USD/JPY H1

Asia session started with price kept above 78.60, the peak of 11th Oct and bulls never looked back the entire Asian session. We manage to see higher lows throughout Asian session, and 6 bull candles out of 8 during the journey to the new weekly high. Price is currently in between H3/H4, but still trading slightly above Yesterday’s high.

AUD/USD H1

It will be important to see if AUD/USD manage to keep it’s head above 1.02582, which coincide with the bottom of trading range found between 10 – 11 Oct. A break below Yesterday’s high will open up Today’s L3 level as intraday support.

NZD/USD H1

Not sharing the bullishness of its Oceanic counterpart as NZD/USD remained depressed. Price did enjoy the Asian early rally experienced in USD/JPY and Aussie but bulls were not able to keep price above L3, not to mention hitting previous Swing High.

Hang Seng Index Futures M15

Market gapped higher on the back of strong US Retail Sales, but bulls were still unable to break above the upward rising trendline. If 11th – 14th Oct price actions can be used as any indication, we could see price potentially ranging for most of Wed with another attempt to push back to the upward rising trendline via a strong bullsih candle rather than a measured move upwards.

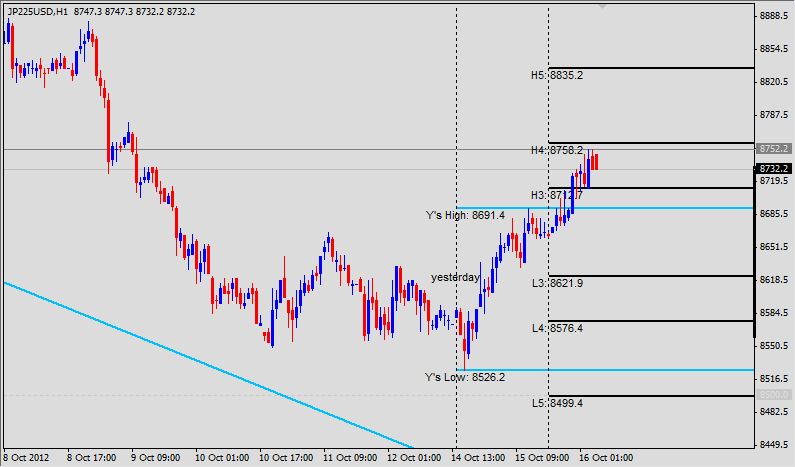

Nikkei 225 Futures H1

We started today with strong optimism as price managed to clear previous swing high on October 11. However price is currently trading within today’s H3/H4 zone with coincides with small consolidation area found on 8th Oct. Failure to break higher may push prices back down while a break above H4 will open up H5 for a potential Bowl Shape pattern to be formed in the future with an extended consolidation area found along H5 as a “Handle” similar to what we’ve seen on 8th Oct.

Bottomline:

Equities and USD/JPY points higher, which is a good sign for risk-appetite. However it is disconcerting to see Aussie and Kiwi unable to share the same bullishness. This could be explained if one is to believe that market is pricing in for further rate cuts from both RBA and RBNZ which is a possibility after RBA minutes and also New Zealand lower than expected CPI.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Latest posts by marketpulsefxstaff (see all)

- Oil Remains Near Multi-Month Lows - 6 August 2015

- U.S. Dollar Higher on Recent Data - 6 August 2015

- Greece’s PM Tsipras: Loan Deal with Lenders Close - 6 August 2015