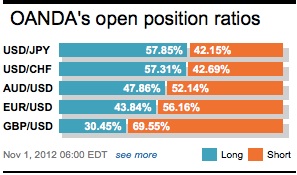

What would we do without JPY? Amongst the G10, it was the outright go to currency pair that generated most of the overnight excitement, breaching 80.00, the psychological benchmark on no meaningful data. There is a possible list of negatives, like a warning from Moody’s that the ongoing impasse over funding the Japanese budget deficit is credit negative or perhaps the poor earning’s season unfolding in Japan could be blamed. The disappointing BoJ policy ease this week is already history, so that is a no go.

Stops were taken out as high as 80.11. Dealers note that offers appear ahead of 80.40-50, with the latter quote a presumed option barrier level. We can expect, that with a very good NFP tomorrow and generally higher US yields, for these levels to be at least threatened medium term. The latest flow data continues to show outflows from the Japanese money market, suggesting that JPY is again being used as a funding currency of means, especially domestically. This is certainly good enough reason for the pair to continue its current upward momentum.

Is the “tail risk†of a Chinese hard landing dragging Asia down being reduced? The risk of an Asian recession seems to be fading, which can only be good news for yield hunters. October PMI indices are recovering modestly across the region. Despite the Australian data being the laggard on the month (45.2), China’s PMI is edging higher, to 50.2 from 49.8, m/m (new orders rose +0.6p to 50.4, and export orders rose +0.5p to 49.3.). Stronger data has led to a broad based improvement across China’s sub-indices and evidence of China’s economy stabilizing. Again, this is being touted as strong proof of a modest rebound in industrial activity heading into Q4. Elsewhere in the region, manufacturing PMI’s in Korea, Taiwan, and Indonesia have also advanced. Perhaps this is the proof required that may limit the downside risks to Asian currencies?

GBP is off its highs after downward revisions and a poor manufacturing print. The UK manufacturing sector fell for a second consecutive month in October, again underlying the fragility of its own economy despite the sharp rebound in growth in Q3. This morning’s PMI print for the manufacturing sector fell to 47.5 from 48.1, m/m, and further into contraction. This sector continues to be hindered by declining export sales, depressed demand and rising cost pressures. Despite the manufacturing sector being a small part of the UK economy, the data remains a strong reminder that UK Q3 growth data of +1% was abnormal. Recent strong employment numbers could see the BoE hit pause in November.

US reports today should be reinforcing the theme of “steady growth at subdued levels.†The street is calling for an unchanged manufacturing ISM reading of 51.5, similar to the message from last week’s Markit index. In the jobs sector, the October ADP employment change data expects a +135.0k print and an unchanged reading on jobless claims at +369k. Anything close to expectations should be moderately supportive for risk sentiment. Do not be surprised to see more range trading in anticipation of tomorrows NFP release.

Many now expect the single currency to remain confined to a tight range as we wait for both the US jobs data and election to pass. It seems after yesterday’s price action that the specs have erred to short the EUR on the back of the October month end-flow. The softer tone of S&P’s futures so far this morning adds weight to the EUR’s negative tone. Option expires are aligned at 1.29, 1.2965 and 1.30 today. Any substantial breakouts to the downside, do not be surprised to see the sub 1.29 ‘area peppered with s/l revers orders below and again opening the way for the recent lows to be tested.

Other Links:

Are EUR Shorts Waiting for Month End Dollar Demand?

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019