strong at +395k, up from +377k, with consensus at +385k.

Yen and the EUR remain the order of play. The single currency has managed to already print a 10-month high this morning. The EUR’s rally has firmly extended through 1.34 and is eyeing this week’s long-term spot target, 1.3490-00.

The techie’s continue to talk up the currency’s bullish momentum by indicating that the daily charts show scope for further upward action. The market’s has really got to take a peek at 1.35, and see what just behind that. It’s a smart move to move one’s stop below Wednesday’s low (1.3263) to reduce risk.

Other Links:

Is the Euro Market Now Sitting On The Fence?

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019