Where has all that volatility gone? Volume, depth and market interest cannot have already peaked? After an encouraging start to the New Year for forex investors, currency market seems again to have settled into a narrow range. That is even the same for the most dominant of trades, being short yen against anything else. For 24-hours we saw yen get the upper hand as the market punished and profited from the BoJ, who may or may not have been dovish enough for investors liking. It was all in the timing-2014 was perceived being a tad too far away for Asset Purchase changes!

However since then, USD/JPY has neatly pushed itself deep, well above 89, boosted by comments from deputy economy minister Nishimura that the yen at 100 is no problem for Japan. The EUR on the other hand continues to trade sideways, now that after the US House of Representatives voted to suspend the debt ceiling until May, has allowed some of this market volatility to recede. Two trains of thought have the single currency going in opposite directions. Some see the currency rising to +EUR1.38 on encouraging news from the EU (periphery spreads narrowing for instance), while a percentage of investors have a growth case argument for the EUR to be weighed down by the regions weak growth. The rest of us are sitting on that picket white fence!

Other asset classes ‘to and fro’ action is again influencing the participation rate for forex. Global bourses have nudged a little higher so far this morning, as investors weigh up yesterdays disappointing Apple data (a statement we thought we would never have to utter) against early signs of an improvement in the Euro-zone business activity. A company whose products of many “i’s” reported mostly flat year-on-year earnings and a Q2 guidance falling short of market expectation had Asian regional index ending in the red. To be fair, Apple is far reaching, but not that globally influencing. Early session equity gains following the better than expected China’s flash manufacturing PMI were wiped out after North Korea threatened to conduct a nuclear test in response to UN sanctions. Scare mongering tactics tend to have a bigger impact than an iPad!

Digging deeper, China’s HSBC flash PMI rose to a two year high of 51.9 in January from 51.5 in December, a fifth consecutive monthly improvement. The new orders index fell marginally to 52.7 from 52.9, but new export orders rose 0.9 to 50.1. This certainly gave the Aussies and the Kiwi’s a boost, as China is their largest trading partner. Most analysts are probably crying a sign of relief that the great ‘Red Machines’ economy continues to gather momentum. Many continue to look for that global savior, however, early indicators from the region that many have backed, show strong proof that they could be on to a winner. All the signs look good for the new Chinese administration that begins work next month.

Heading to Europe and with the aid of encouraging data, indexes are seeing black and dragging the ‘single unit’ along with it so far. Initially the EUR threatened to revisit some of yesterdays outright lows after dismal French business activity figures for last month (42.9 and 43.6 manufacturing and services PMI), but quickly re-energized to trade a session high as the same data from Germany, the backbone of Europe, showed strong activity (48.8 and 55.3 manufacturing and services PMI). Evening things up was the Euro composite PMI for January beating expectations (47.5 and 48.3 manufacturing and services). One can conclude that this data, once added to the improving financial market conditions we have seen over the past few weeks (tighter periphery spreads), is beginning to have a positive effect on the Euro economy. This is certainly a feather for the EUR bulls hat, however, little things like Spanish unemployment creeping up to +26% this morning looks good for the underachieving EUR camp. The remainder of us will be painting those picket fences!

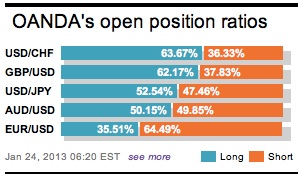

Stateside today, US Jobless claims will be the main event on most traders’ calendar. Early expectations from a few, anticipate deterioration from +335k to +370k, while consensus is looking at a much smaller correction, to +355k. For the Markit flash PMI, easing a tick to 53 for this month will not surprise to many. The fresh day range in the European session stretches from just below the 1.33 figure to 1.3344’ish so far, with regional PMI’s the obvious driver for the directional move. Long EUR traders remain intact and in play, looking towards the recent long-term objective to retrace the 2011-12 decline (1.3490). The long stop-losses are comfortably placed below the 21 DMA of 1.3230.

Other Links:

Whose Chain Are Central Banks Pulling?

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019